The saleyards have opened the year slightly softer overall, although demand is still very strong and all indicators are still historically very high. The story of the week was low supply, with Covid again affecting supply chains across the board.

AuctionsPlus reported last week that cattle prices are continuing to ‘challenge record levels’. AuctionsPlus also reported the categories that dipped last week tended to be those ‘dominated by processor buyers’ as the new Omicron variant is impacting staffing numbers at processing plants.

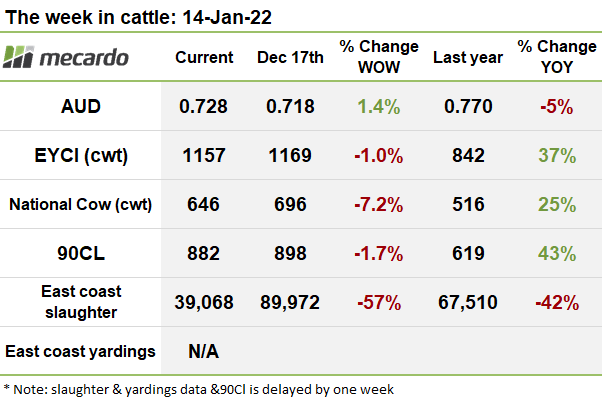

The Eastern Young Cattle Indicator (EYCI) has opened the year slightly down on where it finished 2021, currently sitting at 1157 ¢/kg cwt. The top saleyard contributing to the EYCI was once again Roma store, reflecting the strong demand from cattle producers in the north, contributing the most head of cattle (21%) at an average of 1240¢/kg cwt.

Dalby contributed 13% of EYCI eligible cattle and average prices there were 1143¢/kg cwt.

The 7-day rolling average of EYCI eligible cattle is just over 7,186 head, reflecting the overall low numbers this week in the saleyards.

Over in the west, the Western Young Cattle Indicator (WYCI) opened 20 cents higher on the end of 2021 and is now at 1150¢/kg cwt, with just over 2,000 head the total 7-day rolling average on offer there.

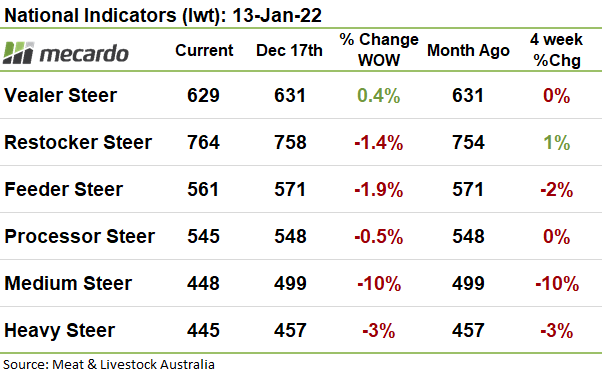

The National Indicators have all opened weaker on last year, bar the Vealer Steer Indicator which is 2 cents higher at 629¢/kg lwt. Medium steers are 10% lower than the end of last year, currently at 448¢/kg lwt.

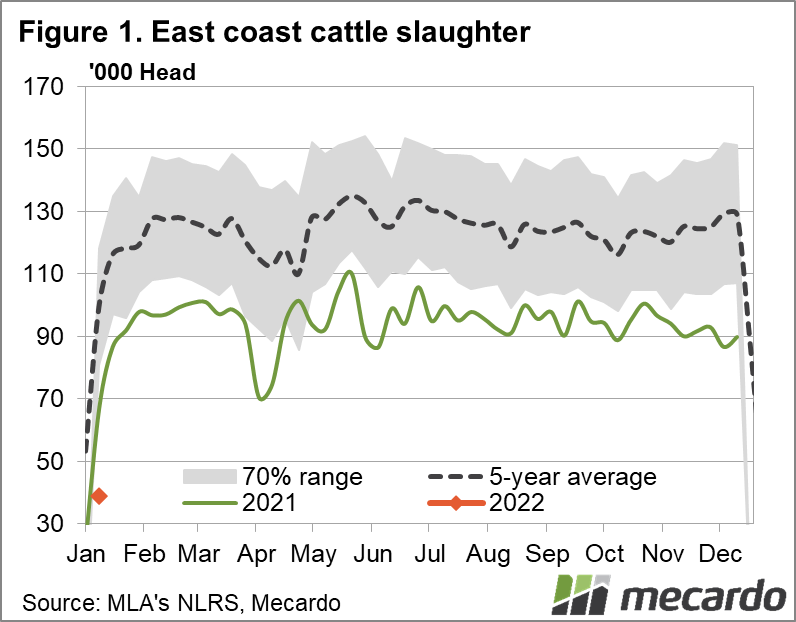

With cyclone activity up north, combined with Omicron disruptions to supply chains, there didn’t seem to be too many hurrying to the saleyards last week. Just 39,068 head of cattle were slaughtered for the week ending 7th of January 2022, over 50% lower than what was slaughtered in the last week of 2021.

The Steiner report from the US was a shortened holiday version this week with not much learn from aside from the 90CL price which, in AUD terms, dropped down 16¢ and is now sitting at 882¢/kg swt, as the AUD shifted marginally up (1.4%) to 0.718US.

The week ahead….

With plenty of grass in the paddocks and confidence in the season ahead we can expect much of the same story as last year, limited supply keeping price pressure on the red-hot cattle market. With more rain forecast to follow Cyclone Tiffany up north, the northern cattle market will continue to provide a solid base for sellers further south.

When (or if) Omicron disruptions settle, and supply increases, we should get a clearer picture of where the market is at.

Have any questions or comments?

Click on graph to expand

Data sources: MLA, Mecardo, BOM.