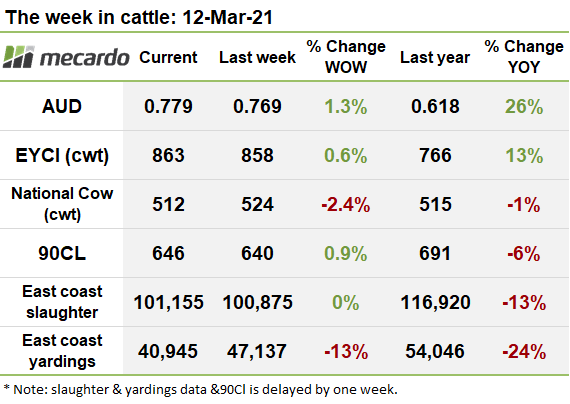

Another week of below average yardings and low slaughter has finally produced a small uptick on the EYCI this week. Feeder and processor prices lifted, however, the heavier side of the market suffered, with medium cows and steers dropping back, along with heavy steers. The Aussie dollar has also strengthened on the back of higher expected US inflation and rallying commodity prices.

The uptick in yarding’s reported last week couldn’t be sustained, with numbers on offer dropping by 13%. VIC and QLD drove the change, falling 23% and 17% respectively.

A total of 40,945 head were yarded on the east coast for the week ending 05th March 2021, which was 6,192 fewer than the prior week, and 28% down on the 5-year average.

Slaughter remained fairly stagnant last week, but it’s still running at 24% below the five-year average, so kill rates are still struggling along.

For the week ending 5th March, 2021, 101,155 head were slaughtered, which is up a measly 280 head on the week prior, but 32,000 head less the 5-year average.

The EYCI finally made a sluggish, but welcome move upwards, putting on 5¢ (<1%) for the week to reach 863¢/kg cwt. If low slaughter and low yarding’s continue to support the price, we can probably not expect much more news on this front.

Moving across to the west, the WYCI is in star territory though- at 937¢/kg cwt, it’s sitting proud at a 9% premium to the EYCI, and is up 34% on the same time last year.

The national category indicators were a mixed bag, weighed down with negative movements on the heavier side of the market, and vealers saw their first price fall in quite a while, however processors and feeders finished up in positive territory.

Medium Cows took the biggest fall, retreating 8¢ (3%) to 276¢/kg lwt. In the same spirit, Medium and Heavy Steers suffered a stumble, respectively giving up 5¢(1%) and 6¢(2%) to settle the week at 384¢/kg lwt; and 364¢/kg lwt.

Processors and Feeders were a more positive story however, both adding 5¢(1%) to end the week to finish at 450¢/kg lwt and 443¢/kg lwt.

Restockers were relatively stable, backing off just 1¢ (1%) to 519¢/kg lwt, continuing the decline since the highs seen in mid-January, when prices were 7% higher at 560¢/kg lwt.

Vealers also took their first tumble for a few weeks, losing 4¢(1%), easing back to 502¢/kg lwt, but the upward charge they have been on from the $4 mark last August still has solid fundamentals behind it as very young cattle are just too valuable to slaughter early.

The Aussie dollar rose strongly by 1.3% to tick up to 0.779US. Biden’s generous, and possibly overdone 1.9 trillion-dollar stimulus plan has expectations of US inflation leaping upwards. American households earning less than 150k will all receive a $1400 boost as part of the plan. Strong commodity prices have also boosted demand for the Aussie dollar. The 90CL saw a little rise, adding another 6¢ (1%).

The week ahead….

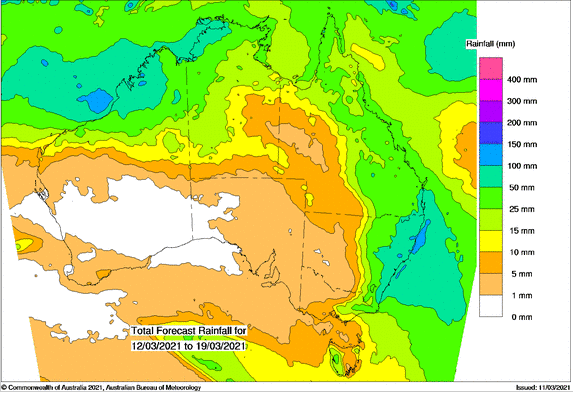

It’s still looking pretty dry going into autumn for NSW and VIC, with only a sprinkling of 5mm expected to come through. Sunny QLD is a very different story though, with a solid 25-50mm expected to come down the coast over the next week.

Historically, yardings tend to trend downwards this time of year, and the slack to rising pricing situation we have this week suggests there will be more of the same on offer, particularly for young cattle. Next week we can expect some more good support from low supply coming up.

Have any questions or comments?

Click on graph to expand

Click on graph to expand

Click on graph to expand

Data sources: MLA, Mecardo, BOM