It has almost gone unnoticed, but November threw up some interesting figures for beef export markets. Supply continues to be tight overall, but the shifts in export destinations, while in line with seasonality, were much stronger than usual.

Regular readers will know that at the end of the day it’s beef export markets which drive Australian cattle markets. While the focus is currently on grass and weak cattle supply, without the money from export markets prices would be much lower.

The November export data released by the Department of Agriculture Water and Environment (DAWE) showed some dramatic shifts in export volume in November. Total exports were relatively steady, up just 1.85% on the October figure, at 75,712mmt, but it was in the detail where the interest lies.

Beef exports to the US were down dramatically, coming in 39% lower than October, and 14% lower than November 2020. Figure 1 shows exports to the US generally weaken in November, but this November they hit their lowest ‘non-January’ level since at least 1990.

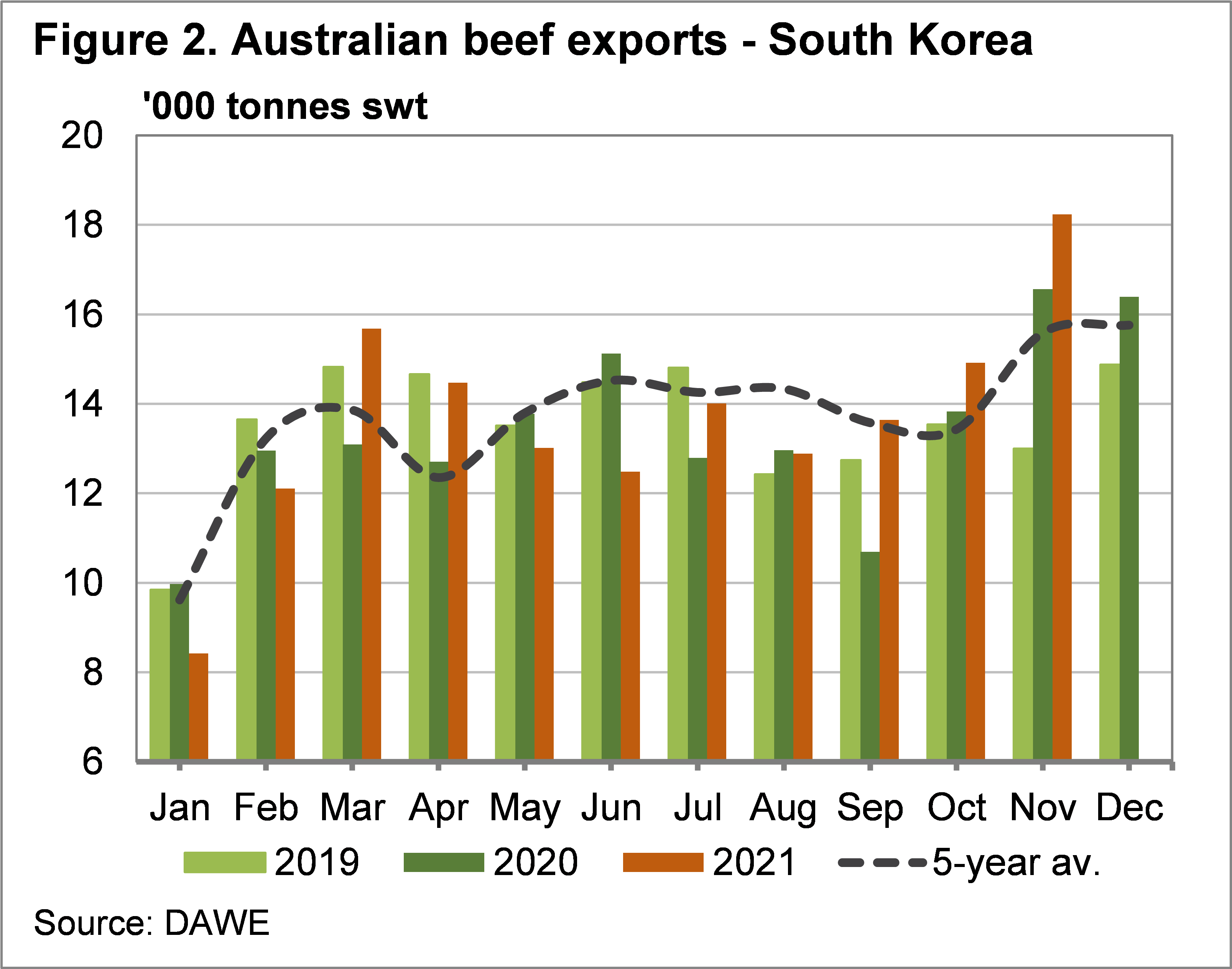

The beef which didn’t go to the US was taken up by South Korea and Japan. South Korean exports jumped by 22% on October, and 17% on last year, to record its highest total since November 2016, the only other time they have been higher.

Meat and Livestock Australia (MLA) have a good tool on their website for tracking exports, and it tells us that most of the increase to South Korea, and decrease to the US, was in frozen grassfed beef. The increase to Japan was largely frozen grainfed beef, which was diverted from the Philippines, one of the smaller markets.

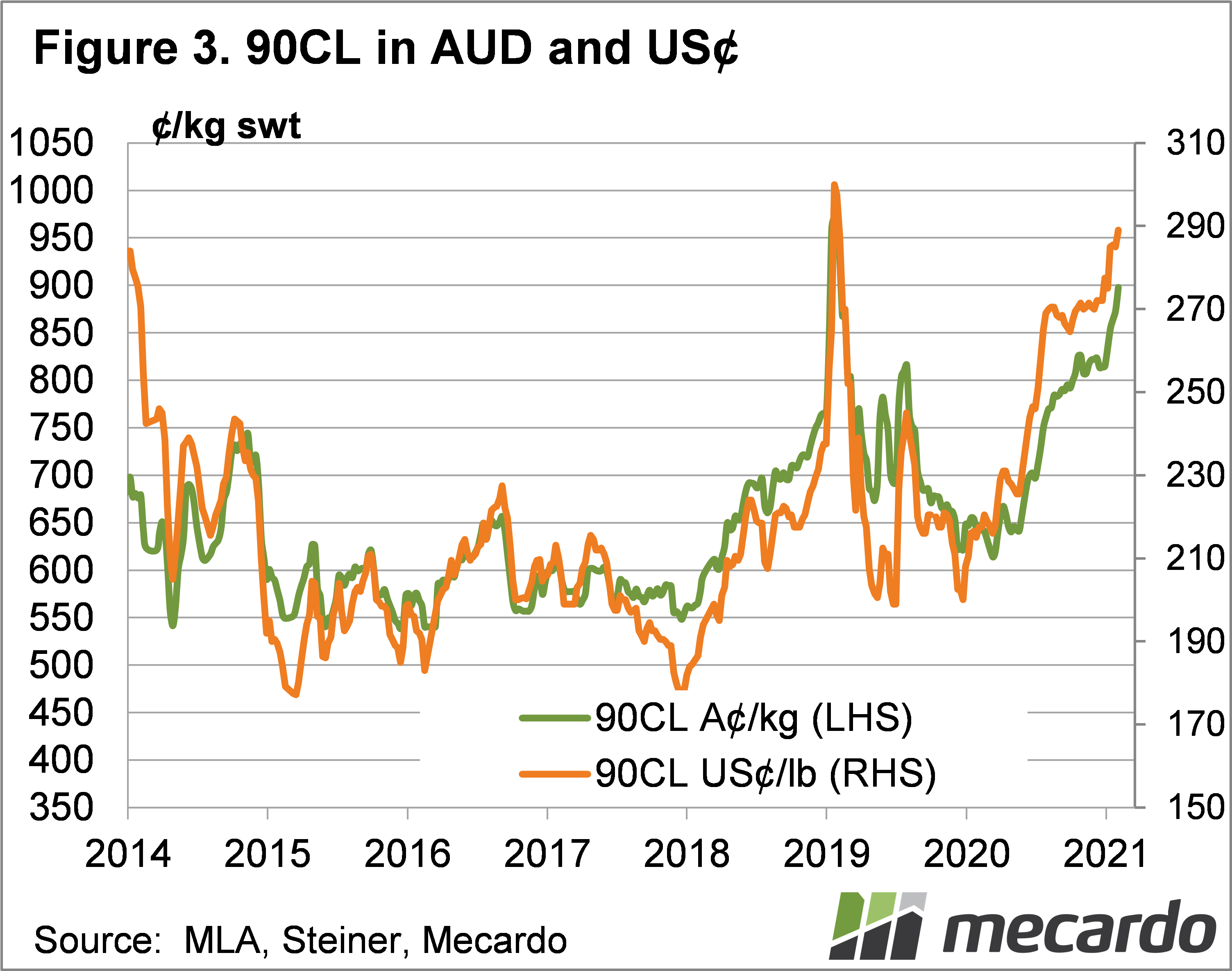

The seemingly increasing demand from South Korea forced beef export prices higher for manufacturing beef in November. Figure 3 shows the 90CL Frozen Cow export price to the US in both US dollar and Aussie dollar terms, and it has been on the rise.

In US terms the 90CL price is heading towards the record highs of 300¢ seen in November 2019, now sittng at 290US¢/lb. In our terms 90CL had gained 10% since the end of October, with some of the gain from a weaker AUD.

What does it mean?

With beef supplies relatively steady from Australia, at least on a national level, it is increasing demand which is again pushing prices higher. This should be taken with some caution however, with the New Zealand Cow culling season not far away, some pressure could come on the manufacturing beef market, which appears to be driving the beef export market in general.

Regardless of this it is good for growers to see higher export prices, as it keeps a floor in cattle markets when the inevitable shift in supplies comes.

Have any questions or comments?

Key Points

- Total beef exports were relatively steady in November, but US lost ground to South Korea.

- Korean demand for frozen grassfed beef was higher, pushing 90CL values to new records in our terms.

- The current higher prices might not last, but current strength is positive moving forward.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: DAFF, Steiner, USDA