Merino wool prices are trading at good levels and there are economic storm clouds on the horizon in the form of interest rates and political instability in Eastern Europe, along with logistic issues which have reduced shipping reliability markedly. The question about hedging naturally arises at such a time. This article takes a look at the 19 MPG in this light – spoiler alert; there are no easy answers.

The wool industry tends to berate itself for not having a liquid forward market, like the cotton industry for example. The farming section of the industry adopts new ideas, on average, if there is a dollar to be made. Witness the change in merino micron in recent decades, the switch out of lamb in the 1980s and back into lamb in since the 1990s. So, the question about forward markets is really, “Is there a buck to be made” or if not, are there some other significant advantages to be gained?

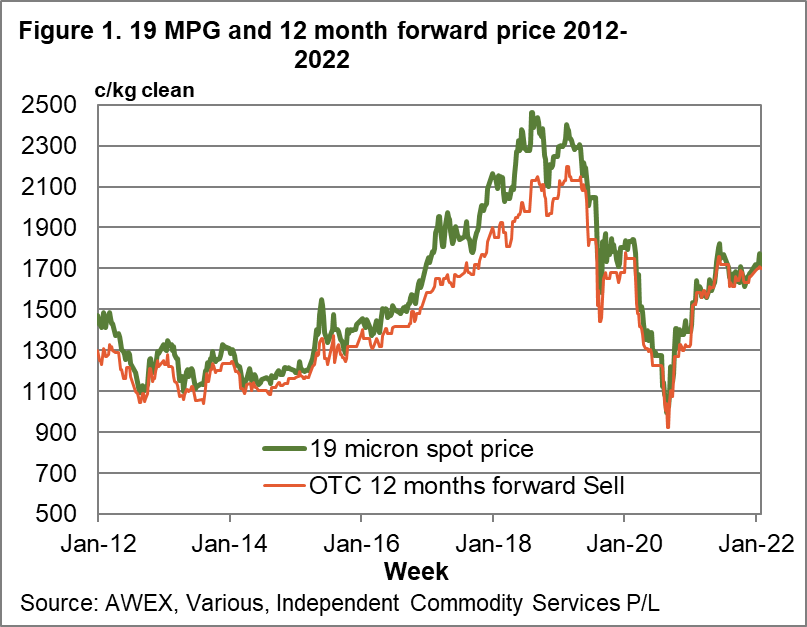

Figure 1 shows the eastern 19 MPG (19 micron has been the effective average fibre diameter of the merino clip for the past decade) from 2012 onwards, along with a 12 month forward price series. The forward price trends to follow the auction level, plus or minus a margin – generally a discount but this has tempered in recent years.

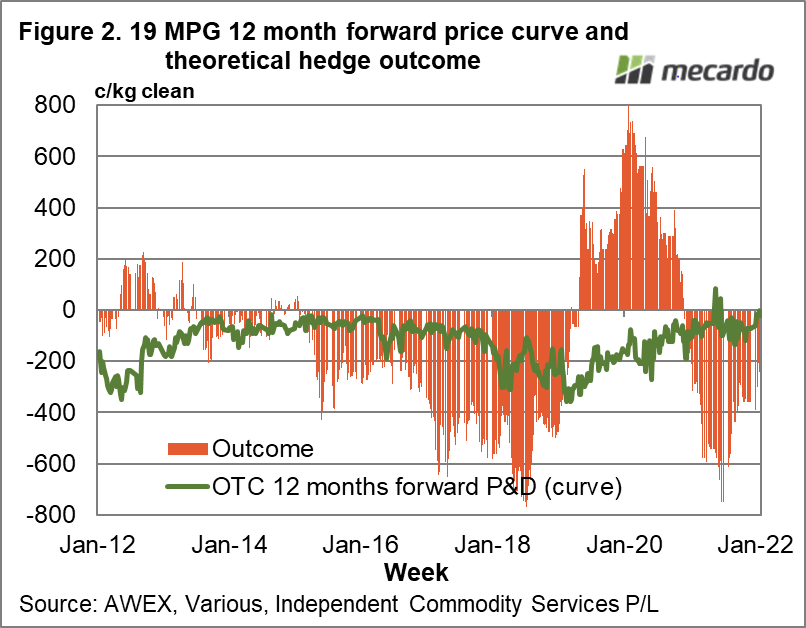

Figure 2 shows two series. The line is the discount/premium which the 12 month forward prices traded in relation to the 19 MPG between 2012 and 2022. The bars show the final outcome 12 months later (note we do not know the result for the theoretical hedging for the past year yet). From 2012 through to mid-2018 the result is skewed badly to a hedge loss, then form mid-2018 through to early 2020 the result swings around to be skewed heavily a hedge profit before swinging back to a hedge loss again in the autumn of 2020. During this decade hedges were profitable 28% of the time for the 19 micron category, looking forward 12 months.

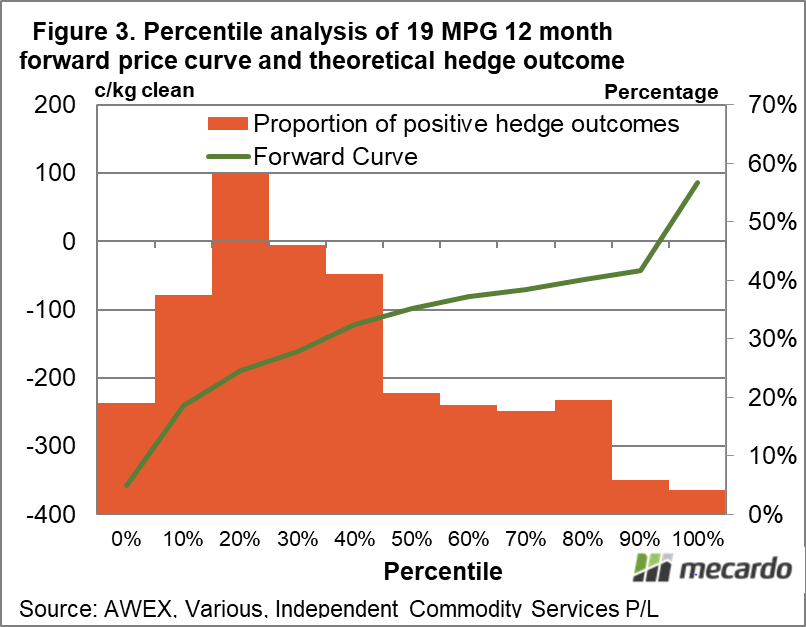

Figure 3 breaks up the hedge outcome according to the forward price premium and discount at the time of hedging. This forward price premium and discount is shown along the horizontal axis in deciles, with the average level for each decile shown in the left hand vertical axis. The bars show the proportion of hedges which would have been profitable (right hand axis). The interesting thing here is that the forward curve provides some useful information. When the curve is heavily discounted, the forward market is flagging a significant chance of lower prices in the future and, despite the discounts, the chance of the hedge being profitable is significantly higher. When the forward curve is only discounted slightly or at premiums, the probability of the hedge being profitable is quite low. The message from Figure 3 runs against human nature as it is much easier to sell forward when there are premiums then when there are heavy discounts.

What does it mean?

Pandemics aside, the forward market does a reasonable job in reflecting price risk through the forward prices premiums and discounts to the auction market. When the forward prices are heavily discounted, flagging significant risk of lower prices, the forward market has worked reasonably well as a way to hedge and offset a large part of this risk.

The downside to this is that it is harder mentally to sell at large discounts. The current market is not discounted, therefore it is flagging minimal levels of risk for the 19 and 21 micron categories.

Have any questions or comments?

Key Points

- On average hedging 19 micron wool 12 months forward has not been a winning strategy during the past decade (positive 28% of the time), unless you are gaining some benefit beyond a simple hedge profit.

- Forward prices do carry useful information about risk in the market.

- Selling forward has had a much better chance of being profitable when the forward prices were heavily discounted.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources:

AWEX, Various, ICS