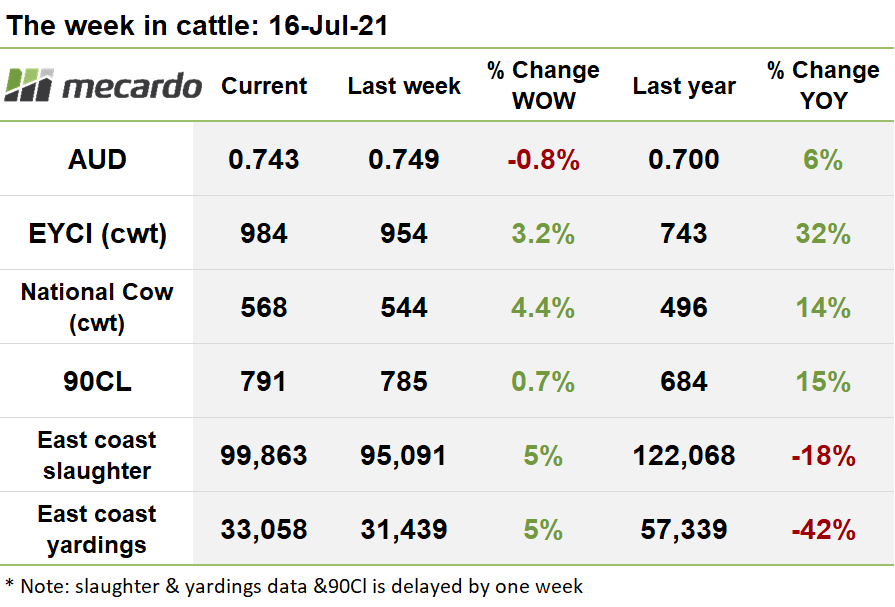

Another week, another record. Solid rains in QLD, coupled with talk of a possible repeat of La Niña conditions for the season ahead kept the momentum up, and the EYCI reached for the sky again, hitting, yes, a new record on Wednesday. In some major selling centres, yearling steers are already selling at prices north of 1,000ȼ/kg, indicating where the overall market for young cattle could head.

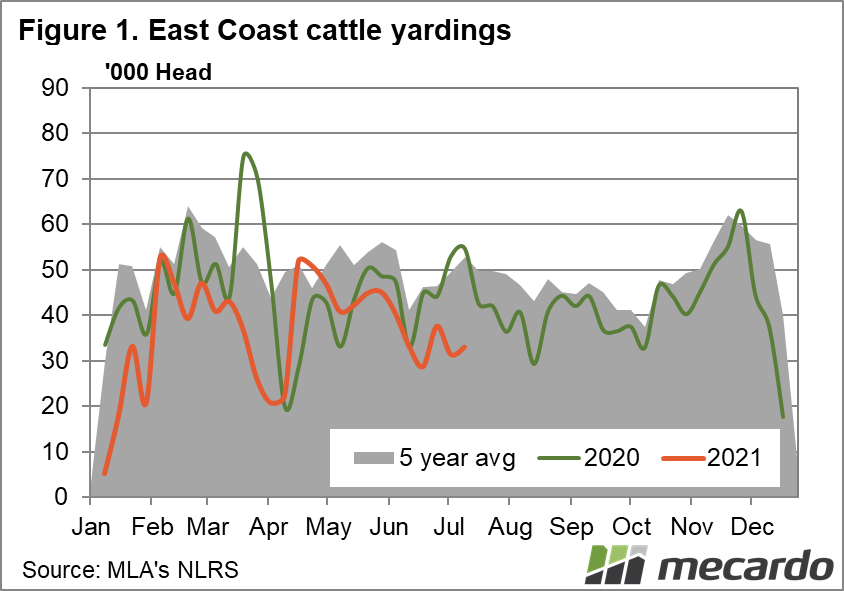

Yardings lifted 5% on the week prior, with the bulk of the additional supply coming from NSW and VIC, which offered numbers rise by 19% and 16% respectively. In contrast, QLD supply tightened, with yardings falling by 8% week on week. A total of 33,058 head were yarded on the east coast for the week ending 9th July 2021, up 1,619 head from the week prior. Last week, AuctionsPlus yarded 10,439 head, down 19% on the week prior, with clearance rates for young cattle remaining strong at well above 90%.

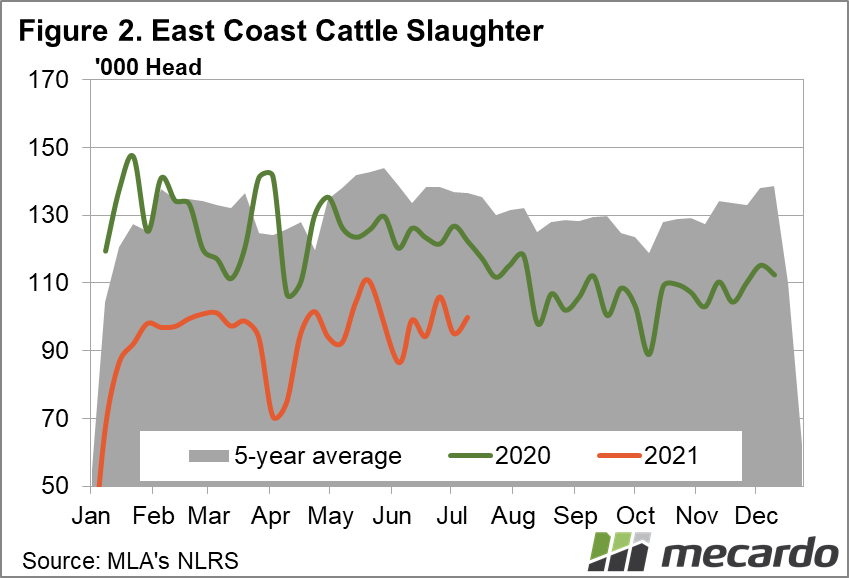

East coast slaughter also increased last week by 5%. While kill rates in all other states were virtually static, NSW production jumped ahead by 19% week-on-week. In total, 99,863 head of cattle were slaughtered for the week ending 9th July 2021, which was up 4,772 head on the week prior.

The Eastern Young Cattle Indicator (EYCI) added another 30ȼ(3%) for the week, reaching a new all-time record of 988ȼ/kg on Wednesday, before settling at 984ȼ/kg yesterday. This was achieved despite supply of eligible cattle being up 27% week-on-week at 13,532 eligible cattle. Looking at the top three EYCI contributing saleyards, which made up over 60% of the index this week, the market was red hot at Roma Store. Prices there averaged 1,000ȼ/kg cwt, all attributable to yearling steers and heifers, with the situation little different at Dalby, while yearling steers fetched 1,009ȼ/kg at Wagga.

It was another positive week for the national indicators, with gains made across most categories, with the standouts being feeder steers and medium cows, which both gained around 3%.

Feeder steers climbed 13ȼ(3%), reaching 484ȼ/kg lwt, and similarly, medium cows increased 9ȼ(3%) to settle the week at 307ȼ/kg lwt. Heavy steers maintained the new high position achieved last week, adding another 6ȼ to finish the week at 432ȼ/kg lwt. Medium and restocker steers also enjoyed upward movement, gaining 8ȼ(2%) and 10ȼ(2%) to respectively close off at 417ȼ/kg lwt and 588ȼ/kg lwt.

Processor steer prices and vealers were the odd ones out, losing ground, with vealers dropping 15ȼ(3%) to come to rest at 533ȼ/kg and processor steers downshifting marginally by 2ȼ(<1%) to settle at 488ȼ/kg lwt.

The Aussie dollar fell 0.8% from its Friday close last week, bringing it to 0.743US today at time of writing. With the US CPI hitting a whopping 5.4%, fears are rising that the US federal reserve may need to instigate rate rises earlier than anticipated, causing an appreciation of the USD against other countries, helped along by cautious capital markets continuing to shift toward the safety of reserve currencies like the USD.

US 90CL frozen cow prices rose by 5ȼ(<1%) to 791ȼ/kg swt last week, with most of the increase coming from the depreciation in the AUD. Supply emanating from the peak period of NZ slaughter into the US is thought to be in the rear view mirror now, so a tightening in the market for imported beef over the next few months can be expected as a result. However, a steady trend of continued weekly depreciation in the US choice cut-out could be a sign of weakening US beef demand.

The week ahead….

The rain is moving south for the next week, with large parts of southern VIC and eastern NSW looking set to capture 50-100mm, though QLD is looking largely dry. We saw some minor hesitation and pullback in young cattle toward the end of the week, but with knowledge that prices of over 1,000ȼ/kg are being paid in major selling centres of QLD and NSW, plus news of another potential La Niña over summer still at the forefront of their minds, producers could very well push this market higher next week.

Have any questions or comments?

Click on graph to expand

Click on graph to expand

Click on graph to expand

Data sources: MLA, Mecardo, BOM