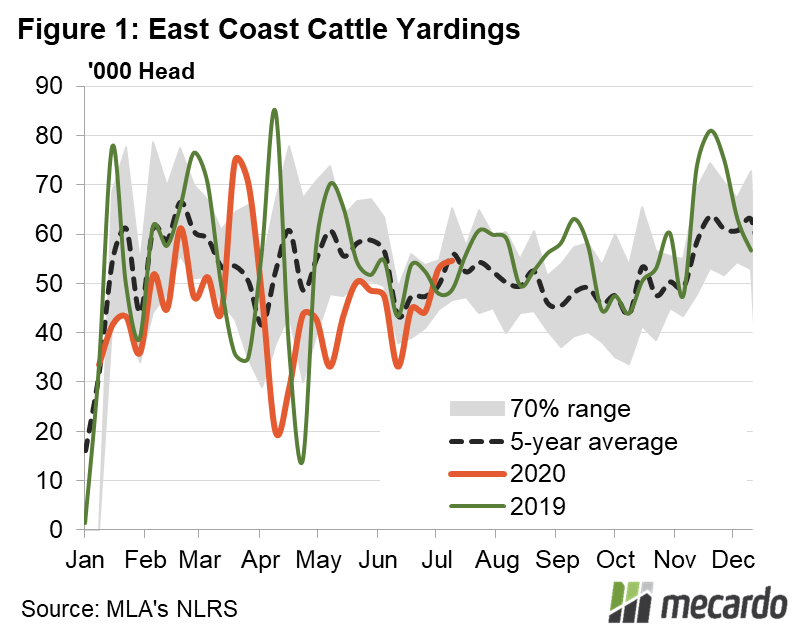

The eastern cattle market continues to be a story of the heady prices being supported by low supply and pent up export demand from burger-loving consumers in the US and higher household food shortages. Although, that demand is held under some constraint by processors unwilling to pay more than the already elevated prices. The dismal yarding numbers seen recently have tracked upwards, but history shows that yardings tend to stabilize or drift downwards until the usual November surge.

While prices and export volumes for US grinding beef have lost ground recently (view here), US manufacturer demand historically rises sharply through October & November in preparation for the thanksgiving holiday season. This, coupled with pessimistic MLA forecasts (view here) for slaughter off the back of tight supply in Australia should help support price in the near term.

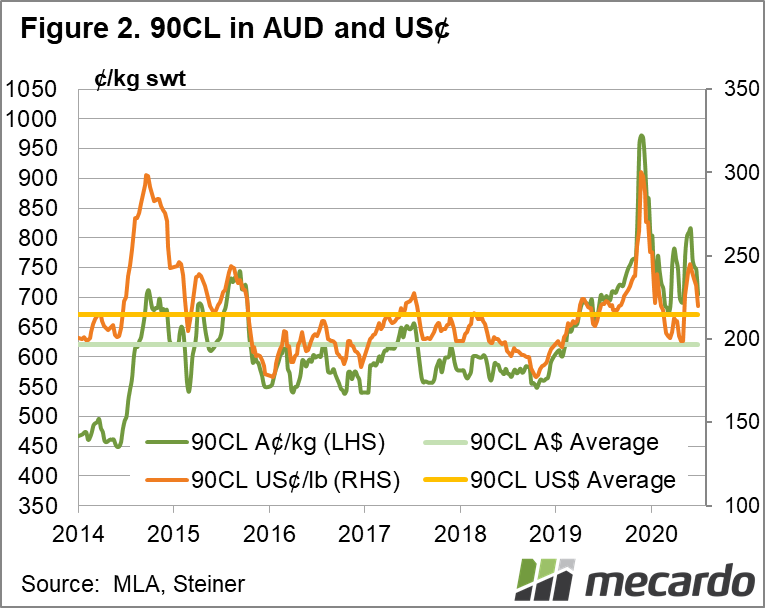

The benchmark 90CL frozen beef price has bounced around violently in recent weeks, pushed by US economic reopening , but despite tracking lower overall, it still sits at levels above longer term USD averages. US domestic 90CL remains priced at a 5% premium to the Australian product, suggesting US processors will continue to source cheaper Australian product if they can.

USDA data indicates that US household food shortages are still tracking at elevated levels that are almost double that of peak 2018 levels, with 9.7% of US households, or 31.5m Americans reporting being unable to buy enough to eat in June. With unemployment benefits boosted by $600+ USD per week currently, open to even the previously ineligible, it seems unlikely that this stems from poverty.

Large USA corporate burger chains such as McDonalds and Burger King have reported sales recovering to within 5% of pre- COVID-19 levels, as they have successfully adapted their business model in response to ongoing COVID-19 conditions. Ground burger beef accounts for 40% of the USA’s domestic beef consumption, and requires largely imported lean beef on a 1:1 basis to make burgers.

Major Brazillian processors such as Mafrig group were recently granted access to the USA market. However, Brazillian beef accounts for less than 5% of US imports, and is unlikely to gain internal approval from USA corporate buyers such as McDonald’s and Burger King, currently supplied by Australian product.

Successful reopening of US processors in mid-June, such as Tyson foods; the world’s second largest processor of meats, have led to increased slaughter capacity in the USA, putting pressure on aggregate import demand.

Future downside pressure on US demand for imported Aussie beef exists, with extreme US stimulus such as the $600USD a week unemployment supplement provided under the CARES act expected to be unwound and replaced in August with less generous schemes.

What does it mean?

Prices for finished cattle are currently being stabilized by extremely tight seasonal winter supply. Cattle prices are at levels that pressure processor margins, constraining both slaughter numbers and export volumes. With processors paying top dollar for cattle, we can expect that saleyard prices will be tightly pegged to the export situation. Promising US burger sales figures, coupled with expected thanksgiving & holiday manufacturer demand should provide support to US import prices. However, downside risk looms imminently, with USA stimulus measures tailing off in August, which may impact beef consumption.

Have any questions or comments?

Key Points

- 31.5 million Americans report not being able to buy enough food, but burgers chains are driving ground beef demand.

- Tight supply now, before the usual November jump.

- Beef Export supply constrained by high saleyard prices, squeezing processor margins as processors compete with restockers building herds.

Click on graph to expand

Click on graph to expand

Data sources: MLA, McDonald’s USA, Restaurant Brands International, US Census, Steiner report, US-NCBA, Mecardo