The first new crop estimates for the 2021/22 season have been published in the USDA’s May World Agriculture Supply & Demand Estimates (WASDE) report. Of note, the USDA is expecting a record global wheat crop, US S&D for both corn and soybeans will remain tighter than normal, while global trade remains strong, including Chinese import demand.

Summary by Crop

Wheat

- The USDA has pegged Australian wheat production in 2021/22 at 27 million metric tonnes (Mmt). While the season is still young, this is well below the 33 Mmt 2020/21 crop.

- The 2021/22 US wheat production forecast accounted for higher acreage and increased yields, which resulted in a marginal increase to total wheat production to 50.9 Mmt. Russian wheat production for 2021/22 is estimated at 85 Mmt.

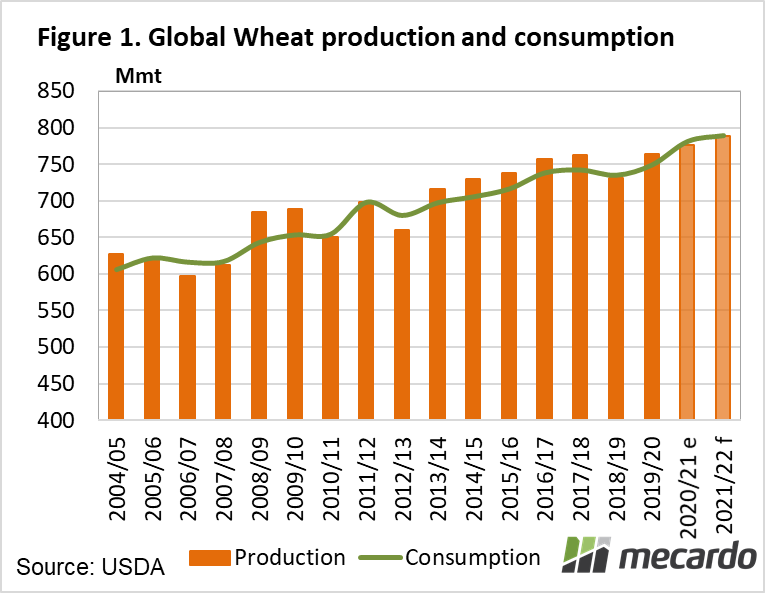

- Global wheat production was forecast to increase by ~13 Mmt in 2021/22 vs 2020/21. However, the tight carry in stocks from the prior season (2020/21) resulted in total supply growth being largely offset by wheat demand growth. Projected 2021/22 global wheat ending stocks were forecast to increase by only 0.29 Mmt year-over-year.

Corn

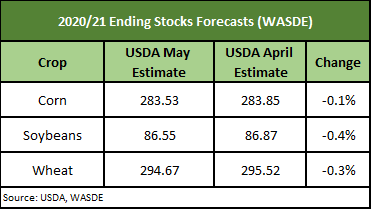

- The USDA made several changes to their old crop corn (2020/21) forecasts, resulting in tighter ending stocks. Projected corn ending stocks were lowered 95 million bushels to 1.257 billion bushels. This resulted in the projected stocks-to-use ratio decreasing to 8.5%, vs 9.2% in the April WASDE.

- New crop corn estimates (2021/22) were released and estimate production which is ~800 million bushels higher year-over-year. Domestic feed demand is projected to remain flat at 5.7 billion bushels, while Food, Seed and Industrial (FSI) use is projected to increase by 220 million bushels to 6.615 billion bushels. The increase to FSI demand is driven by increased corn use for ethanol in 2021/22 due to more normal driving behaviour as the US exits the coronavirus pandemic. Total US corn exports are projected to decrease by 325 million bushels year-over-year to 2.450 billion bushels. For context this would still be the second-best export season on record; higher than all years expect last season (2020/21). Ending stocks are projected to be 1.507 billion bushels, an increase of 250 million bushels year-over-year, however still tight relative to recent history.

- Global changes of note for old crop corn (2020/21) include an increase to Chinese imports to 26 Mmt (+2Mmt) and a conservative reduction to Brazil corn production to 102 Mmt (-7 Mmt). For new crop corn (2021/22) global production was forecast to increase by ~60 Mmt largely from increased production in Brazil, Argentina, and Ukraine. Global corn ending stocks are forecasted to increase by a modest 9 Mmt but remain well below 2019/20 levels.

- Generally, the initial 2021/22 estimates are in line with market expectations, however, the decline in exports was likely larger than the market expected as the forecasted ending stocks provided by the USDA did come in ~150 million bushels higher than average trade estimates.

Soybeans

- The US projected 2021/22 soybean S&D estimates production forecast of 4.4 billion bushels, an increase of 270 million bushels year-over-year.

- Chinese soybean imports were forecast to remain at 100 Mmt for 2020/21 but are expected to increase to 103 Mmt in 2021/22. Brazilian soybean production was forecast to increase to 144 Mmt in 2021/22 a 6% increase versus 2020/21. The increased global soybean production in 2021/22 was forecast to increase global soybean ending stocks by ~4.6 Mmt which, although higher than 2020/21, remain below 2019/20 levels.

- The changes made by the USDA to new and old crop soybean forecasts were largely in line with market expectations.

What does it mean?

In the hours post WASDE release 2021 corn futures fell by ~2 to 18 cents/bushel depending on the contract due to the forecasted 2021/22 corn stocks being above very bullish market expectations. Spot soybean futures traded up ~28 cents/bushel. Spot wheat futures were trading down ~12 cents/bushel on neutral USDA projections and falling corn prices.

The corn and soybean supply & demand outlook support an optimistic picture for wheat, despite big global production expectations. With corn supplies expected to remain tight, and demand remaining strong both in 2021 and into 2022, the USDA is tipping higher wheat consumption for food, seed and industrial as well as feed.

Have any questions or comments?

Key Points

- 2021/22 global wheat production estimates at a record 788.98 Mmt (up 13 Mmt or 1.7%)

- Production increases projected for Black Sea crops.

- Strong Chinese demand expected to continue.

Click to expand

Click to expand

Data sources: USDA, Nutrien, Mecardo