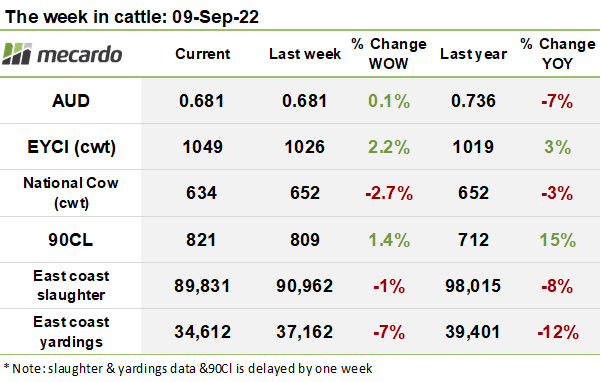

On the surface, the advances in cattle prices seen this week look encouraging, but indications are that support is coming not from strengthening demand but falling supply of young cattle. What needs to be pointed out is that the over the hooks indices are on a gentle downtrend, and slaughter numbers still sit well below average, even on the levels seen last year.

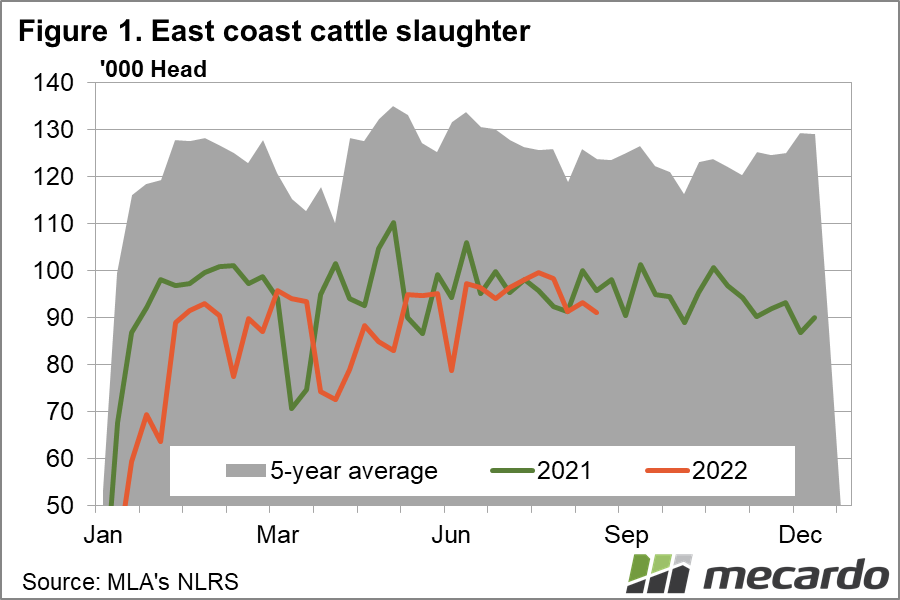

Last week’s east coast slaughter volumes data showed that numbers are continuing to decline. This is in line with the general trends we have seen on average for this time of year, but the 1% fall down to 90,962 head brings us 8% lower than this time in 2021, and miles under the 5 year average of ~125,000 head. The downward shift gained its impetus from a 5% fall in QLD numbers, partially offset by an increase in slaughter within NSW and VIC of 6% and 3% respectively.

The preliminary national cattle yardings running total comes in at around 34,000 head, around 6% below last week. Again, everything in the marketplace that we can see about this week is indicative of tighter supply. Yardings numbers across some of the major indexes are well down on last week, with EYCI eligible yardings down 24% to 8,697 head, while restocker and feeder steer volumes both slipped 10%. Some of the driver for lower yardings in QLD, like in Roma Store on Tuesday was due to heavy rain impacting logistics.

The Eastern states Young Cattle Indicator (EYCI) bounced 23¢(<2%) higher this week to reach 1,049¢/kg cwt, supported by lower eligible yardings.

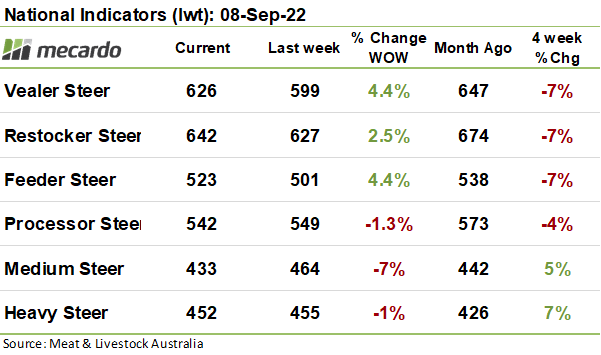

The Western Young Cattle Indicator (WYCI) faltered this week, giving back the gains made last week, dipping 28¢(3%) to end the week at 957¢/kg cwt. Prices were pressured by a fall in the vealer percentage in the index from 37% to 23%, while steers traded 11¢(1%) lower, finishing the week at 985¢/kg cwt.

The national indicators were a mixed bag of results, with younger cattle price generally lifting, while finished animal prices fell lower. This week’s wooden spoon was awarded to medium steers, which posted a 31¢(7%) loss for the week, closing at 432¢/kg lwt. Bear in mind though that the index is thinly represented, with only 105 head in the mix this week. In contrast, Feeder steer prices lifted 22¢(4%) to finish up at 523¢/kg lwt.

90CL prices pushed up 12ٌ¢(1%) this week to 821¢/kg swt. Steiner reports that one factor supporting the market is a sharp reduction in the flow of Brazilian beef into the US. An emerging trend in US meat retailing (and consumers) are for more focused on budget cuts of beef in recent times. This trend is supportive of 90CL prices, but the price outlook for more higher end cuts is looking softer.

Some doubt has been cast over the accuracy of the data behind the record high levels of July Chinese beef imports that have recently been circulating in the market. Steiner reckons that the sky high figures don’t mesh well with export data from China’s key contributing import sources, including Australia. One theory was that COVID-Zero related disruptions may have caused some of the import volumes reported in July to be actually related to prior months, making the big spike a symptom of a record keeping issue.

The week ahead….

Strengthening prices driven by tightening supply isn’t a sign of high confidence within the markets at present, especially given that finished cattle prices are trending downwards. One sign that there are pockets of positive, but considered and measured restocker confidence out there, is that some saleyard reports are indicating that buyers are actively searching for examples of young cattle with good frames on them, and that condition is of a secondary consideration.

As such, producers with well bred store stock with great potential have a good chance of commanding prices well above average, especially given the trend towards more limited offerings in saleyards lately.

Have any questions or comments?

Click on graph to expand

Click on graph to expand

Click on graph to expand

Data sources: MLA, NLRS, Mecardo