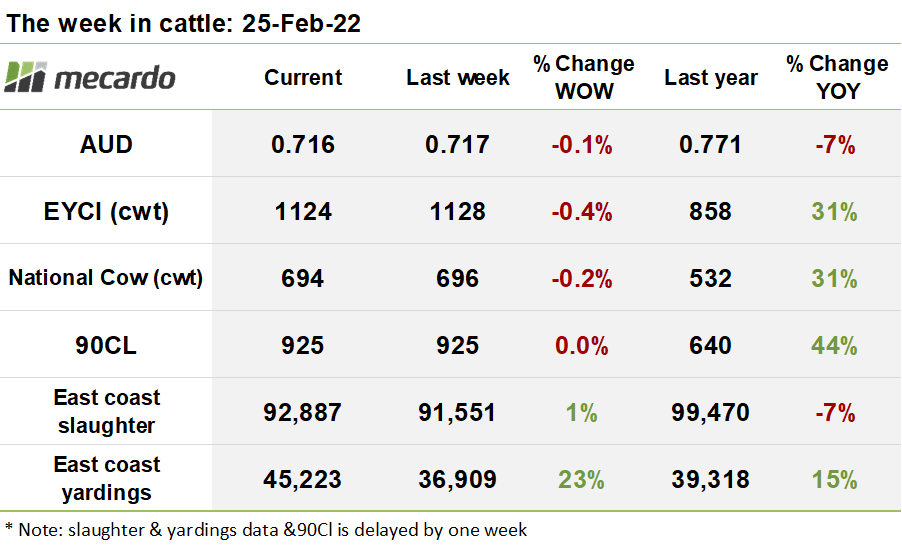

We saw a significant increase in cattle from QLD, for the week ending 18th February 2022. Strong US cow liquidation also paints a rosy picture of US demand for Australian beef into 2023 and 2024.

East coast slaughter volumes inched up another 1% last week, which is no surprise given a gentile incline tends to occur at this time of the year. 71% of the increase emanated from QLD, and 27% from VIC.

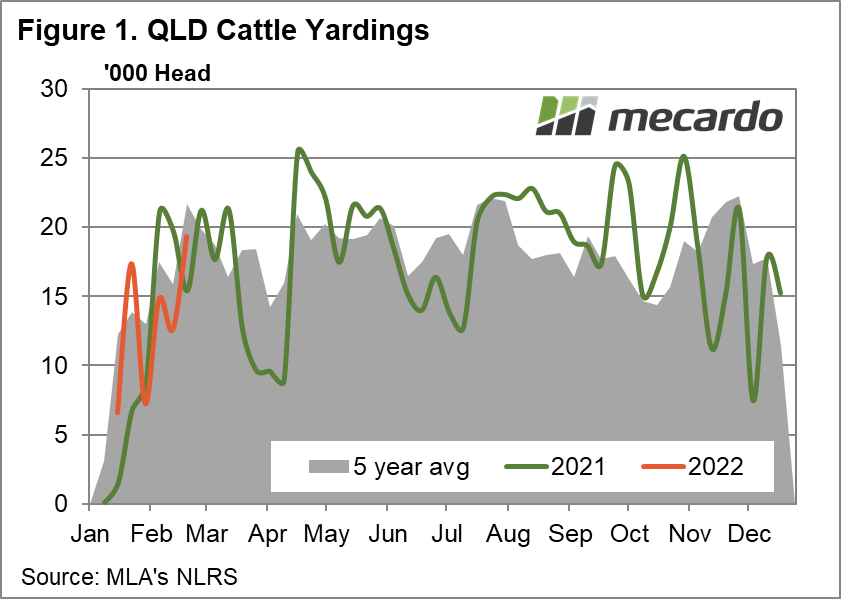

Yardings on the east coast surged 23% week on week last week to 45,233 head with QLD driving the increase in supply, booking a huge 81% (6700 head) jump from the week prior, backed up by a 16% (2,200 head) increment coming out of NSW. From a historical perspective, a late February surge in yardings from QLD and NSW is fairly typical though, as it happened both last year in QLD, and generally over the last five years. This year however, it looks more significant as it’s coming off a lower base, and a touch earlier in the year.

The official yardings data release essentially confirmed the truth in the leading signal we saw last week in the form of a big 22% jump in EYCI eligible yardings. This week EYCI eligible yardings have dipped 7% to 13,454 head though, so we may see that supply this week has fallen.

The EYCI fell a smidgen, 4¢ (<1%) to 1,124¢/kg cwt, reversing from last week’s minor recovery. Roma store lead the way again, contributing 17% to the weekly index, at 1188¢/kg cwt, followed by Dalby at 13%, at 1,145¢/kg cwt. The slight fall in price despite lower supply may be indicative of lower demand for young cattle this week, but it’s nothing major at this stage and the price fluctuation could just as well be put down to fluctuations in quality or a change in average weight.

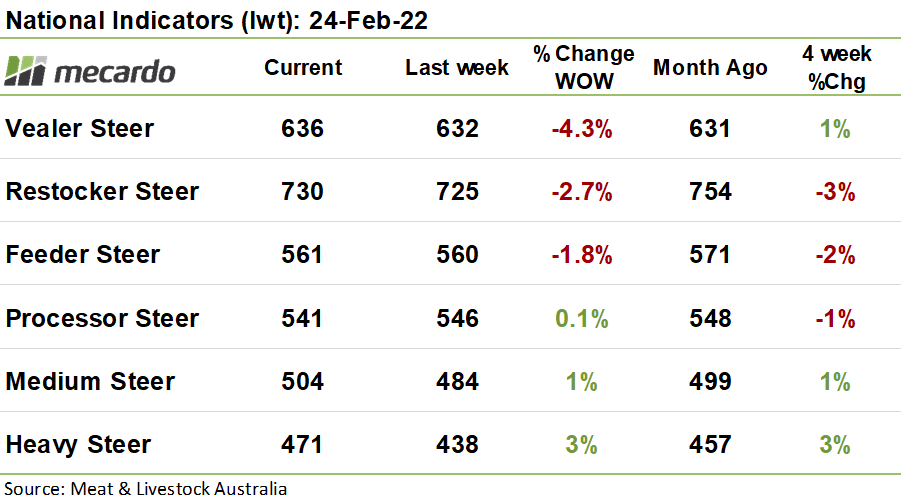

Over in the west, the WYCI fell 31¢(3%) to 1,080¢/kg cwt, again on a reasonably solid yarding of 728 head, down 23% from the prior week, with the proportion of vealers in the market remaining stable at around 75%.

On the national categories there was mostly red ink on the board with restocker steer prices shedding 20¢(3%) to 730¢/kg lwt, with feeders and vealers also flopping 2% and 4% respectively. More encouragingly, the national heavy steer price lifted 15¢(4%) on the week prior, led by an average price of 511¢/kg lwt being paid in Wagga for 101 head of cattle, making up 30% of the index this week, followed by Dubbo at 449¢/kg lwt, contributing 25%.

The US frozen cow 90CL price has lifted 5¢(2%) in US dollar terms, to 305¢US/lb but in Australian dollar terms, was steady at 925¢/kg swt. Steiner comments that the ongoing drought fuelled liquidation of the US cow herd spells disaster for beef supplies in the future as the US herd is decimated, meaning that Australia’s expanded herd is well placed to take advantage of higher US demand for imported beef into 2023 and 2024.

The week ahead….

In the scheme of things, prices are holding ground tenaciously despite higher supply coming on from QLD, with producers looking to restock clearly prepared to pay up. This, coupled with rising slaughter numbers indicating that demand for finished cattle is tracking along comfortably, is all supportive of another stalwart week ahead on the markets.

Have any questions or comments?

Click on graph to expand

Click on graph to expand

Click on graph to expand

Data sources: MLA, NLRS, Mecardo