All lamb indicators tumbled lower this week due to a solid surge of lambs coming to market with prices for most key categories of lambs dropping a sizable 2-5% in the space of a week. In contrast, sheep prices were resilient despite evidence of a sharp jump in yardings, advancing 4%.

Prices were subdued this week, with all the east coast lamb indicators falling under the pressure of sharply increased numbers in the saleyards. Restocker lambs took the wooden spoon for falling a punishing 47¢(-6%) during the week down to 774¢/kg cwt. Heavy lamb prices also dropped 18¢(-2%), closing the week at 804¢/kg cwt. Light lambs exited the week relatively unscathed at 801¢/kg cwt

The ESTLI lost ground, shedding 25¢(-3%) to close the week at 791¢/kg cwt/ However, the NMI strengthened, clearly benefiting from solid underlying demand, advancing 27¢ (4%) to 648¢/kg cwt.

Looking at the preliminary yardings statistics for each of the categories, the sizable dips in prices can be chalked up to a significant surge in supply in comparison to demand. For example, eligible lambs contributing to the national trade lamb indicator were up 53% week on week to 19,900 head. Heavy lamb supply increased 40% to 70,252 head. Light lamb volumes surged 81%, to 13,119 head. Restocker lamb yardings increased only 15% to 11,420 head, but suffered the most savage price fall out of the group.

Interestingly, the NMI index’s offering increased 55% to 16,223 head, and prices actually advanced despite the big influx in supply. To put this in perspective though, weekly sheep supply has been at least 25% higher in the last couple months.

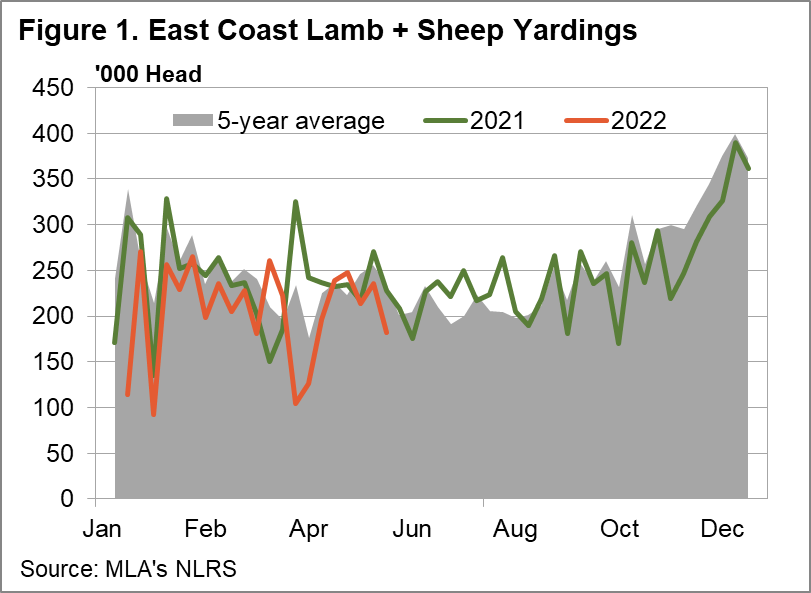

Last week’s east coast lamb slaughter increased 6% to 363,417 head, while sheep slaughter numbers lifted 4% to 90,082 head. Sheep slaughter in NSW has followed a downward trend over the last month, while VIC volumes show a vague rising pattern. Lamb slaughter numbers remain in the position we would expect them to be given the larger flock size- well above 2021 levels.

The official release of yardings data applicable to last week, ending 03/06/2022 were indicative of a fairly large bump in the road for lamb and sheep supply, with east coast lamb yardings down 21% to 143,028 head, while sheep numbers had dropped 28% to 54,669 head. The signs we are seeing of a big lift in yardings for this week however seem seasonally unusual, as a surge typically doesn’t occur till after the financial year.

This raises the question about whether this is the point where we will finally see the backlog of lambs for this year rush to market. Part of this week’s increase can be attributed to a few sales being cancelled next week due to the queens birthday holiday, but this doesn’t impact major saleyards like Wagga & Ballarat, which operate on Tuesdays and Thursdays.

The week ahead….

All eyes will be on volumes in the saleyards next week, with another repeat of this week’s elevated volumes likely to put downward pressure on prices. If you are selling sheep though, you seem to be in luck, as demand appears to be well and truly outstripping supply at the moment, with pricing again in the heady regions we saw in mid to late 2021.

Have any questions or comments?

Click on graph to expand

Click on graph to expand

Click on graph to expand

Data sources: MLA, Mecardo