The article earlier this week looked at non-mulesed and RWS premiums. RWS is one of a range of quality systems, so in this article Mecardo looks at the supply of SustainaWool and Authentico in comparison to RWS as well as premiums.

For this article the focus on quality systems has been widened beyond RWS to include SustainaWool and Athuentico. SustainaWool data in this article is split into non-mulesed and other.

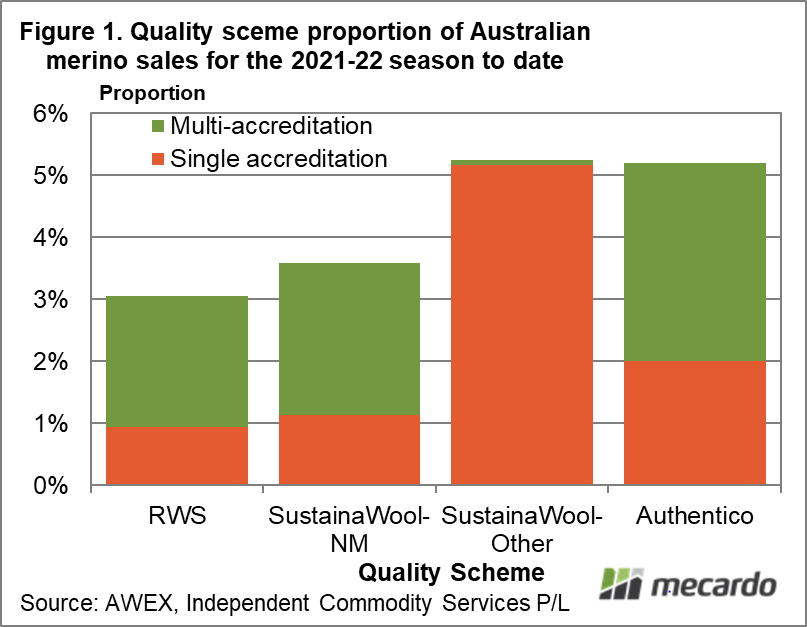

Figure 1 shows the proportion of Australian merino wool sold at auction for this season to date which was accredited to RWS, SustainaWool (non-mulesed and other) and Authentico. New Zealand merino wool sold at the Melbourne sale centre has been omitted. Many sale lots are accredited to more than one quality scheme. Each quality scheme in Figure 1 is divided into the proportion of lots accredited to one system only (single accreditation) and into the lots with accreditation to multiple quality systems (multi-accreditation).

For the 2021-22 wool selling season to mid-March some 3% of merino wool sold (on a clean base) has been accredited to RWS, 8.5% to SustainaWool (3.5% non-mulesed and 5% mulesed) and 5% to Authentico. SustainaWool is clearly the largest scheme and RWS the smallest by volume, although in non-mulesed terms SustainaWool volume is on par with the smaller RWS scheme. There will be some leakage of accredited wool outside of auction (direct/forward sales). As a contrast the South African merino clip has 28% of its volume accredited to RWS for the season to date (from late September ’21, when sales volume reporting by Cape Wools began).

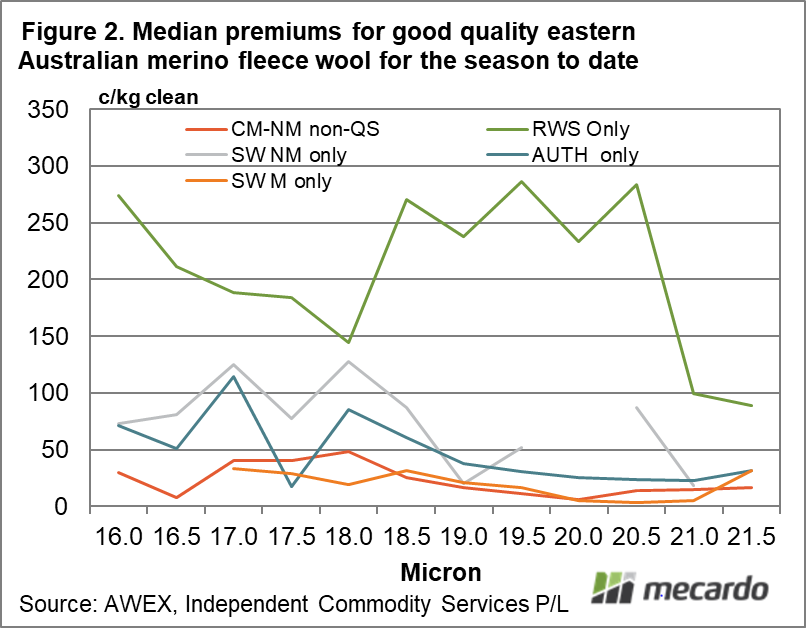

In terms of premiums the focus this season has been on RWS wool, simply because the premiums both in Australia and South Africa are so large. Figure 2 shows an estimate of the median premiums by micron category, for the season to date, for the quality systems with regard to good quality merino fleece. Only lots with a single accreditation were used for the analysis, which limited the available data for all the quality schemes. Good quality merino fleece in this instance means full length fleece (70 to 110 mm), 0-1.5% vegetable fault, eastern selling centres (there is plenty of good wool in Western Australia but not much RWS, with only 5% of merino wool declared CM-NM in the past year compared to 20% in the east), no subjective faults and no ASF lots (spinner style wool which can distort price calculations). Prices for the quality systems are simply compared to wool which was either declared mulesed or had no declaration.

RWS stands out in Figure 2 due to the high premiums, which are similar to those reported by Cape Wools for the South African market. As a benchmark non-mulesed wool which was not accredited to any of the three quality systems has been added to Figure 2. Authentico and SustainaWool non-mulesed are performing slightly better than SustainaWool mulesed and the base non-mulesed, non-quality scheme wool. The methodology used for this analysis is simple, with the small amount of wool available for RWS and Authentico engendering caution when looking at the results. The key point is that RWS premiums are significant, while premiums for non-mulesed wool with a quality system accreditation and for SustainaWool and Authentico are generally small.

What does it mean?

Low volume remains an issue for the RWS and Authentico and for SustainaWool non-mulesed. Premiums for RWS wool are in another league when compared to non-mulesed wool and wool with accreditation to other quality schemes. The premiums for RWS are in the order of ten times the non-mulesed premium, while SustainaWool mulesed is on par with non-mulesed premiums with Authentico and SustanaWool non-mulesed about twice the non-mulesed premiums.

Have any questions or comments?

Key Points

- SustainaWool is the largest quality scheme by volume, with Authentico the second largest and RWS the smallest of the three considered in this article.

- The simple nature of the analysis used for this article raises caveat with regards to the results but RWS premiums stand out in relation to the other major quality schemes.

- Premiums for SustainaWool non-mulesed look to be on par with the premiums for Authentico.

Click on figure to expand

Click on figure to expand

Data sources: AWEX, ICS