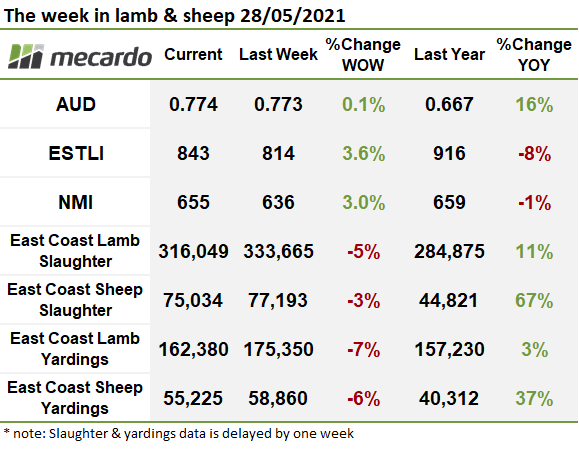

Simple supply and demand economics were in play this week, as softening throughput and slaughter provided a boost to prices. Trade and heavy lambs found strong support in most states, while store lambs failed to attract buyers.

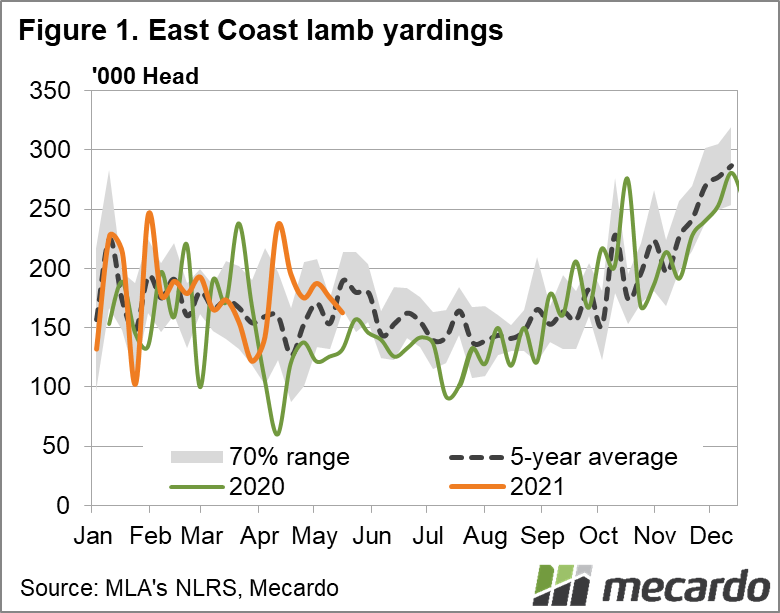

East coast lamb yardings dropped 7% last week, compared to the week prior, to see 162,380 lambs yarded. Throughput was down in NSW and Victoria, but when compared to the five-year seasonal average NSW lamb yardings were 22% below average, and 6% higher in Victoria. In WA 16,443 head were yarded which was a slight lift week on week but 15% below the seasonal average. Sheep throughput was also down in the east, with 6% fewer sheep yarded than the week prior.

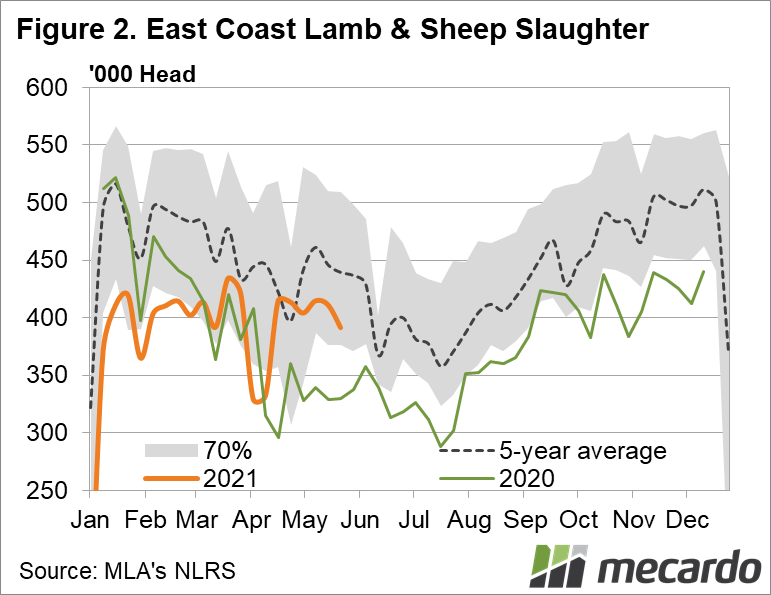

316,049 lambs were processed in the east for the week ending the 21st of May. This was a 5% drop on the week prior and 10% under the five year seasonal average.

The Eastern States Trade Lamb Indicator (ESLTI) picked up an extra 30ȼ on the week to end at 843ȼ/kg cwt. This time last year the ESTLI was 70ȼ higher at 913ȼ/kg cwt. In the West trade lambs also improved, gaining 24ȼ over the week to 719ȼ/kg cwt. A year on year comparison shows the Western Australian Trade Lamb Inidcator is also 70ȼ lower.

Strong processor buying saw the National Heavy Lamb Indicator lift 9ȼ over the week to 796ȼ/kg cwt. Heavy lambs are trading at about 76ȼ under the same time last year.

Restocker lambs lost the gains made last week, dropping 23ȼ to 847ȼ/kg cwt. They were hardest hit in South Australia and NSW where the Restocker Lamb Indicators dropped a massive 110ȼ in SA, and 80ȼ in NSW a single week. Light lamb prices also softened, the national indicator dropping 9ȼ to 765ȼ/kg cwt.

Lower sheep supply also helped to lift the muttom market. The National Mutton Indicator gained 19ȼ to 655ȼ/kg cwt. This is just 19ȼ below the same time last year.

The week ahead….

Earlier in the week on Mecardo we cunched the numbers on our spring lamb forecast. While demand remains good, spring supply is likely to be stronger this year than last and that means lower prices. But until then, we still have the seasonal winter peak as supply tightens.

Have any questions or comments?

Click on graph to expand

Click on graph to expand

Click on graph to expand

Data sources: MLA, NLRS, Mecardo