The dry spring (in many eastern regions) has kept the pressure up on adult sheep sales to abattoirs in 2019. This article takes a look at what this means for the Australian flock size in the coming year.

Last June Mecardo looked the relationship between the sheep offtake (a rolling 12 month sum of adult sheep sold to abattoirs in Australia expressed as a proportion of the flock size) and the number of sheep in the flock. Varying sales of adult sheep is the main mechanism by which Australian (and New Zealand) farmers adjust their flock sizes. As the slaughter number is hard data, it provides a regular and reliable way to monitor what is happening to the flock size.

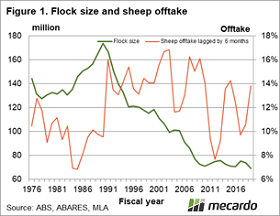

Figure 1 shows the flock size from the mid-1970s to last season (2018-2019) along with the sheep offtake lagged by six months (for example the rolling sheep offtake in December 2018 is lined up with the flock size in June 2019). The sheep offtake has some ability to project futures flock changes by 3-6 months. Note the low sheep offtake in the 1980s, as the flock grew to its peak 1990 level. As of last June, the lagged sheep offtake was still trading close to 14%, well into contractionary levels. It has eased in recent months but remains at 13.3% as of October.

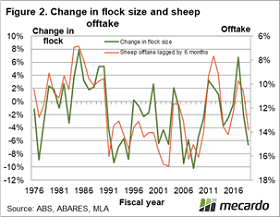

In Figure 2 the flock size is replaced with the year on year change in the flock size, and in addition, the sheep offtake axis has been reversed in value so it runs from small (expansionary for the flock) downwards to large (contractionary for the flock). This adjustment lines up the changes in flock size with the sheep offtake, not perfectly but to a substantial degree. The elevated sheep offtake as of mid-2019 is no surprise given the dry conditions and portends a smaller flock by mid-2020.

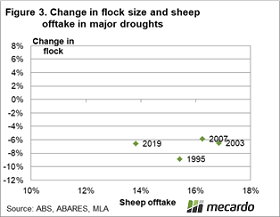

In Figure 3 the sheep offtake for the past four major spring failures (southern drought) since the mid-1990s is shown and compared to the change in flock size which was recorded in the middle of the following calendar year. The offtake varied from 14% to 17%, and the flock contractions ranged from 6% to 9%. It seems safe to say that the flock will contract by at least 6% this season and perhaps match the mid-1990s level of 9%. The 1990s were a time of reaction to the collapse of the Reserve Price Scheme, high greasy stock levels and deep cyclical downturns in wool prices.

Supply is now the opposite of that which held sway in the 1990s, which is reflected in prices of recent years and the continued outperformance of major apparel fibre prices by wool. However, the new condition is the back to back failed springs with the rolling 12 months rainfall rank looking like it could spend two consecutive seasons in the second decile, something unprecedented in the past century.

What does it mean?

Changes in the flock size are dependent on the sheep offtake which in turn is sensitive to rainfall. At this stage, it seems safe to assume the flock will shrink this season by at least 6%. Rainfall in the second half of the season will determine whether the shrinkage is well above 6%, more so than normal as the industry copes with two consecutive drought seasons (on average across all regions).

Have any questions or comments?

Key Points

- The sheep offtake remains at contractionary levels.

- The sheep offtake has some short term ability to project changes in flock size of 3-6 months.

- Shrinkage of the Australian flock in the current season is likely to be at least 6%.

Click on graph to expand

Click on graph to expand

Click on graph to expand

Data sources: ABS, ABARES, MLA, Mecardo