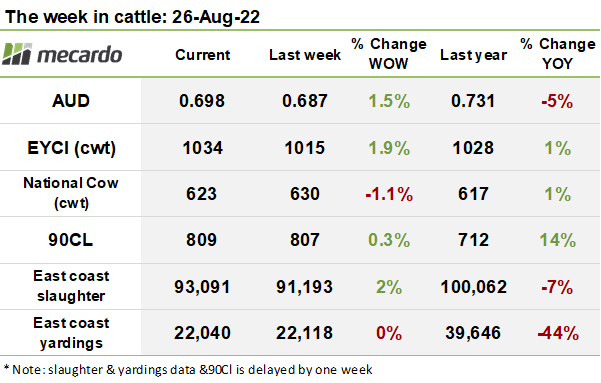

Prices advanced this week, but the exciting point of difference is that volumes in the yards have returned also, pointing towards underlying strength in demand to back it up this time. A lot of confidence seems to have returned to the markets compared to a month ago, probably fuelled by a return to La Niña watch status for the summer coming, and biosecurity hysteria subsiding.

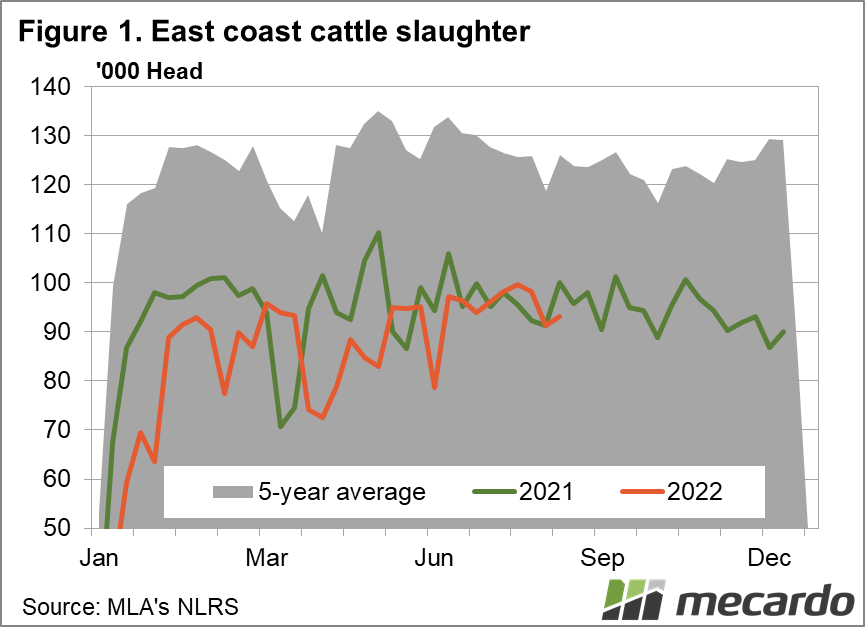

Last week’s east coast slaughter volumes lifted 3% to 93,091 head, with a 9% lift in QLD volumes more than offsetting a 15% drop VIC. We are still a hefty 7% down from where we were at this time last year however, and given the expanded herd, it’s likely there is a large chunk of supply being held back.

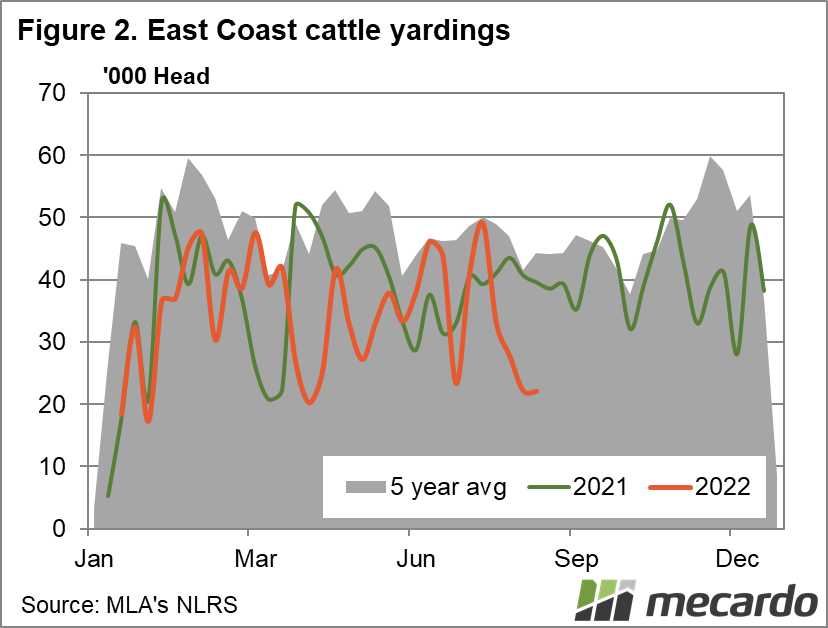

The most exciting indication of a return to a more sustainably robust market for young cattle was a 70% lift in EYCI eligible yarding volumes, to 12,289 head- a level of supply we haven’t seen since late last month, when prices were spiralling downwards. Restocker volumes were also up 83% to 2,509 head which is suggestive of a return to confident purchasing by producers, again, probably due to positive signals from the BOM that we may see the influence of La Niña weather systems hanging around into next season. Given the early indicators, it’s likely that when yardings numbers for this week are released, they will tip well over the 35,000 head mark- a good 60% increase on last weeks number, and fairly close to where the supply situation was at this time of the year in 2021.

The Eastern states Young Cattle Indicator (EYCI) lifted 19¢(2%) on the prior week, although still well down form the highs seen earlier this year, the index is still travelling at 1% above where it was sitting last year.

The Western Young Cattle Indicator (WYCI) accelerated forward, pushing up 101¢(+13%) to end the week at 955¢/kg cwt.

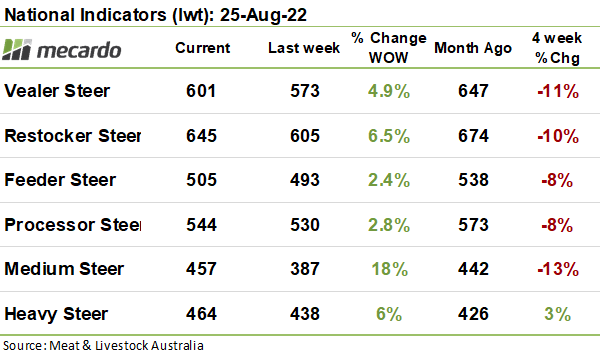

The national indicators saw another positive week, with green ink right across the board. The standout was the medium steer price, which rocketed up 18% against the drag of higher yardings, though one does need to consider that the transacted volumes in this index are quite thin, at only 158 head this week. Of more interest was the restocker index, which increased 39¢(+7%) on the week, again against the tide of an 83% increase in supply volume.

Aussie 90CL prices in the US improved 2¢(<1%) to bounce back up to 809¢/kg swt, with the increase stemming from the depreciation in the Aussie dollar recently. This gain will be eroded next week by the gains the AUD made against the greenback this week. Steiner reports that the imported beef market in the US is slowly grinding lower, as exporters fold and take lower bids from buyers. The outlook on US cattle slaughter over the next few months is still pointing towards elevated production, as forecasts of continued dryness pressure US producers to lighten stocking rates.

The week ahead….

Prices holding, and even pushing higher despite signs of a strong increase in yardings this week which are probably close to 2021 levels again are extremely encouraging. The healthy demand we have seen this week could just be pent up buying interest saved over from the last few slow weeks which may cool.

However, more positivity next week could confirm that we are out of the localised downward spiral caused by depressed demand, and our attention needs to turn more firmly towards assessing the international export situation and processor capacity closely, namely the inflation and recession impact on consumer beef demand.

Have any questions or comments?

Click on graph to expand

Click on graph to expand

Click on graph to expand

Click on graph to expand

Data sources: MLA, Mecardo