Lamb and mutton markets have been a wild ride over the last 12 months. Unexpected seasonal events have given heavy swings in supply and a massive range in prices. Here we take a look at if, and when the market might settle, and importantly, what level that might be.

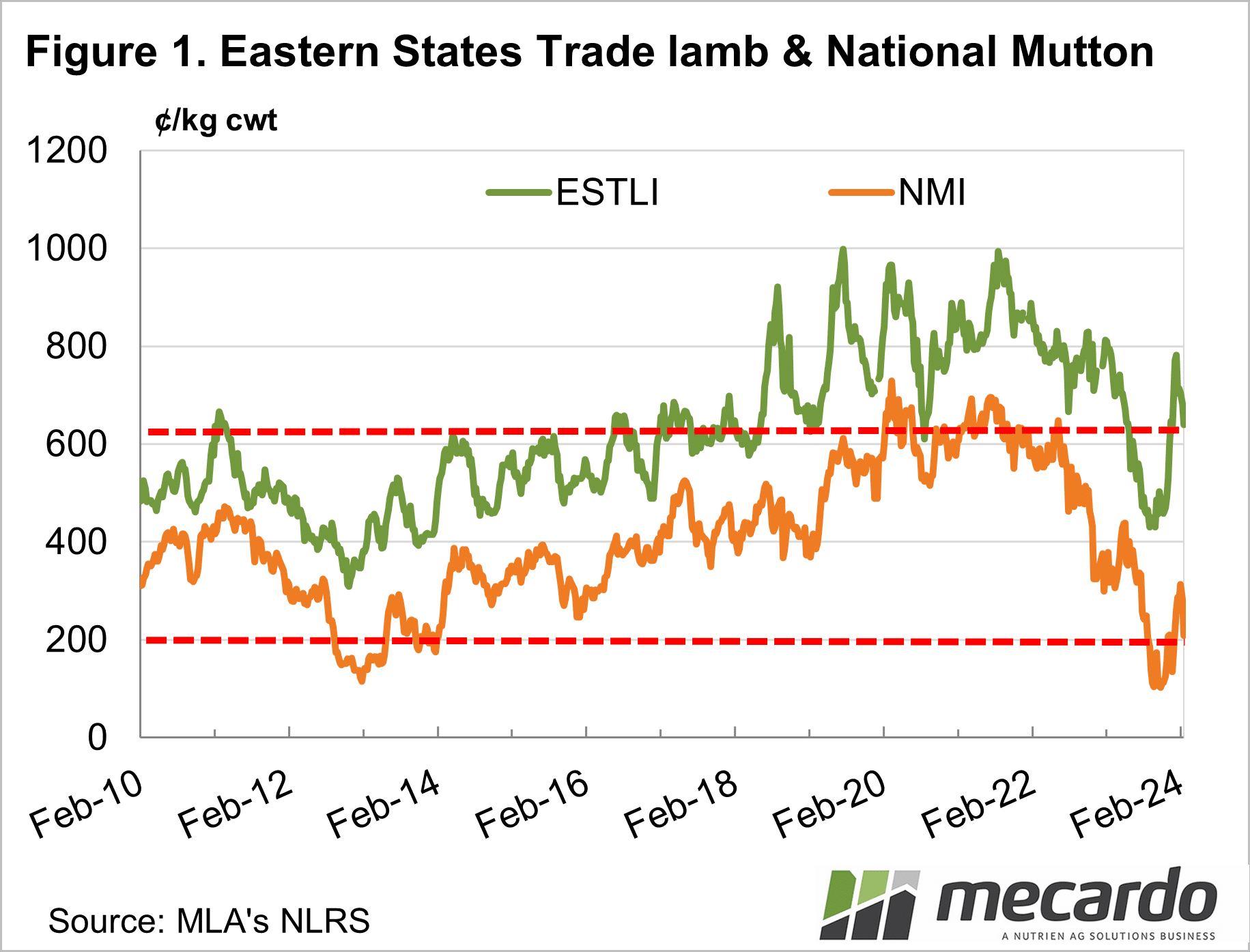

The wild range of the

lamb market over the last 12 months has been largely unprecedented (Figure 1). The fall from February to September was a 41%

drop. The Eastern States Trade Lamb

Indicator (ESTLI) hasn’t seen anything like that in the last 20 years.

Similarly, the rally

from November to January in the east recovered almost all of the 350¢ lost

through the middle of last year. In the west trade lamb prices picked up around

235¢ from November lows to January. We’ve only ever seen rallies of that

magnitude during the late autumn and winter supply squeeze. Supply is usually more consistent during the

summer.

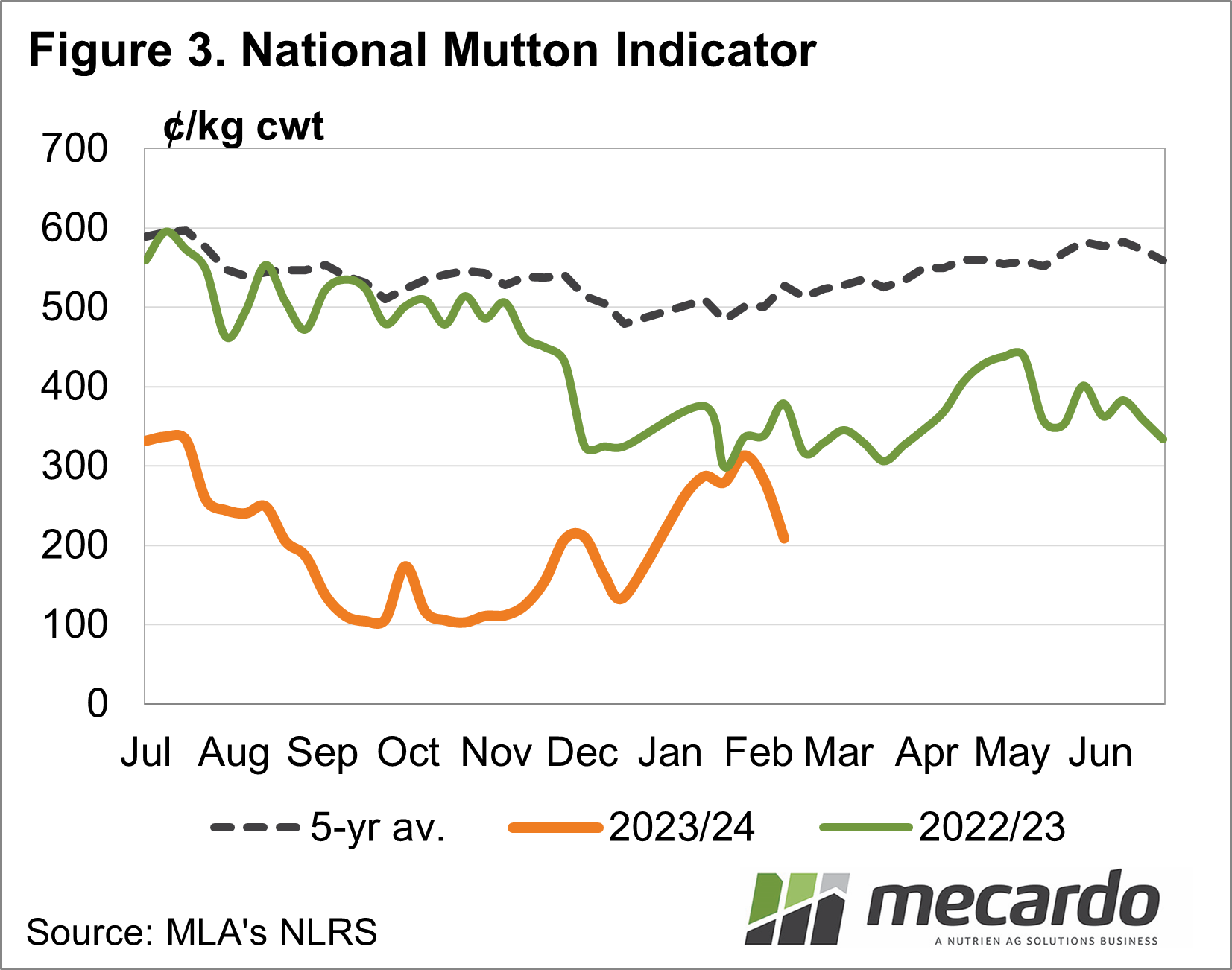

For mutton, the declines

were similar to lamb, but the recovery was not quite as strong. The relative values of lamb and mutton, and

the fact mutton doesn’t necessarily have to be ‘finished’ seem to mean it takes

less of a price rise to draw out mutton.

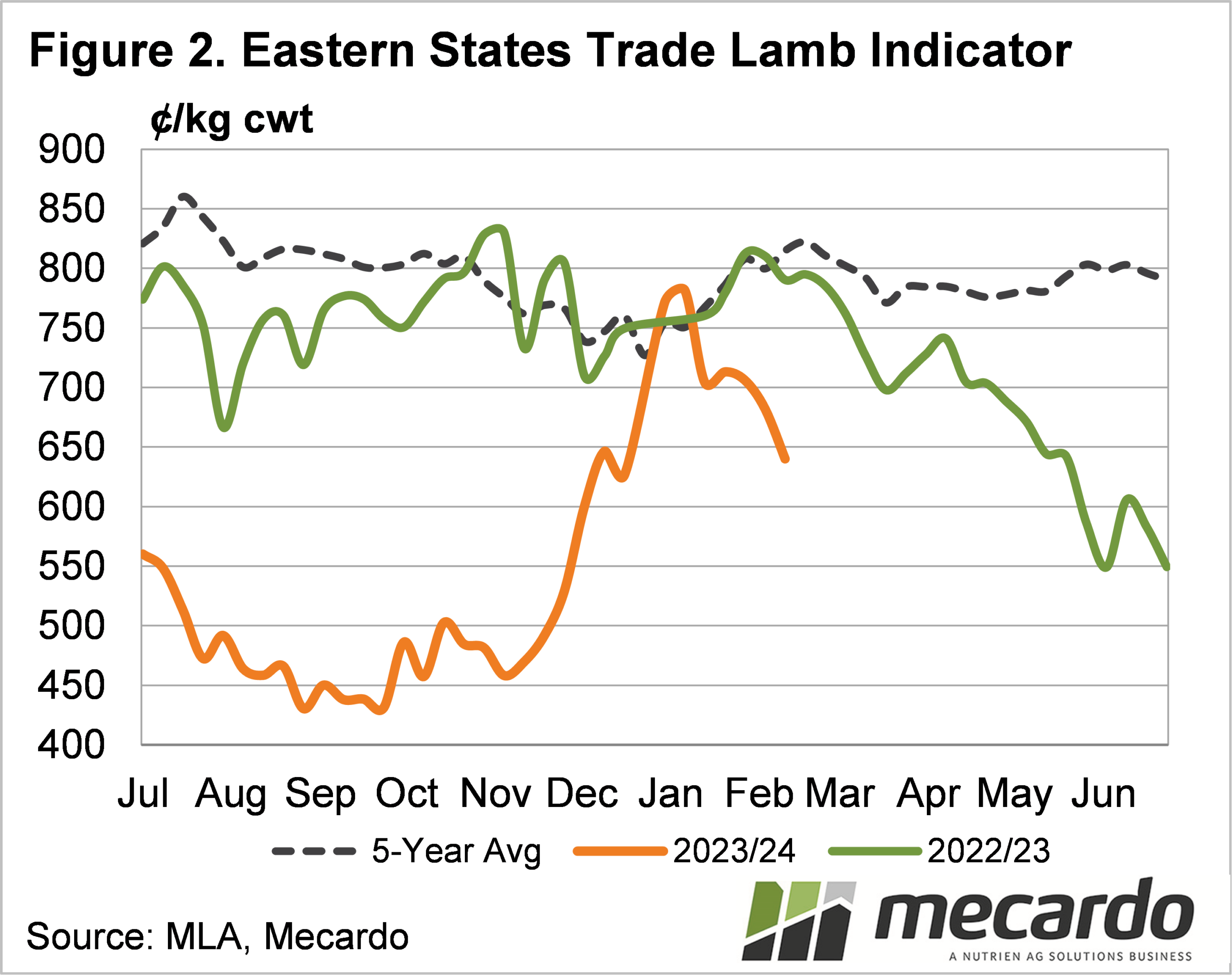

Big swings in markets

suggest supply and demand are struggling to find a level that suits both. Figure 2 shows the last time ESTLI did in

part find a consistent level was from July 22 to March 23. During this period the ESTLI ranged between

700¢ and 800¢/kg cwt. Interestingly, it

was at this level the market spent January.

Figure 1 shows there

should be solid support for the ESTLI at 600¢.

We know that slaughter capacity is at record levels, and anecdotal

evidence suggests that the 150¢ that has been stripped out of prices from the

peak should have made lambs profitable again for processors.

To halt the fall,

producer selling needs to slow down. A

fall in prices will help with this, but as we know rain would confirm it. Holding lambs, and in large areas feeding

them, needs to be profitable for lamb producers to slow up supply.

For mutton, it’s a bit

different. There is little in the way of

profits from weight gain, and price moves need to pay for the cost of holding

onto sheep. Tightening lamb supply would no doubt help mutton rally.

What does it mean?

The back-of-the-envelope calculations at 640¢/kg cwt in eastern states show feeding lambs for a month would roughly break even if prices remain steady. Those holding lambs will be looking for a price rise, and it doesn’t need to be much to turn a profit.

For mutton, it’s more about the timing of supply. The sheep appearing now are likely cast for age, or scanned dry autumn lambing ewes. You would think the cast-for-age sheep supply should be coming to an end, and prices will find support around current levels (Figure 3).

Have any questions or comments?

Key Points

- Lamb and mutton prices have been swinging wildly over the last 12 months.

- Lamb has shown a stronger price recovery than mutton.

- With recent price falls supply should slow down and find some price support.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: MLA, Mecardo