The world has had a very sharp reminder of the power one man wields. Vladimir Putin has in the past week flexed his autocratic muscle more than once and made the world a far less certain place.

Last weekend, Russia cut the Nord Stream gas pipeline that supplies 40% of Europe’s natural gas requirements indefinitely. The cuts and restrictions to gas flow leading up to this, have only hinted at the repercussions that the Europeans are now facing. There have already been examples of manufacturing plants that have had to close or at least reduce their output citing the exorbitant cost of inputs. The implications for Europe are huge. Over the past decade, an environmentally sensitive awareness has pervaded the governing parties which has seen nuclear power plants and coal fired energy mothballed in favour of lower emission renewables and natural gas. The severing of Russian gas leaves the EU27 bloc of countries extremely vulnerable to soaring energy costs, a major economic recession and a very cold winter.

Perhaps more relevant to ag commodities is the latest rhetoric coming out of the Kremlin. I suspect the world has been lulled into a sense of relief that the Black Sea grain corridor has held up and we are seeing exports out of Ukraine start to pick up pace. The success of the corridor is seen as requisite to help avoid a potential food crisis particularly in the Middle East and North African regions. The corridor has if anything, brought the cost of food and feed down from the highs seen mid May.

As always though, the devil is in the detail. The initial agreement was for a period of 120 days – with a view the agreement could operate in perpetuity providing all parties agreed. Over the past couple of days, the Kremlin has voiced ‘outrage’ that the grain flowing from Ukraine is not going to those who desperately need it, but is in fact going to Europe (historically a major market for Ukraine). Last night Putin has doubled down on his faux outrage, insisting that the deal will not be extended unless there are limits to where Ukrainian grain is exported to. Five weeks into a 12 week deal, the corridor appears to be on shaky ground.

The claims of being ‘cheated’ coming from Russia rings a little hollow but is perhaps more about a perception of Ukraine exports seen to be ‘helping’ NATO countries but also because Russian market share and export pace is not running as hot as expected.

The week ahead….

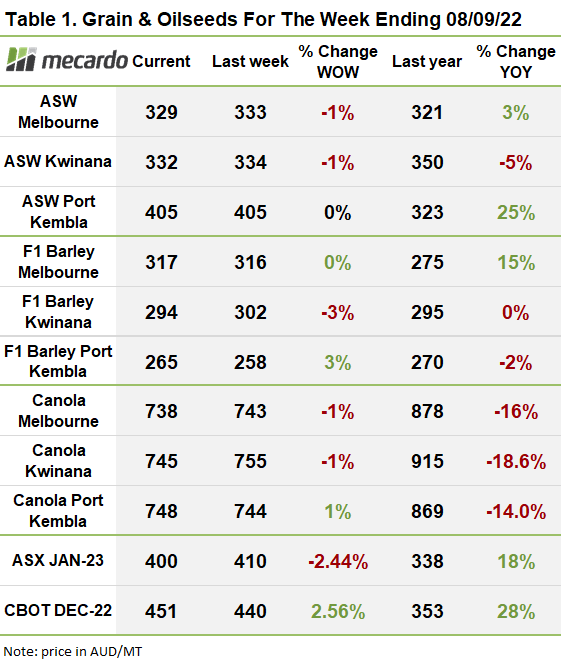

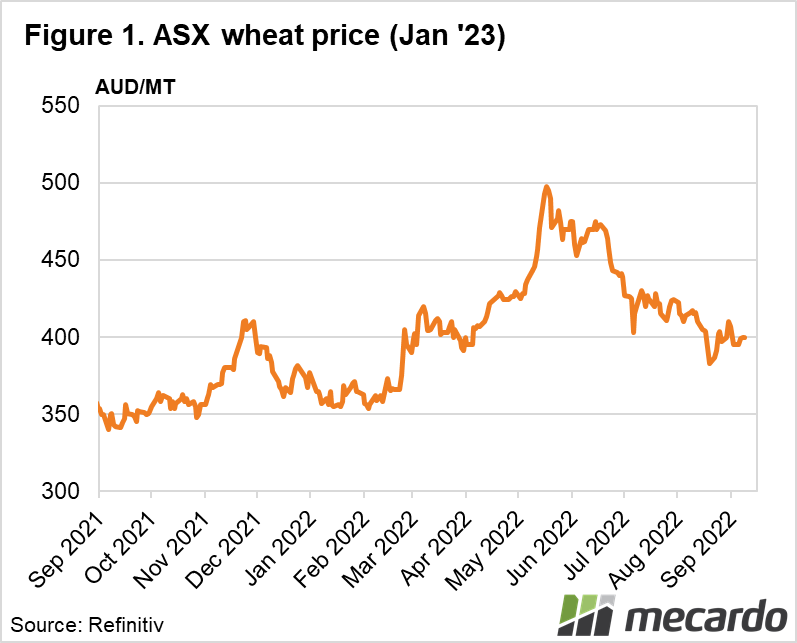

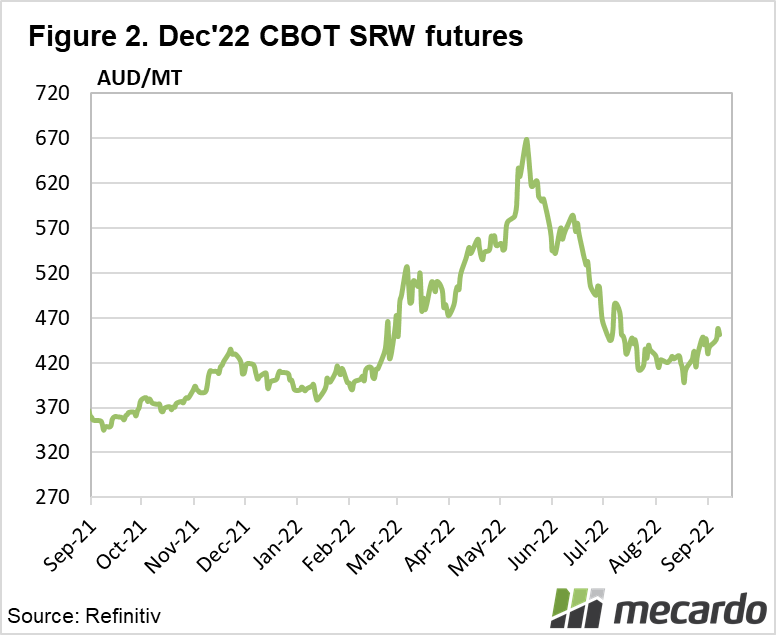

The initial response in the wheat market was to climb 4%. The following days dialogue will determine if the market continues to climb or settles down. Watch for the USDA S&D report due out next week which will also provide some direction in the corn and bean market.

Have any questions or comments?

Click on graph to expand

Click on graph to expand

Click on graph to expand

Data sources: SovEcon, Reuters, Top Lead