Wool auctions go into a three week recess after the sales this week, recommencing in mid-August. Given the volatility in prices during the past two springs, after the mid-year recess, Mecardo looks at the seasonal price pattern.

In January Mecardo looked at seasonal price patterns in the 21 MPG, showing there has been a consistent weakness in price during the spring months but the overall pattern was not set in stone, it has varied through time. In the past Mecardo has looked at seasonal price patterns across a range of indicators, highlighting the wide range of possible price movements around the historic medians of these patterns.

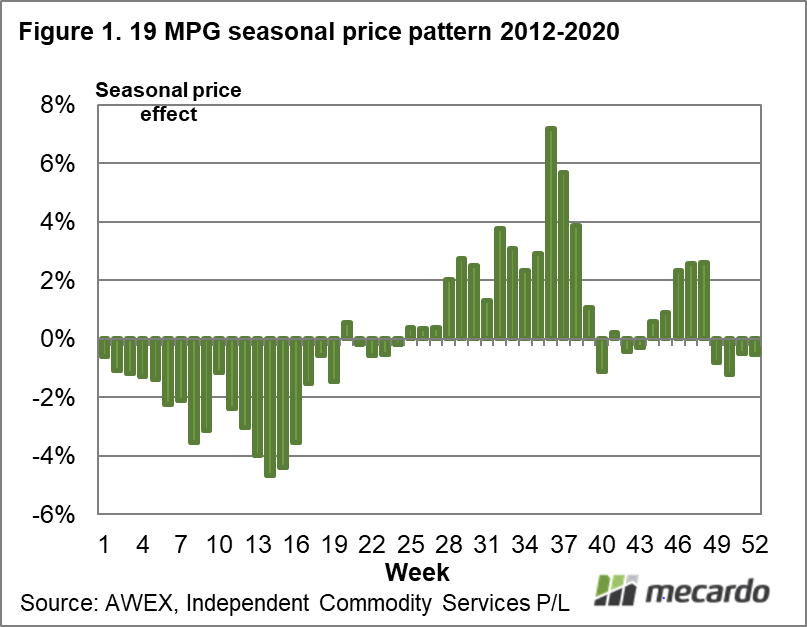

For the purpose of this article Figure 1 shows the median seasonal price pattern of the past decade for the 19 MPG. That persistent price weakness in the spring shows up, often finding a base in September/October (weeks 10-18). Without any other information the seasonal pattern indicates a price fall in the order of 4% during the spring is normal. This provides some guide to the likely direction of price and the extent of the move.

Now, the experience of the past two springs will be present in many minds of the supply chain. In 2019 greasy wool prices fell heavily as the wool market played catch-up with the general apparel fibre markets and then in 2020 the full weight of uncertainty from the pandemic belted prices lower. Will lightning strike a third time? Unlikely, but there will be some in the supply chain holding back in case it does, which is a partially self-fulfilling prophecy. This uncertainty allied with a Chinese economy is expected to slow in the second half of 2021 and plenty of greasy wool flowing onto the market points to the standard seasonal pattern of weaker prices in the spring.

As we have shown in the past, there is considerable variation in seasonal price movements between seasons. Figure 2 shows the best and worst of the past decade for the 19 MPG, and there is some difference between them. The 2020-21 season is not complete because of the nature of the calculations (rolling centred moving averages require approximately 6 months of extra data hence the 2020-21 line only extending to the middle of the graph). It would be fair to say there is no one in the supply chain who wants a re-run of last spring, as such a fall causes a lot of uncertainty and wipes a lot of value from stocks of raw and processed wool. On the other hand it is unlikely that a re-run of 2018 will happen due to the points made above.

What does it mean?

Guessing what the future holds is always a precarious venture. There seems to be enough headwinds in the form of a weaker Chinese economy and increased greasy wool supply to count out prices rising through the spring. On the other hand, the wool market is not in the midst of a major down cycle, so the risk of a re-run of the past two springs seems unlikely. That leaves a normal price cycle as the likely pattern we will see.

Have any questions or comments?

Key Points

- Spring weakness in wool prices has been one consistent feature of seasonal price patterns.

- In the absence of a major factor to push prices either up or down, the assumption that the standard (median) pattern is likely to appear seems reasonable.

- The seasonal price pattern points to prices easing by 4-5% into September/October, give or take a bit.

Click to expand

Click to expand

Data sources: AWEX, ICS , Mecardo