In an ideal world we would consider the supply of merino wool out of the main southern hemisphere exporting countries as a whole, with regional variations, as the buy side of the market does. Along these lines, this article takes a look at merino RWS wool supplies and some of the premiums for the season to date.

Just as the raw wool market is part of a larger apparel fibre market, with prices for different fibres tracking similar patterns unless particular circumstances (usually temporary) intervene, the raw wool market is made up of national markets which track each other. In late September Cape Wools South Africa started publishing RWS volumes and premiums in their weekly market report. In the Australian wool market RWS volumes were small, with highly variable pricing in addition to quite varied wool quality so it was difficult to ascertain what the supply chain was prepared to pay for suitable wool with an RWS accreditation. The Cape Wools reports certainly prompted a closer look at what was happening here on the eastern side of the Indian Ocean.

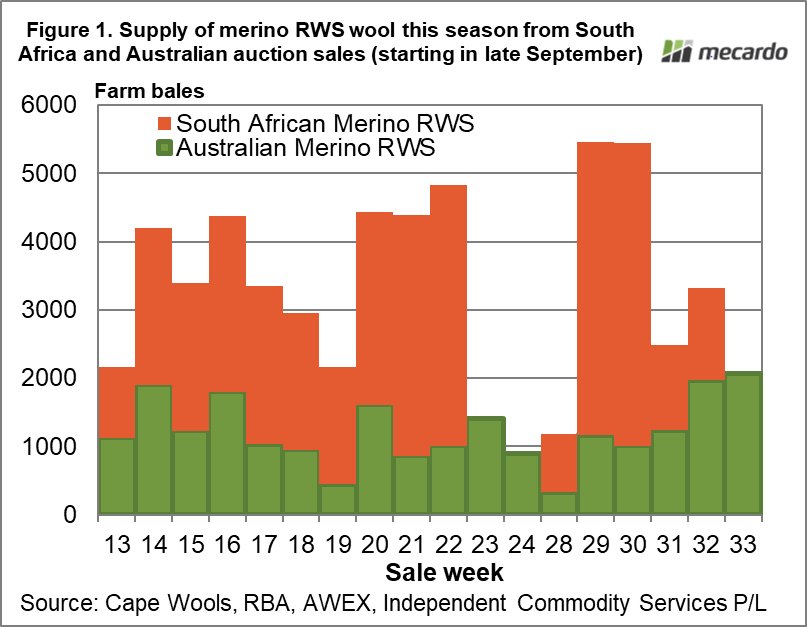

Mecardo has looked at the premiums being paid across the different micron ranges (view article here), so this article will look at Australian and South African volumes across the season (where the data is available). Figure 1 shows the volume of Australian and South African RWS accredited merino wool by sales week from late September through to last week. There was no South African wool sold last week due to logistics issues clogging up the shipping of wool. In the 17 sales weeks to Week 32 (two weeks ago) twice as much RWS merino wool was sold in South Africa as Australia, so South Africa is the key supplier at present.

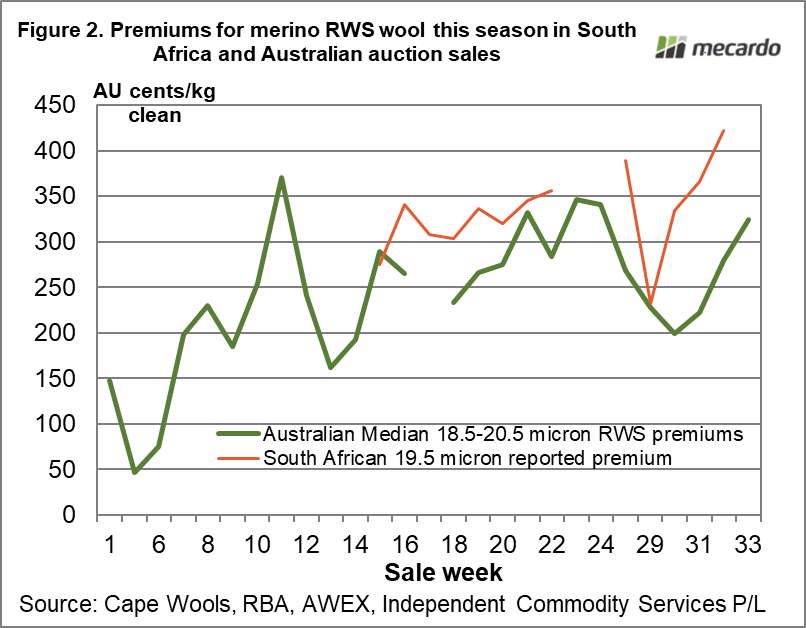

The South African merino clip tends to be broader than the Australian merino clip so the comparison for premiums shown in Figure 2 has been set at 19.5 micron. The premiums are shown in Australian cents per clean kg. For the Australian premiums an average price was calculated each week for good merino fleece (38 + N/ktx staple strength, full length, vegetable matter under 1.6% with no subjective faults) by half micron categories with the RWS accredited wool compared to non-RWS non-mulesed wool. It is not a perfect methodology but the consistency of the premiums and their similarity to the reported South African premiums gives confidence that the measured effect reflects a sizeable premium in exporter baremes for suitable RWS wool.

In the period when South Africa has reported RWS premiums the average for 19.5 micron wool in South Africa has been 323 cents and in Australia 257 cents.

What does it mean?

In Australia the weekly proportion of merino wool (all categories) accredited to RWS has ranged this season from 1% to 6.7%, with no real trend in the proportion. In South Africa on average 27% of their merino clip has been accredited. Without considering South America, which also supplies some RWS wool, there is obviously plenty of scope for supply to increase. The large premiums being paid are very likely to encourage increased supply, with some resulting downward pressure on the premiums. In the meantime the South African market reports are a good guide to the strength of demand for RWS wool.

Have any questions or comments?

Key Points

- Since late September twice as much RWS accredited merino wool has been sold in South Africa as Australia.

- In terms of premiums, for 19.5 micron the Australian premium has averaged 257 cents for suitable 19.5 micron fleece while in South Africa the average has been 323 cents.

Click on figure to expand

Click on figure to expand

Data sources:

Cape Wools, RBA, AWEX, ICS