Aside from some weekly variation, domestic cattle prices are continuing their bullish run, with the Eastern Young Cattle Indicator trading 60 per cent higher than one year ago. Seemingly ignoring the global pandemic altogether, Australian cattle prices are being driven solely by supply and demand. And this equation is very much on the side of the seller after good seasonal conditions throughout winter in many areas, and forecasts for a similar spring. But how is the domestic price impacting on our overseas markets?

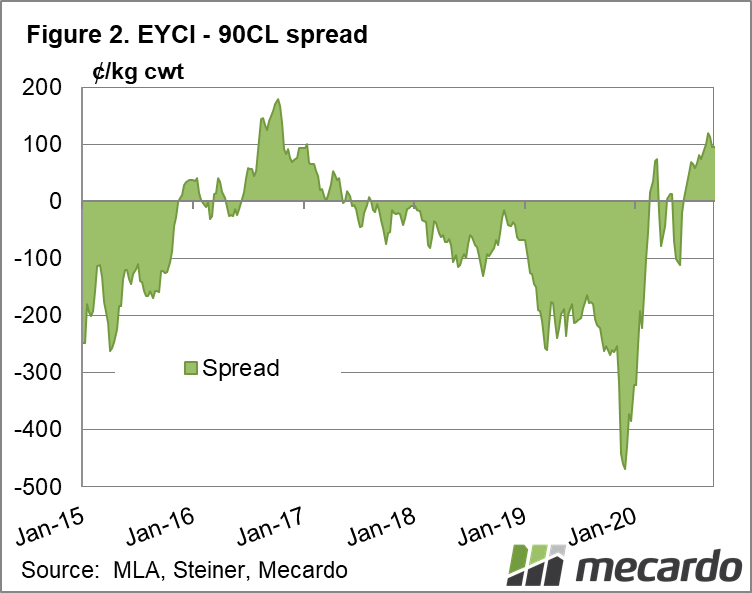

We looked at the latest export figures recently here, and they showed our high prices are being offset by lower supply – meaning our meat hungry markets will take what they can get, for now. The EYCI has been operating at a premium to the 90CL (US export price) since February (disregarding the months it wasn’t being generated because of Covid-19). Keeping in mind the 90CL data is a week delayed, latest figures have the EYCI 100¢/kg higher than the 90CL price in Australian dollars.

Traditionally, when the EYCI overtakes the export price, overseas markets start to push back. Last time the EYCI was at a premium, in 2016-17, it was also a period of restocking and record prices. Differing factors this time around are a tighter than usual supply scenario – even for a restocking phase – along with processor shutdowns in the US and Australia because of Covid-19, and African Swine Fever impacting China. These factors may be contributing to why the US is yet to push back on price.

If we look at the latest export value data available (July) we can see that total beef export volume for the month was down 33% year-on-year, and total beef export value dropped roughly the same amount. If we look at the US specifically, the volume of Australian beef sent there in July was roughly the same as last year, however the value of that beef rose by 10%.

The latest report from Steiner out of the US states that those looking for Australian product are finding “supplies very tight”. With roughly 100,000 less cattle processed per week for August in Australia, and the USDA putting out 2021 forecasts for Australian beef inventory, slaughter and export of even lower figures then this year, importers will have to start considering their options. For instance, beef from South America. In good news for us though, Argentine beef has reached its quota, and Brazilian finished cattle prices have risen 18% in US terms, and the Brazilian Real is on its way up.

What does it mean?

For now, our domestic cattle prices are bucking the trend, and with supply generally getting tighter in the coming months, may well continue to do so. US domestic production – which is back above year-ago levels with more cattle heading onto feed as well – and political standing with China will be the global indicators to watch.

Have any questions or comments?

Key Points

- EYCI maintains premium over 90CL export price

- Export markets yet to push back on price as supply dearth continues

- USDA forecast Australia beef exports for calendar year 2021 as 21 per cent lower than 2019.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: MLA, Mecardo