With cattle markets at extraordinary levels, there are still plenty of questions as to how long they can last. Even with a herd at an extreme low, and prices at extreme highs, the pattern of supply should still show some sort of seasonality. Here we explore how this might impact prices over the coming months.

Seasonality in prices is mainly driven by supply fluctuations. While there are times of higher and lower demand, supply has much more variation throughout the year. Predictably, price responds to stronger supply by moving lower, and vice versa.

Our two basic measures of cattle supply are slaughter and yardings. Interestingly, cattle slaughter and yardings peak at different times. Figure 1 shows cattle slaughter would normally hit its first quarter high in early February, before hitting the annual peak in May.

Figure 2 shows cattle yardings normally peak for the year in February, before having a more minor peak in May. The May highs for both slaughter and yardings are linked to strong sales of females out of northern cattle areas and coincides with strong supply of young cattle from autumn weaning.

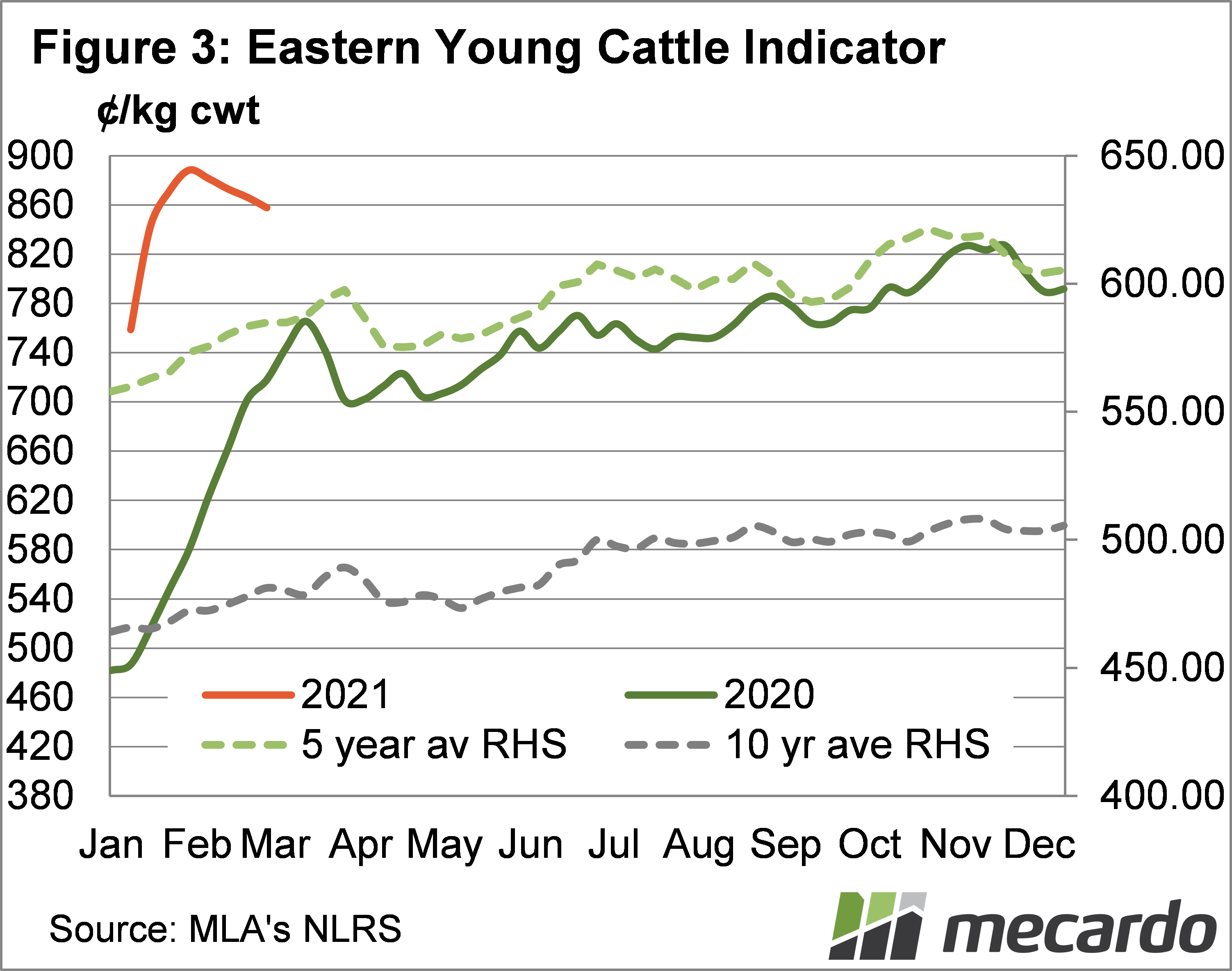

Prices seem to respond more to the May peak in supply rather than the February ones. Figure 3 shows the five and ten year average Eastern Young Cattle Indicator (EYCI) increase through January and February despite rising supply. Demand must be increasing in February, to push prices higher in the face of stronger supply.

The May supply increases do have an impact on price. Figure 3 shows that the five and ten-year average curves fall from April to May. Even with the average curves on a smaller scale, the changes in price look rather insignificant compared to the moves of 2020 and 2021.

Over the last five years, the EYCI has fallen 3.6% on average from April to May, and has fallen in 8 out of 10 years, with the largest decline being 13% in 2013. However, in 2015 the EYCI gained 12%, so prices can rise at that time of year.

What does it mean?

While there is a good chance cattle prices will ease as we move towards winter, there is a month or two before significant downside is likely, at least from the supply side. Given the state of the herd, and with a reasonable season forecast, price falls are unlikely to take the EYCI down below 800¢.

For producers looking to avoid downside, selling before or during April should save getting caught in a downtrend.

Have any questions or comments?

Key Points

- Cattle supply trends should persist even with the low herd and extreme prices.

- May traditionally sees the peak in cattle slaughter, and falling prices.

- Downside is unlikely to be large, but selling in April should see it avoided.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: MLA, Mecardo