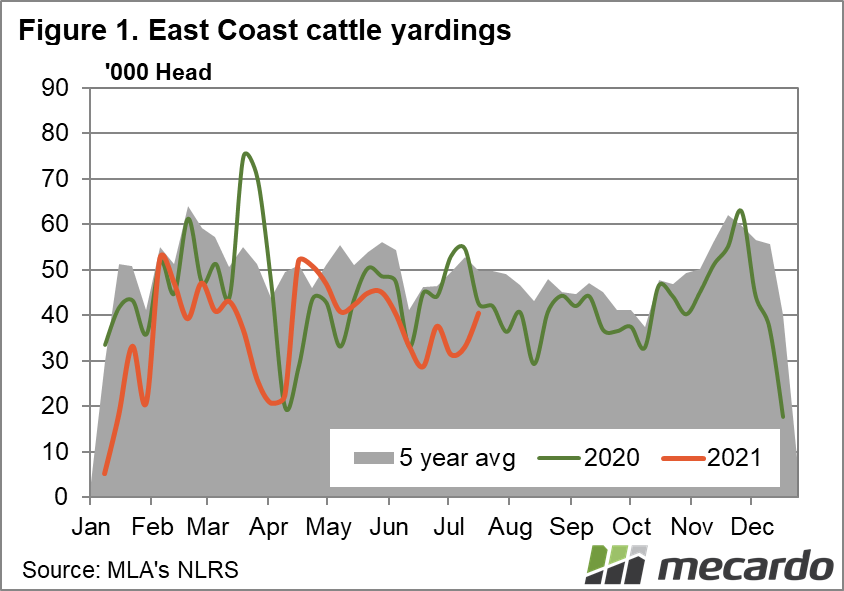

It’s hardly a surprise, but the EYCI has breached the 1000ȼ/kg level and Roma, QLD, has been one of the main contributors to it reaching this new pinnacle. Yarding’s for the week also picked up against the typical trend for this time of year as sellers were attracted by buoyant market.

Yarding’s lifted a solid 23% last week, with all the extra selling action happening in QLD, representing 103% of the total rise, with VIC providing an extra 15% on top. However, NSW hit reverse gear, with the falls in offerings equal to -20% of the net increase for the week.

A total of 40,516 head were yarded on the east coast for the week ending 16th July 2021, up 7,458 head from the week prior.

East coast slaughter reduced by 5% last week. The main negative impetus came from NSW, which fell 9% week on week, representing 56% of the downward movement, followed by VIC, where falls equated to 29% of the national decrease. A lift in yardings is somewhat out of character for this time of year, so the high prices must be the attraction to sellers stepping into the market.

In total, 95,226 head of cattle were slaughtered for in the week ending 16th July 2021, which was down 4,637 head on the week prior.

The EYCI continued to push further into the history books, progressively climbing higher over the week with barely a stumble to rise another 15c (2%) to achieve an unprecedented 1,003c/kg cwt, on a volume of 13,879 eligible cattle; only 2.5% above the prior week.

Roma Store continued to impress, averaging 1,019ȼ/kg over 5,570 head, composed entirely of yearling steers and Heifers, but Dalby’s price was behind the pace, at 978ȼ/kg cwt, with yearling heifer prices of only 958ȼ/kg dragging the average down below the 1,009ȼ/kg yearling steers were achieving in that market. Wagga fared better, at 1,030c/kg, on a smaller yarding of only 831 head, but heifers were the letdown again, with yearling steers fetching an average of 1,069ȼ/kg.

The national indicators mostly moved into positive territory this week, with medium and processor steers the standout of the bunch, while volatile vealers pushed up strongly in addition. This week, we will take a look at how much each of the indicators have advanced from levels seen at the start of the year, and interestingly, it is processor steers that have achieved the biggest percentage gains, not restockers.

Vealer prices advanced 33c (6%) to reach 566ȼ/kg lwt, meaning that they have appreciated a total of 23% since the beginning of the year. Restocker steers pushed up 14ȼ(2%) to close the week at 602c/kg, bringing their cumulative rise to 17% from January 2021 levels. Processor steers lifted 17c (4%) to settle the week at 505.4ȼ/kg, a level that is 21% above the opening Jan price.

Medium steer prices increased 22ȼ (5.3%) for the week, reaching 439.2ȼ /kg, up a total of 14% for the year. Feeder steers and medium cows were up 6ȼ (1%) and 8ȼ (2%) to settle the week at 490ȼ /kg and 314ȼ /kg, both clocking in a net rise of around 11% for the year. Heavy steer prices bucked the trend, backtracking 5ȼ (1%), coming to rest at 427ȼ/kg, representing a net 13% lift for the year.

The Aussie dollar fell another 0.3% since last week to 0.738 US at time of writing, recovering from intraweek lows of 0.7329. The possible cause continues to be cautious “risk off” investor sentiment and worries about COVID resurgence, with the safety of reserve currencies preferred to volatile equity markets.

US 90CL frozen cow prices took a downward turn losing 2ȼ (<1%) this week, as the price in USD fell, cushioned slightly by the depreciation AUD. Steiner consulting reports that buyers have taken a pause as they consider uncertain forward demand, while supply of cheaper south American beef lifts, and forecasts of increased volumes of Australian beef shipments circulate the market.

The week ahead….

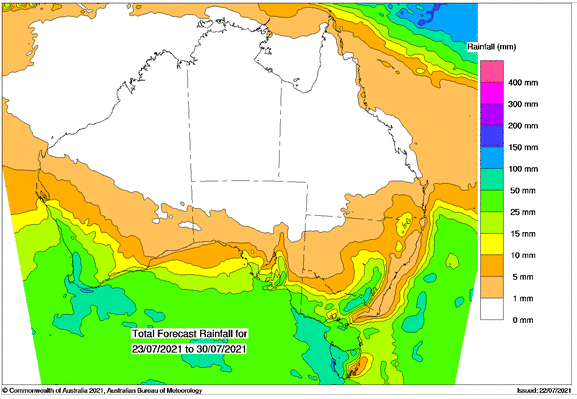

Little rain is coming in the north over the next week, with many parts of southern VIC and some areas of central southern NSW receiving a solid 25-50mm. With the EYCI so high, going from strength to strength each week, it’s possible that more sellers will be attracted into the market again next week, but it’s questionable about whether increased supply is likely to put a dent in prices.

Have any questions or comments?

Click on graph to expand

Click on graph to expand

Click on graph to expand

Data sources: MLA, Mecardo, BOM