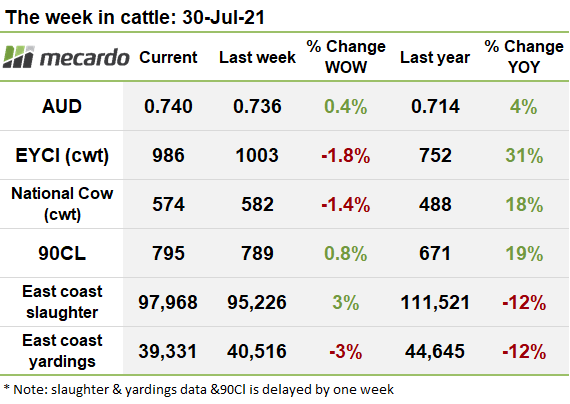

No new records set this week, the EYCI has fallen, but fortunately not to an earthshattering degree. However, the heat seems to have come out of the market in the key saleyards of Roma Store, Dalby and Wagga. On the brighter side, the processor and medium cow indicators lifted.

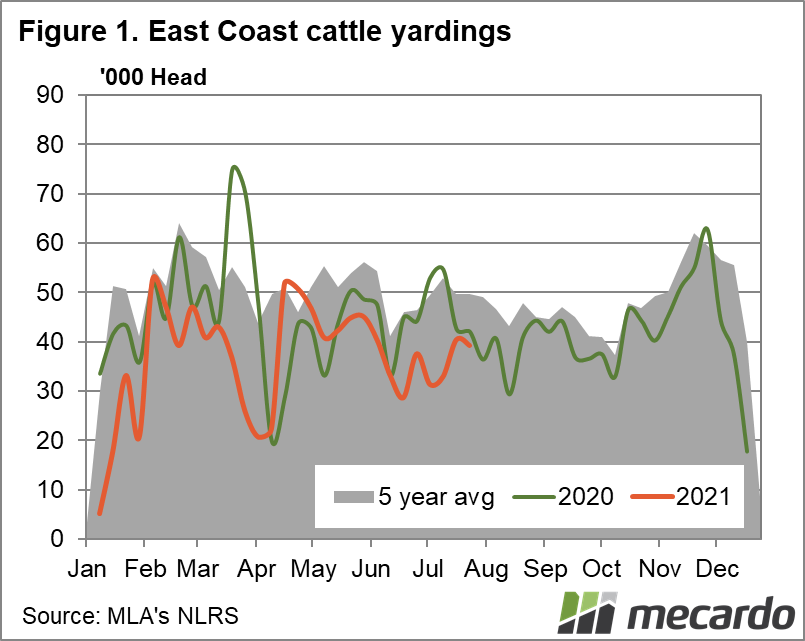

Yardings dipped slightly last week, with volumes down 3% on the week prior. Although, it was a situation of swings and roundabouts, with southern offerings from VIC and SA plunging 30%, almost entirely offset by an increase in QLD. A total of 39,331 head were yarded on the east coast for the week ending 23rd of July, 2021 down 1,185 head from the week prior.

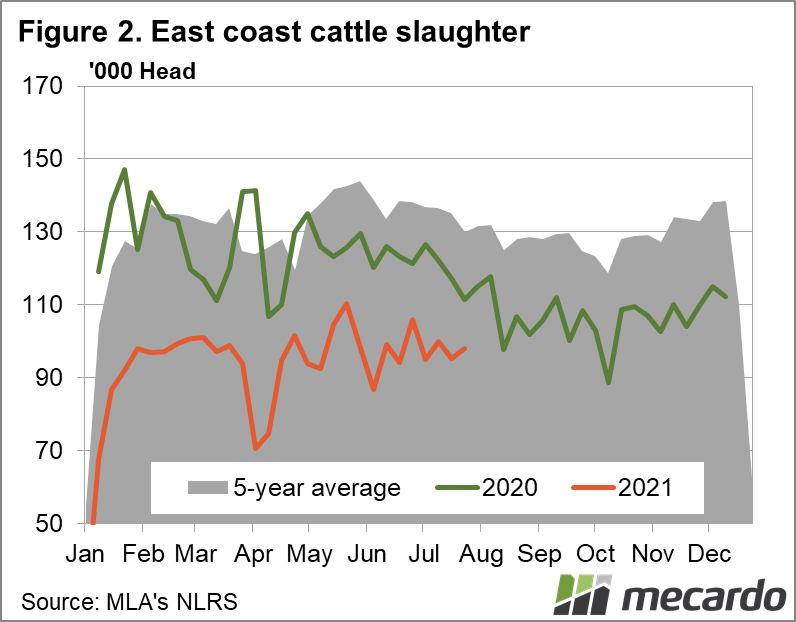

East coast slaughter picked up a smidgen last week, gaining 3%. 40% of the net increment emanated from VIC, and 44% from NSW. In total 97,968 head of cattle were slaughtered in the week ending the 23th July 2021, which was up 2,742 head on the week prior.

The EYCI stumbled slightly this week, shedding 18¢(2%) to come to rest at 986¢/kg cwt. This is despite supply being more constrained, with eligible cattle volumes comprising the EYCI down 18% on the prior week. Prices at the key marketplace of Roma store were down 30¢ to 991¢/kg cwt, while Dalby and Wagga prices also slipped to 965¢/kg cwt and 992¢/kg respectively. Overall, saleyard prices were softer than last week, with only four saleyards averaging prices over 1,000¢/kg- Casino, Singleton, Forbes and Scone, across a total volume of only 1200 head. Processor buying activity lifted, from 7% of the index last week to 10%.

The national indicators were a mixed bag of results, with processor and medium steers benefiting the most, while restockers and cows fell. Processor and medium steers gained 9¢(2%) and 8¢(2%), respectively, settling at 515¢/kg lwt and 447¢/kg lwt. Feeders also lifted by 5¢(1%) to end the week at 595¢/kg lwt.

On the downside, restocker steers dropped 8¢(1%) to 595¢/kg lwt, and cows followed suit, falling 4¢(1%) to 310¢/kg lwt. Heavy steers slipped a fraction, losing 1¢(,1%) to end the week at 426¢/kg lwt.

The Aussie dollar appreciated 0.4% for the week, lifting to 0.736US thanks to a weak US dollar, impacted by lower than expected GDP growth figures.

US 90CL frozen cow prices lifted 6¢(1%) to 795¢/kg swt, mostly on the back of the depreciation in the AUD, as prices actually slipped 1¢ back for the week to 265¢/klb in USD. Steiner consulting suggests that present prices are somewhat reflective of what was paid for existing inventory, as opportunity to buy new stock of Australian beef is limited in the US at the moment.

The week ahead….

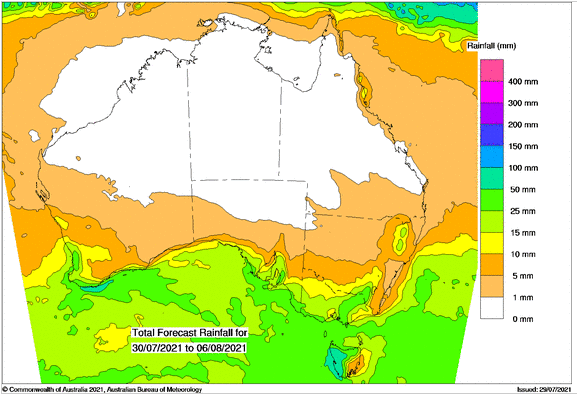

Similar to last week, down south is set to receive a good dose of rain over the week ahead with VIC likely to get 25-50mm in many areas, while QLD and NSW mostly miss out. The fall in the EYCI from its high perch, combined with softer restocker prices might just attract a few more sellers out of the woodwork, but equally, buyers are likely to step in, supporting prices, so next week could well prove to be fairly uneventful.

Have any questions or comments?

Click on graph to expand

Click on graph to expand

Click on graph to expand

Data sources: MLA, Mecardo, BOM