The USA is one of the world’s largest beef producers and consumers, and hence have a large bearing on world beef and cattle prices. Australia’s beef production is minor by comparison to the US, but we are still heavily impacted by what is going on in the US.

With all the talk around tight world beef supplies, improving demand and record cattle prices here in Australia, you would think that we would be seeing a similar thing in the US. Figure 1 shows that while cattle prices are good in the US, they are not near records by any means.

Figure 1 shows the US Live and Feeder Cattle Futures traded on the Chicago Mercantile Exchange (CME). After diving at the beginning of the Covid pandemic on the back of processor bottlenecks, US cattle futures have gradually improvded. While being at the top of the range of the past five years, US cattle values are no where near the records seen during the herd rebuild of 2014 and 2015.

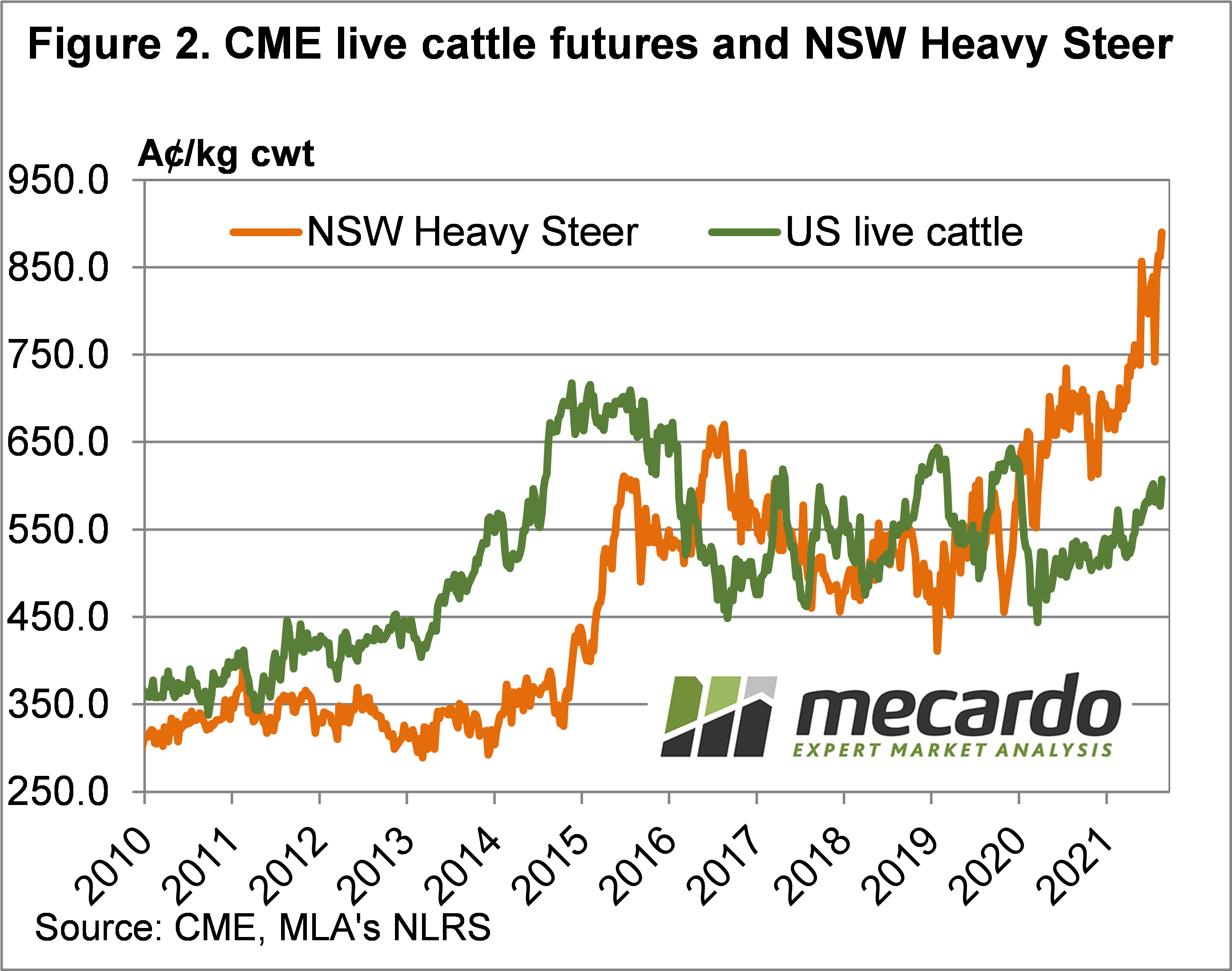

After being the poor cousin of finished cattle prices up until 2016, Heavy Steers in Australia have bridged the gap and streaked ahead. Figure 2 shows the huge premium heavy steers in NSW are trading at compared to US Live Cattle.

It seems counter intuitive that Australian heavy cattle, coming both of grass and out of feedlots are able to trade at such a strong premium to US prices. The US is a major competitor in exports markets for higher value beef, and a major market for Australian manufacturing beef. This is why our prices tend to be impacted by US prices.

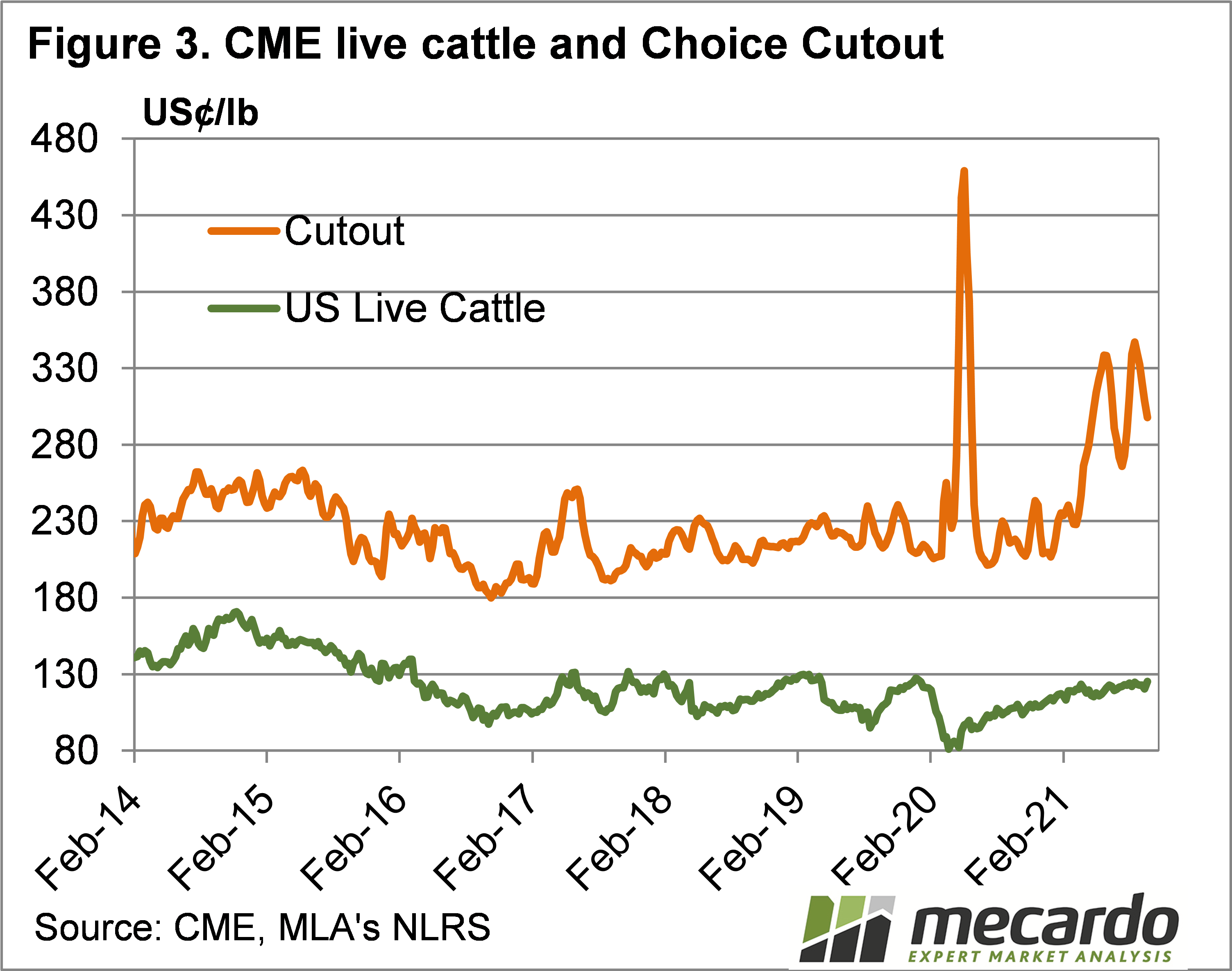

The premium we are seeing for Australian cattle at the moment is largely due to domestic processing issues in the US. Figure 3 shows the US Choice Cutout price in the US, along with CME Live Cattle Futures.

The Choice Cutout is the price of all the cuts of beef added together and boxed. US beef cutout prices are at very strong levels, but it’s not being passed on to producers due to limitation on beef processing in the US.

What does it mean?

Basically US processors are reaping the rewards of tight global beef supplies and strong demand, but capacity limitations are not seeing this passed onto cattle suppliers.

In Australia it is cattle supply which is tight, and there is excess processing capacity, and as such cattle suppliers are the ones benefiting from the beef market fundamentals.

Processing bottlenecks in the US are benefiting Australian cattle producers, but it doesn’t seems a huge backlog of cattle are building up in the US. If and when processing capacity increases it might puts some downward pressure on global markets, but it still doesn’t look like our markets are heading back to 2018-19 levels in the short or medium term.

Have any questions or comments?

Key Points

- Cattle prices in the US have recovered from the Covid collapse, and are back close to 5 year highs.

- Compared to Australian cattle prices, US cattle are very cheap.

- Processing limitations in the US are not seeing strong beef prices passed on to cattle suppliers.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: ICS, Mecardo