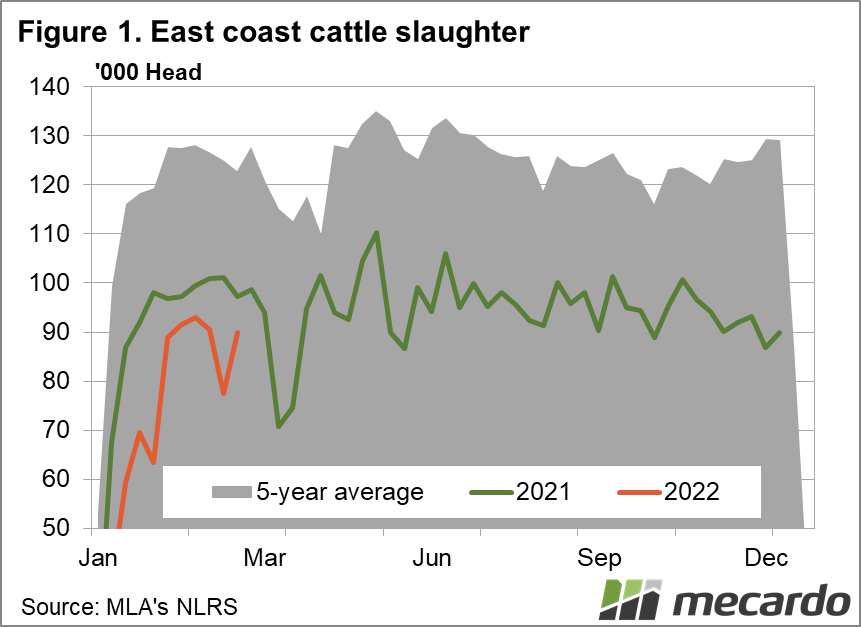

With the Brisbane port returning to service and alleviating logistics constraints in QLD, slaughter surged higher last week, and with it, producer confidence, as cattle also returned to the yards in spades.

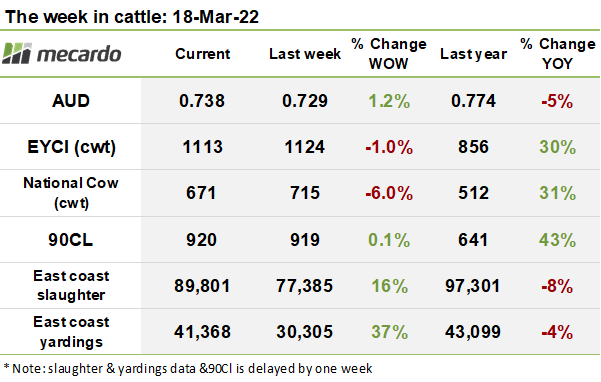

East Coast slaughter recovered strongly last week, rising 16% on the prior week to 89,801 head. The uplift was driven primarily by a 40% increase in throughput in QLD, with numbers slipping slightly in NSW and VIC. Although the kill rate is still 8% shy of where we were at the same time last year, it does appear that some of the flood-related logistics issues with workers, transport, and particularly cold storage capacity may have begun to resolve. Recent reports indicate that the port of Brisbane has largely fixed its flood related issues, and returned to service, operating at 80% capacity now, at 17 ships per day.

East coast yardings also charged ahead 37%, to 41,368 head, with QLD numbers surging over 125% to 21,311 head. This was helped along by a 23% pickup in VIC, all pointing towards a recovery of producer confidence in the markets.

EYCI eligible yardings increased 33% week on week to 14,072 head suggesting that the supply surge has continued this week also. However, this was not kind to the EYCI, as it gave up 10¢ to settle the week down 1% to 1,113¢/kg cwt. Roma store lead the way again, contributing 16% to the weekly index, at 1,191¢/kg cwt, followed by Dalby, at 15%, and 1,134¢/kg cwt.

Over in the west, the WYCI lifted 37¢(1%) to 1,152¢/kg cwt, again on a similar sized solid yarding to last week of 1,043 head. The marketplace remained 85% vealer dominated.

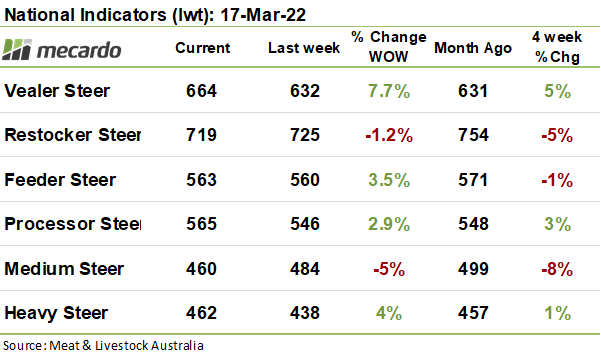

The national categories delivered more positive news, however, with solid price increments displayed in finished animals, reflecting a renewal in processor demand, though restockers and medium steers fell. Heavy steer price lifted 15¢ (4%) to 462¢/kg despite a slightly larger yarding.

The US frozen cow 90CL price was unchanged in US dollar terms at 305¢US/lb but in Aussie dollar terms, added 1¢ (<1%) to 920¢/kg swt, on the back of a slightly weakened Australian dollar. The latest Steiner report expresses concern that a US inflation rate of 8%, the highest in 40 years may weigh on domestic demand, particularly for foodservice, and that demand for lean beef in the US has taken a seasonal dip recently. The good news however is that domestic lean beef supply is expected to be tighter in April and May, which should support prices in the short term.

The week ahead….

At this time of the year, both slaughter and yardings typically decline somewhat, however, given the disruptions in QLD recently, we may see a backlog of cattle continue to come out of the woodwork next week. Indications are that despite higher yardings, demand for young cattle is still solid, so prices are likely to remain relatively resilient in the coming weeks.

Have any questions or comments?

Click on graph to expand

Click on graph to expand

Click on graph to expand

Data sources: MLA, NLRS, Mecardo