The wheat (and broader Ag commodity) market stalled this week, falling in sympathy with a slow down in economic data. Adding to the tone, there has been some rain in the US Corn Belt, and while too late to build yield, it will allow the row crops there to finish off in style. The parched US Northern Plains and Canadian Prairies have also recorded some rain. Possibly it is nuisance value for some, for others it might halt the quality slide. For the market however, the fact it has rained seems to have provided the catalyst for profit taking

As I mentioned last week, the fundamentals have not changed. In fact Russian and Ukrainian FOB values for milling wheat are up 21% and 13% respectively (week on week) with Black Sea Feed wheat up a collective 18%. This is in itself problematic. While the Black Sea values are a reasonable proxy or indicator for global cash values, we are rapidly heading towards prices that spurred the Russian Gov’t into intervening with their Export Tax. Rabobank have suggested that the Russian Gov’t could “add extra measures to stabilise them”. Gov’t intervention rarely works and by limiting exports to keep domestic prices down, should only serve to tighten already tight global supplies.

The Northern Hemisphere wheat harvest is nearing completion. Ukraine is at 98% complete, with average yields of 4.62t/ha for an estimated wheat production of 32mmt (compared with 26mmt last year). Barley production is estimated to achieve 4.1t/ha for a record 10mmt produced. Canola is expected to achieve 2.7mmt, up 8% on the year.

French wheat harvest progress is slower than average but is approaching 95% complete. Recent rain has had an effect on quality with agricultural firm Soufflet announcing only 35% of procured wheat made milling minimum standards of 76kg/hL test weight. The perceived lack of milling quality is causing havoc at export level, as traders scramble to fulfil commitments. The MATIF milling wheat contract jumped $7/t overnight over these concerns, and will fuel the gap between milling and feed quality wheat.

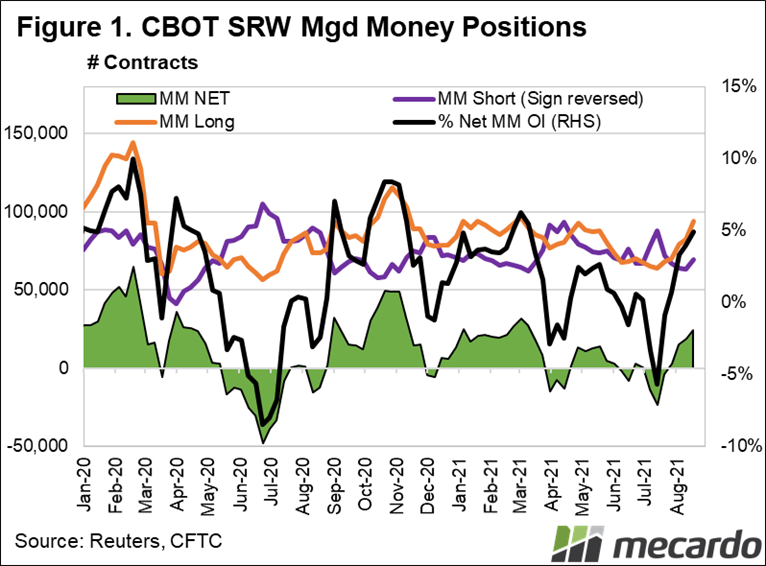

Lastly, as a gauge of whether or not the market has reversed direction, I take some comfort from the managed money (speculator) positions. In recent weeks they have increased their long (BOUGHT) positions in CBOT, which is usually a sign that in the short term at least, they are waging that prices will continue to increase.

There continue to be many moving parts in the wheat market. As the Northern Hemisphere harvest wraps up, focus will turn to Australia and Argentina. The latter is already coming under the spot light with back to back La Ninãs forecast. This years La Ninã dramatically cut precipitation across Southern Brazil and Argentina. The window for seeding is starting to open for soybeans and corn with the dry season officially over on the 15 Sept. Dry conditions recently after a very dry first half of the year will have the market nervous until rains materialise. There is still plenty of time, but given the tightness of stocks, the market is relying on a bumper South American season.

Next week….

The wheat market will likely remain volatile in the short to medium term as we trade the risks to production versus a buyer who is already citing high prices. Also, expect the spread between milling wheat and feed wheat to continue to widen. With a wetter than average forecast for SE Australia, supplies of high protein wheat are expected to get very tight.

Have any questions or comments?

Click on graph to expand

Data sources: USDA, Reuters, Argus Commodities