Last week we touched briefly the relationship between biodiesel production and world demand for oilseeds. Today we take a closer look at what is driving the biodiesel market and what it might mean for Australian canola producers.

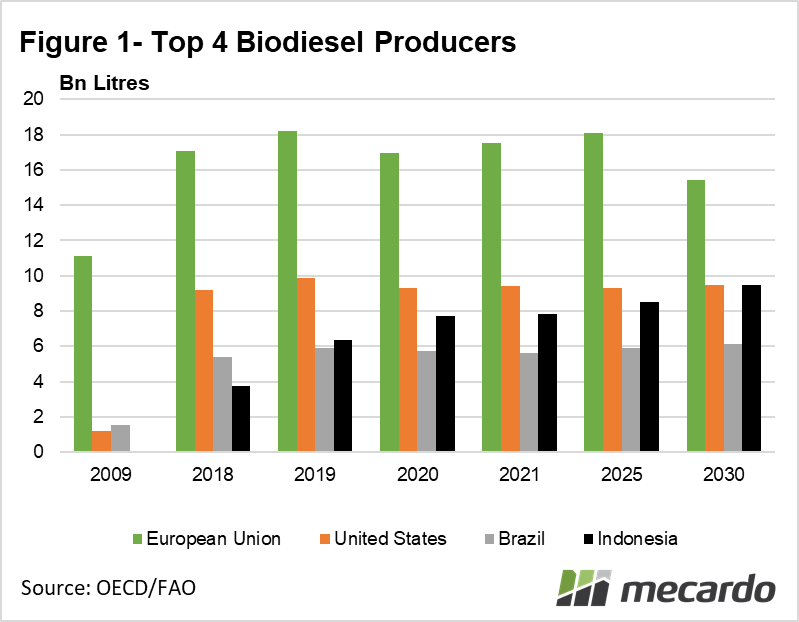

World biodiesel demand and production is supported by various mandatory government renewable fuel policies. The top four producers of biodiesel in the world are the EU, US, Brazil, and Indonesia (figure 1), but the feedstock mix varies considerably between producers.

The four primary fat source feedstocks utilized for US production in 2020 were soy oil (62%), corn oil (11%), canola oil (9%) and used cooking oil (UCO) (7%). In the EU, canola (42%), UCO (20%) and palm (17%) oil dominate. Indonesia exclusively uses palm oil, while Brazil utilizes soy oil (84%) and animal fat (16%).

From an Australian perspective, the EU is the most relevant biofuel market to consider, as in 2020, it utilised 6.1mmt of canola oil as biodiesel feedstock – the equivalent of 16mmt of canola seed. However, the indirect impact world biodiesel demand has on the overall oilseed complex, and hence canola demand and prices is significant.

When we consider biodiesel production, we can effectively translate biodiesel production back to its vegetable oil equivalent, and by proxy, the corresponding equivalent demand in metric tons for oilseeds further up the supply chain. Around 2.6 tons of canola seed at 40% oil content, or 5.25 tonnes of soybeans at 20% oil content is required to produce one tonne of biodiesel at 95% process efficiency. Figure 2 represents world biodiesel demand in terms of the required equivalent tonnes of canola and soy seed needed to produce it. Using this rough comparison, (and ignoring oil-meal byproducts) we can say that in canola equivalent terms, biodiesel production is the equivalent of 20% of world oilseed production tonnage, or 40% of tonnage in soybean terms.

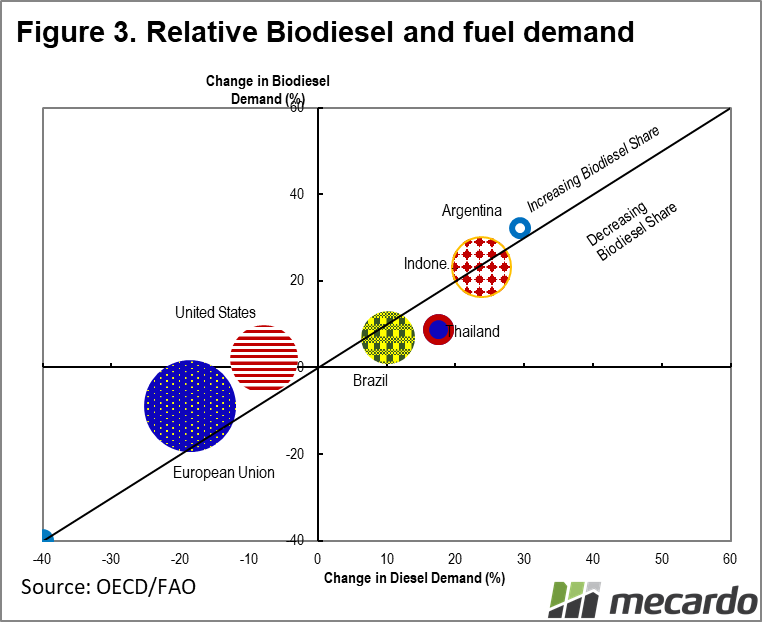

Biodiesel demand is an important component of total world oilseed consumption. Growth of around 5% is expected from this market in the next decade, reaching 51 billion litres. Looking closer at the expected trajectory of the EU’s requirements are predicted to contract in line with a general trend towards a lower requirement for transport fuels, while the US situation is expected to be similar (figure 3). Counterbalancing these losses are increasing needs from the developing world such as Brazil and Indonesia as their overall transport energy requirements grow, and along with it, biodiesel demand by way of their renewable fuel blending mandates of 13% and 30% respectively.

Of special interest to Australian canola producers, is that palm oil is considered a source of potential environmental damage. The EU is phasing out the use of this biodiesel feedstock by 2030, of which it consumed 2.4mmt annually, and is moving towards other alternatives such as canola. In addition, Indonesia may implement a more aggressive 40% blending standard for diesel fuel which has the potential to add significant volumes to world vegetable oil demand, as it intends to drive the country to consume 14.2m KL, or 12.5mtpa biodiesel by 2022 to reduce dependence on imported fossil fuels. This more bullish scenario is not encompassed in the FAO forward estimates out to 2030, depicted in figure 1.

What does it mean?

When considering the longer-term prospects of oilseed production, including canola, future biodiesel demand is an important factor to take into account. Biodiesel demand is largely influenced by the renewable fuels policy settings in various countries, as well as overall transport fuel requirements. With the EU looking to move away from palm oil use, likely underpinning canola demand by up to an extra 6mmtpa, or 30%, and Indonesia intending to aggressively ramp up palm oil use in biodiesel if possible, future demand for canola looks highly secure.

Have any questions or comments?

Key Points

- Biodiesel production is an important source of demand for oilseed.

- Anti-palm oil EU policies could increase EU demand for canola by up to 6mmt by 2030.

- Developing world is expected to drive most of the growth in this market.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: FAO, OECD, USDA, Mecardo