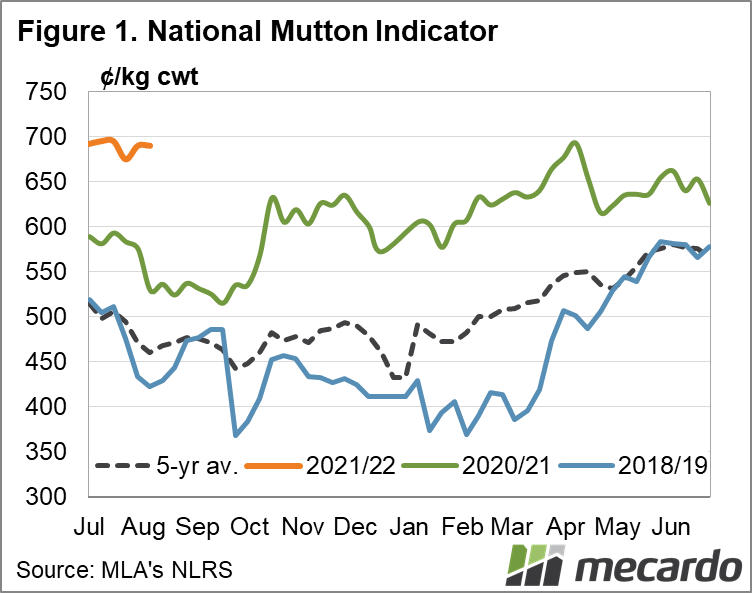

Mutton prices continue to outpace last year, despite supply having also increased. And while prices have come back slightly in the past week, returns are still historically high with spring right around the corner. Traditionally mutton prices experience a steady decline from now through to October, however strong export demand, a weak Australian dollar, and an abundance of grass could limit the fall.

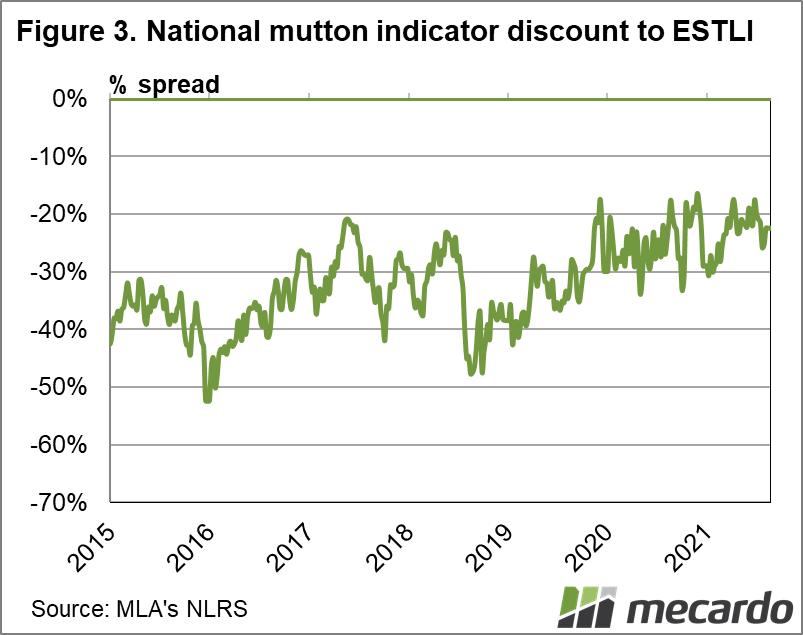

The National Mutton Indicator weekly average has been trading at about 100ȼ/kg stronger year-on-year for the past six weeks, which is close to 200ȼ/kg higher than the five-year average. The NMI’s spread with the Eastern States Trade Lamb Indicator is currently 22.5 %, having got back to 17 % in June. And it hasn’t broken into 30% or higher territory since January.

July saw the NMI reach a record monthly average of 688ȼ/kg, and for the first two weeks of August it was averaging 684ȼ/kg. In 2020, the NMI’s highest monthly average was 683ȼ/kg by March, and it dipped to a low of 530ȼ/kg in September – a 33 % fall. Historically, July is more often the peak month for the NMI, before the price falls from August to October. In 2019, the July to October NMI price spread was 7% lower, while in 2018 it was 17 %.

Medium over-the-hooks national mutton prices also reached new highs in July, at 654ȼ/kg, and are actually tracking higher for August data-to-date at 659ȼ/kg. Having peaked in June last year, the price lost just 5% for the spring, while in 2019 it fell only 6%. And in fact, if we go back five years to 2016, which seasonally was similar, the OTH mutton indicator actually rose 2% from July to October, with September the second-highest averaging month for the year (after December).

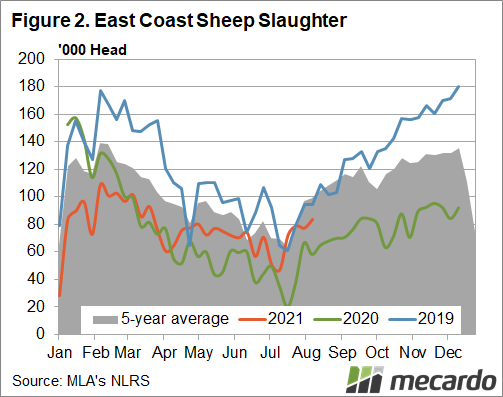

Slaughter is also up by 5% for the year-to-date, and yardings have lifted too – albeit less than 1%. Weekly sheep slaughter totals have been higher year-on-year since early April – last week by 29%. In the last week of July, sheep slaughter was only 1% below the five-year-average, and it was 110 % higher than the same week in 2020. Slaughter figures for sheep usually ramp up from now through to the end of the year, but Meat and Livestock Australia’s June projections had sheep slaughter falling by 6% for the year – which if correct would mean supply is running out.

As we discussed earlier this month here, concerns about labour shortages in abattoirs could start to impact throughput and therefore demand. With the full steam of spring suckers right around the corner, processors might be filling cold stores with mutton while they can before turning their attention to new season lambs.

What does it mean?

There’s money in mutton, and that’s unlikely to change dramatically for the remainder of this year. If processors do take their foot off the pedal in the sheep market, the seasonal conditions will surely put plenty of restockers back in the game looking to boost their numbers prior to joining, limiting the downward pressure on mutton prices – especially if supply dries up. . Plus, even if the NMI fell 33% over the next three months, as it did last year, it would still be above 530ȼ/kg – a price only achieved for the first time for mutton in 2019.

Have any questions or comments?

Key Points

- National Mutton Indicator reaches a record monthly average in July of 688ȼ/kg.

- Sheep slaughter up 5% for the year-to-date, with the weekly total up 29% year-on-year last week.

- Spring price dip to be limited by short supply, good grass and global trade conditions.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: MLA, Mecardo