As the rain in the east keeps coming and soil moisture profiles keep improving, our optimism for the next crop points to continued appetite for fertiliser. However, we’re not alone in that desire. When it comes to fertiliser consumption, Australia is just a mere drop in the global pool. There are other consumer countries, much bigger consumer countries, that are hungry for N.

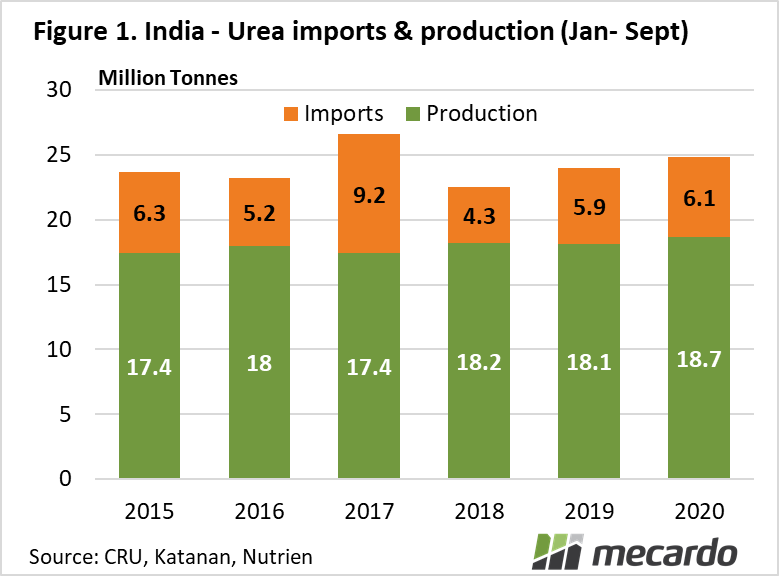

China may have been all the talk of agriculture markets in 2020, but in fertiliser markets, the spotlight has been shared with India. This year it’s been strong import demand from India and tight export supplies in China that have supported the global urea market. Government Minimum Support Price schemes and good monsoonal rains saw record acreage sown in India’s “Kharif” crop season (April to September).

Expectations of record grain and rice production have in turn fuelled significant demand for urea, with India opening back-to-back tenders and soaring retail fertiliser sales. Their most recent urea tender was reported at 2.2 million tonnes. This single tender was larger than Australia’s total urea imports from January to August this year, and at 2.1 million tonnes, this was a record amount.

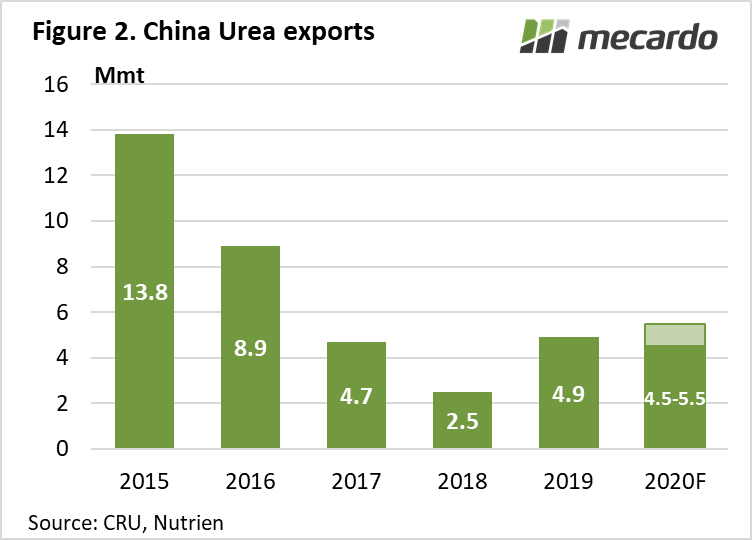

So on the demand side, the fertiliser market has been reasonably resilient in 2020 thanks to bumper crops and strong grower cash margins for key crops. The supply side, however, has been tightening. China is one of the top urea exporters, but exports have declined in recent years as many inefficient plants have closed and producers have become quicker to respond to market signals. Back in 2015 China exported a total 13.8 mmt of urea, but poor margins and low operating rates led to year-on-year declines in production and exports to a mere 2.8mmt in 2018 (Figure 2).

Strong demand from India, improved Chinese domestic demand and favourable production economics have stimulated higher production since, although the expected 4.5-5.5mmt of available exports from China this year has kept the global balance of urea tight.

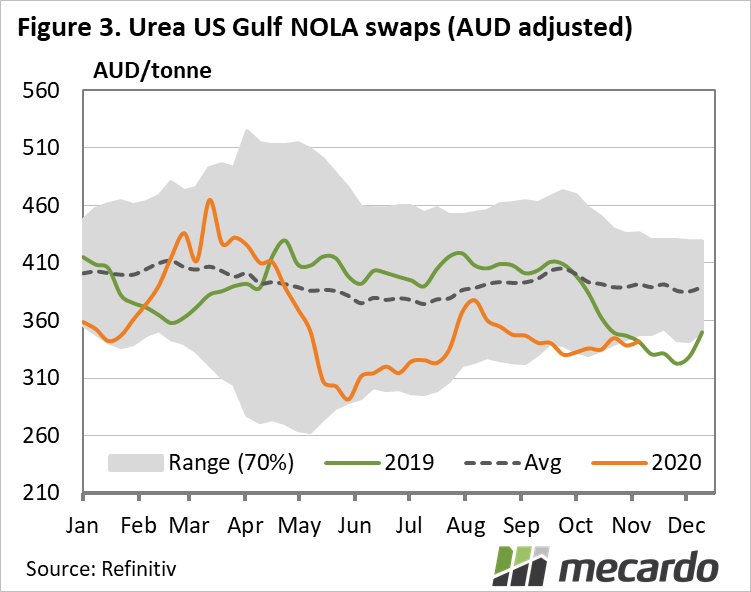

Low global natural gas prices, particularly in Europe, and lower coal prices in China have placed downward pressure on global urea prices in 2020. However, as we have moved closer to the end of the year these trends began reversing. European natural gas prices have increased significantly from lows earlier in the year and the combination of an increase in the value of the Chinese Yuan and higher coal prices have supported production costs in China, which have also increased urea prices.

What does it mean?

As with most markets, the global fertiliser market is seasonal. In general, the Northern Hemisphere’s spring season drives the market in the first half, along with the seasonal peak in prices, while the Southern Hemisphere is important in the second half. Global crop input prices have been at affordable levels, but a key risk for Australian growers lies in any fall in the AUD which would increase import costs.

The medium-term outlook is for global demand of urea to improve, with limited new capacity. Thus, the global urea supply and demand equation is expected to remain tight, particularly after 2021.

Have any questions or comments?

Key Points

- Strong import demand from India supporting global urea market.

- China urea exports forecast based on strong demand and production economics.

- Tightening global Nitrogen supply and demand.

Click on figure to expand

Click on figure to expand

*Note: Urea US gulf prices have been converted to Australian dollar terms and are indicative only of global prices. They do not take basis into account and so do not reflect local urea pricing.

Data sources: Nutrien, Mecardo, Refinitive, CRU, Katanan