Just when we thought world beef markets had been as tight and disrupted as possible, Brazil pops up with a couple of cases of BSE. Today we look at beef exports, and export values, and see supply and demand converging to push prices to new records.

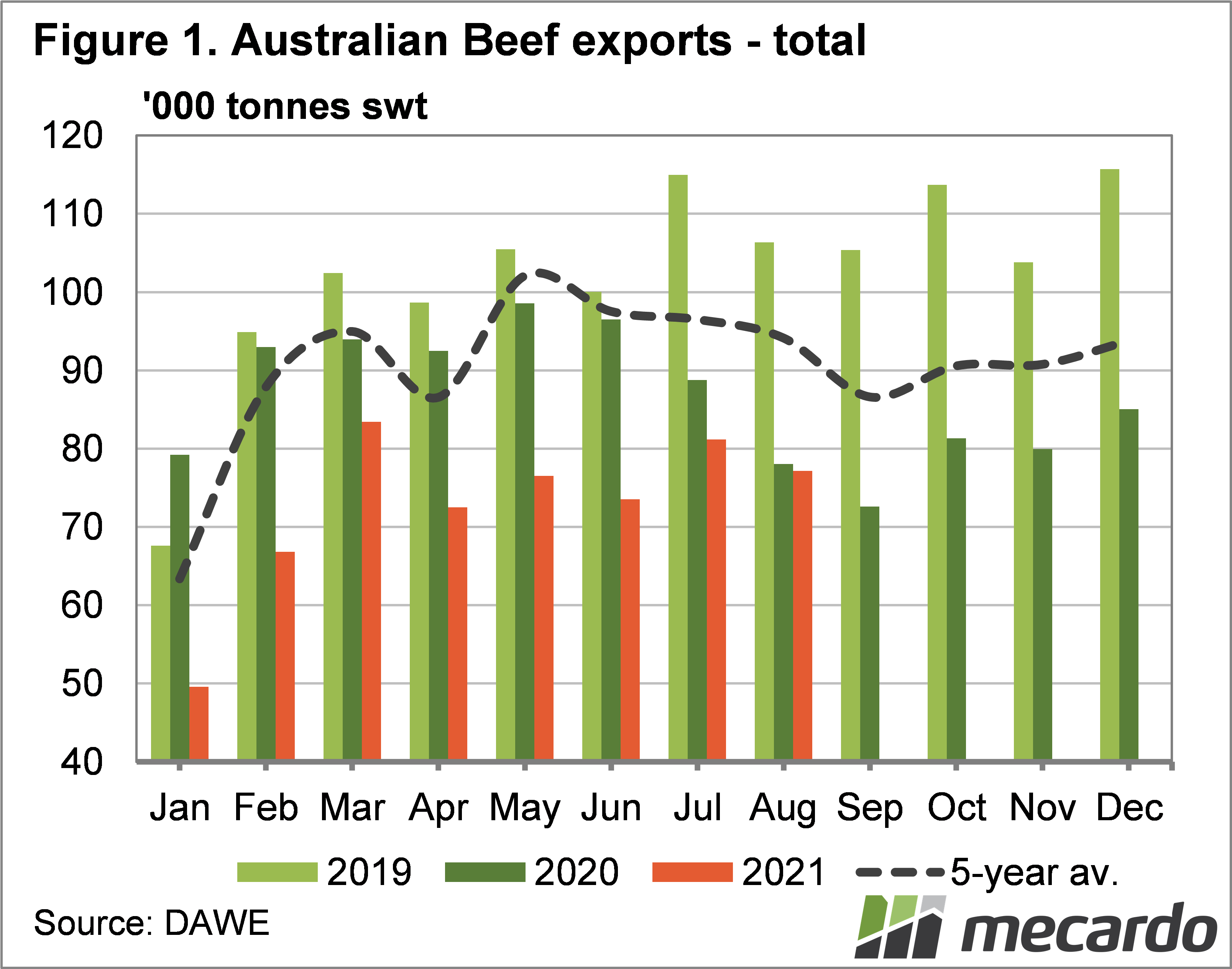

August beef export data was released last week, and it came with few surprises. Beef exports generally decline in late winter and early spring, and this trend held true with total exports down 5% on July, but it was still the third-largest month for the year (figure 1). Compared to 2020, beef exports were down just 1%, with tight supply now impacting markets for over 12 months.

Month on month exports to Japan and South Korea were much weaker, while the US and China took a similar amount. The dearth of cow and lower quality beef available saw US exports down 26% on last year, which help explain the rising value of 90CL as outlined last week.

Australian beef exports to China haven’t really moved with the Argentinian export ban on certain products, and subsequent restrictions, probably more through availability issues than demand.

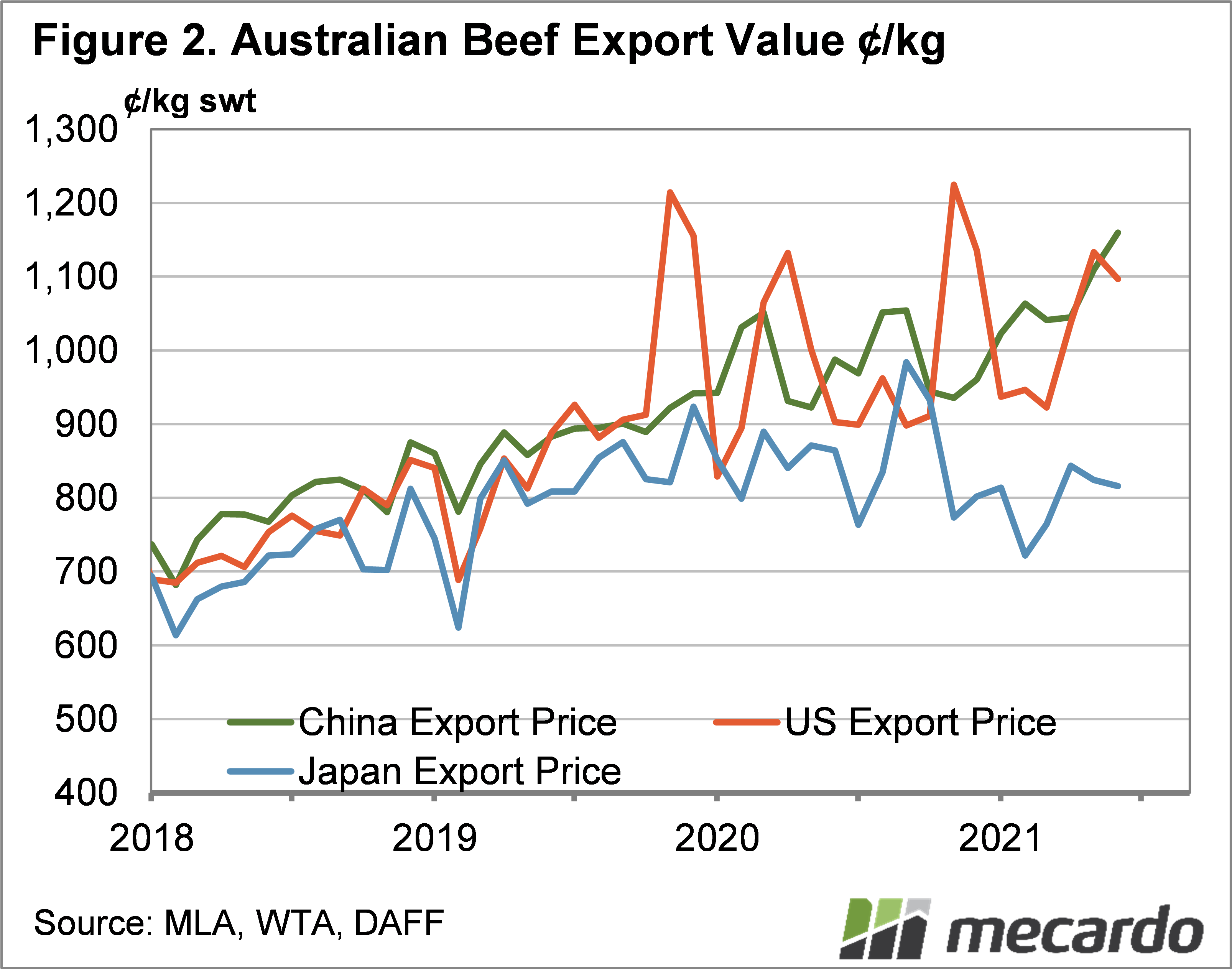

We can see in figure 2 that beef export values did react in June (the latest data), with Chinese per kilo beef export value hitting a new record. China’s average price of Australian beef hit $12 per kilo in June, a record high, surpassing the $11.83 seen in August 2020. When prices rise while volumes remain steady it suggests demand has increased.

US beef export values have been similarly strong, but it has been stronger in the past when 90CL prices have been hitting extremes. Demand has been stronger out of the US, but part of this is seasonal, which could wane as the US moves into the colder months.

It’s interesting to see beef sold to Japan priced lower on average than the US and China. This is likely to have something to do with the variety of cuts exported to Japan.

What does it mean?

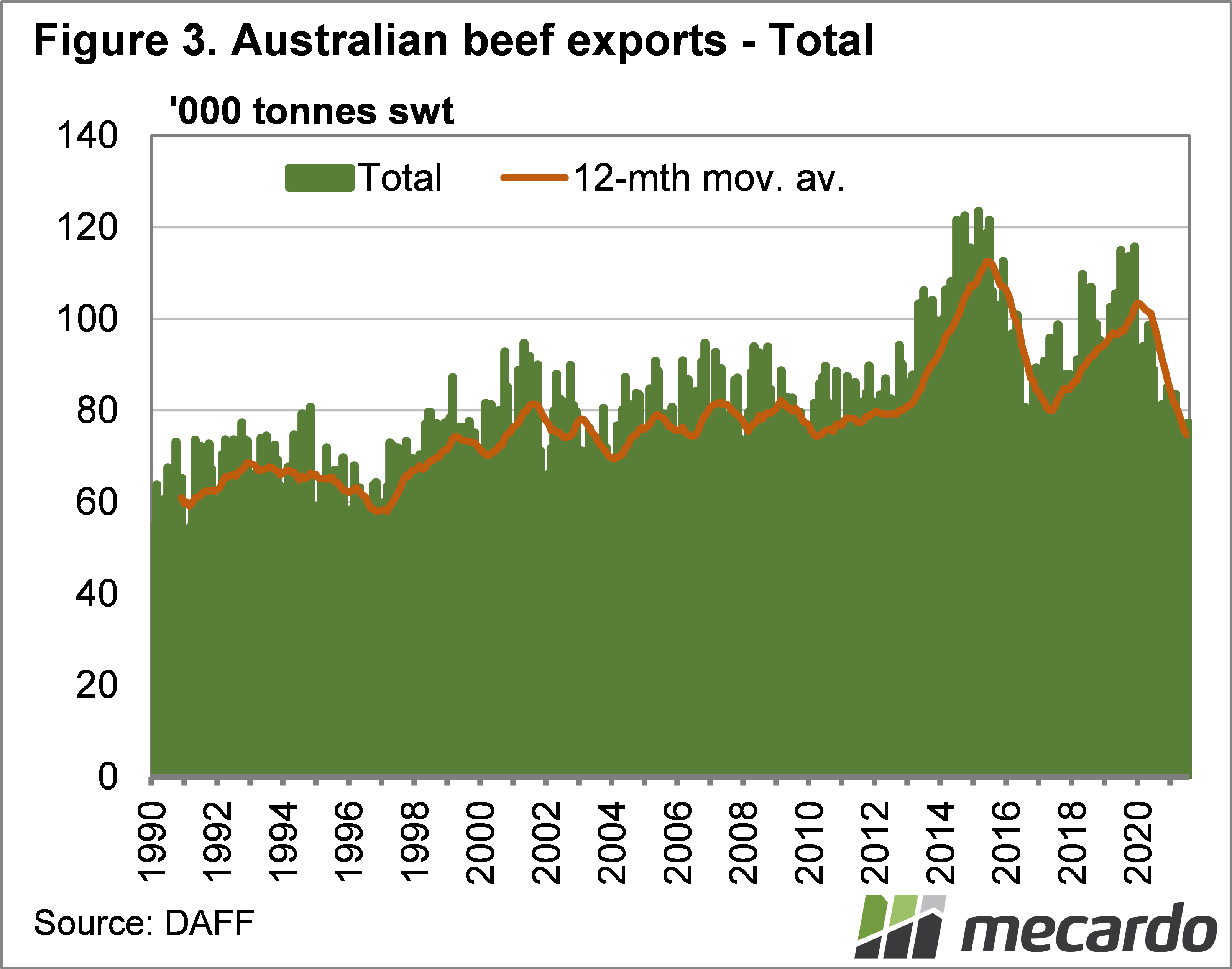

Figure 3 shows the massive decline in beef exports over the last 18 months. With such a decrease in supply, some markets had to suffer, and it looks like it has been the US and China who have received less beef.

There is little prospects of a rapid increase in supply and exports like the two rises seen in 2013 and 2018. Even if seasons deteriorate, there is unlikely to be the volume of stock to move exports higher.

Demand should remain strong across our major markets, even with reports that trade is soon to resume from Brazil.

Have any questions or comments?

Key Points

- Beef exports were lower in August, but for 2021 to date they were relatively strong.

- While exports to China haven’t risen, values have gained ground on improving demand.

- Exports are heading to the bottom of the curve, but are unlikely to rise quickly

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: DAWE, WTA, MLA