The last time we looked at lotfeeder margins, we concluded feeder prices had reached their limit, unless finished cattle could rally. Of course, over the last six weeks we have seen a massive rally in finished cattle prices, which hasn’t all flowed through to feeders, but they too are at a record.

We have all seen the record-breaking run of the Eastern Young Cattle Indicator (EYCI) in recent weeks, driven by restockers and feeders. Restockers can be irrational when there is grass and not many cattle but lotfeeders run tight margins. So how are lofeeders affording such lofty price levels?

It turns out that lotfeeders might actually be doing better under current record prices than they were back a month ago. The Queensland Over the Hooks 100 Day Grainfed Steer Indicator hasn’t been representative of actual prices recently, sitting at around 700ȼ/kg cwt.

Actual Grainfed over the hooks are prices are closer to the NSW Heavy Steer Indicator, which sits around 840ȼ/kg cwt. The rapid rise in finished cattle prices is being driven by export demand and tight supply, with 20%, or 140ȼ/kg added in the last six weeks.

The rise in finished cattle prices has added over $450/head to the value of a 340kg cwt steer, with the total value now over $2800.

With grain prices remaining relatively steady, much of the increase in value of finished cattle have been passed on in feeder prices. In prime and store sales feeder steers have been making up to 550ȼ/kg lwt, up around 90ȼ on the last time we ran the margin model.

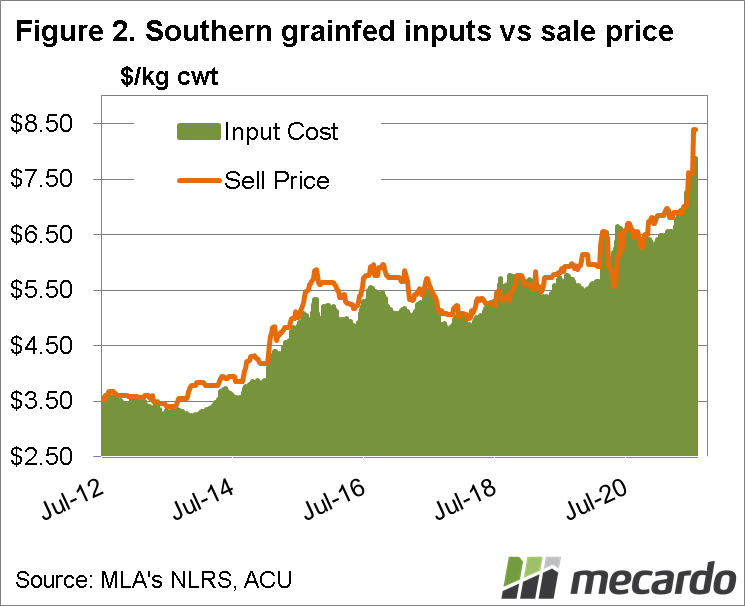

Figure 1 and 2 shows how the changes in price have impacted input and sales prices in northern and southern markets. Feed grain is a little cheaper in the south, and as such input prices are slightly lower.

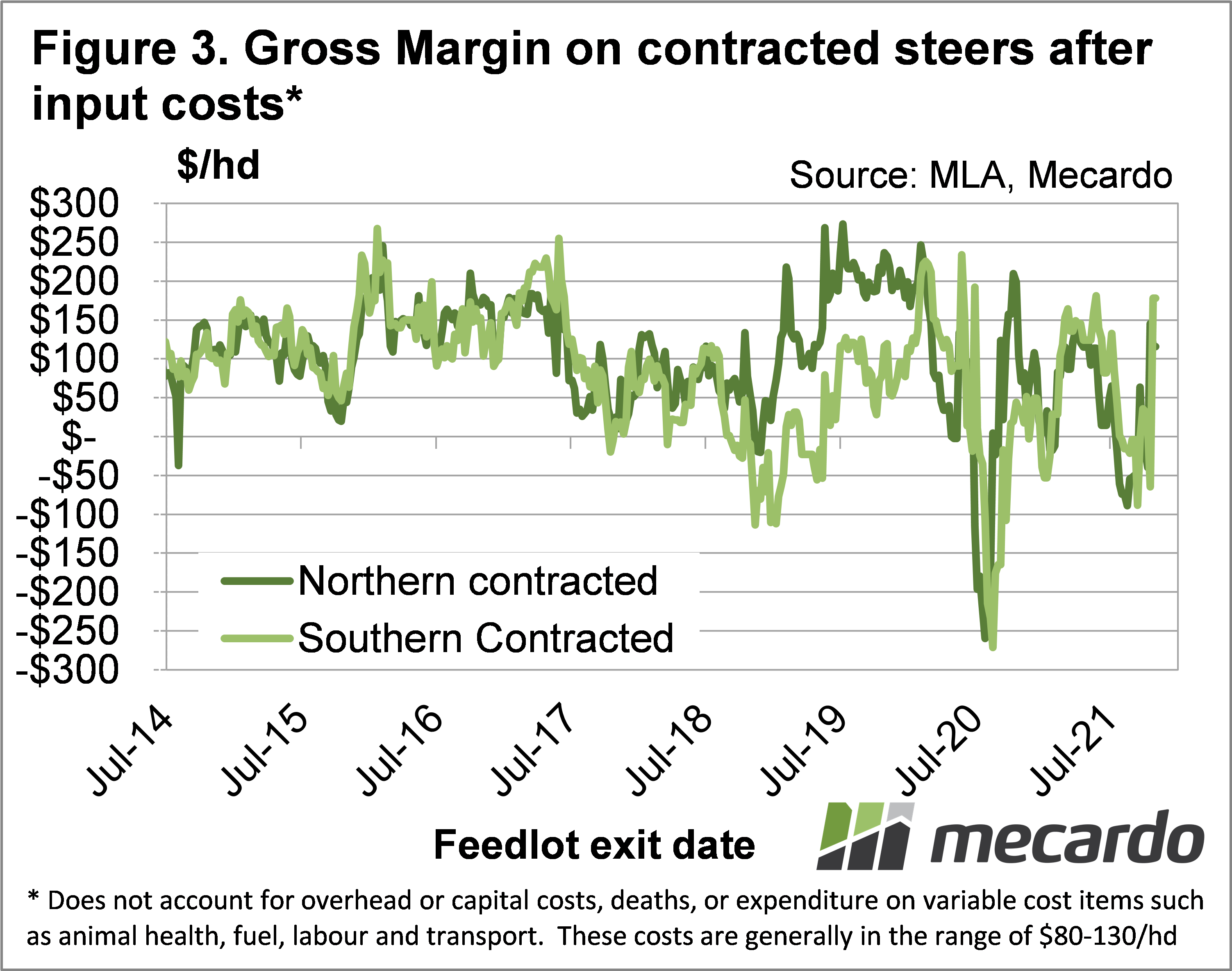

Figure 3 shows the margins between input costs and selling prices, with lotfeeders back in the black after spending three months in the red. The massive increase in input costs since 2019 hasn’t been matched by higher lotfeeder margins, which struggle to move past $150 per head. Returns are being squeezed, but in a tight cattle supply and low interest rate environment this might be expected.

What does it mean?

An over $100 per head margin in feeding cattle at this time of year is pretty rare, and it actually means there could be further upside in feeder and young cattle prices. We have seen margins below zero plenty of times when cattle are tight, but it would ‘only’ add a further 20-30ȼ to feeder prices.

There is an argument to say such high prices might draw out feeders earlier, and at lighter weights. This means the deficit of feeders might last longer than usual, and push back the spring seasonal price decline, if we see it at all.

Have any questions or comments?

Key Points

- Record finished cattle prices have largely been passed on to feeder prices.

- Lotfeeder margins have improved, leaving a little room for further feeder value increases.

- While finished cattle prices remain strong, feeder values should maintain strength.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: MLA, Mecardo