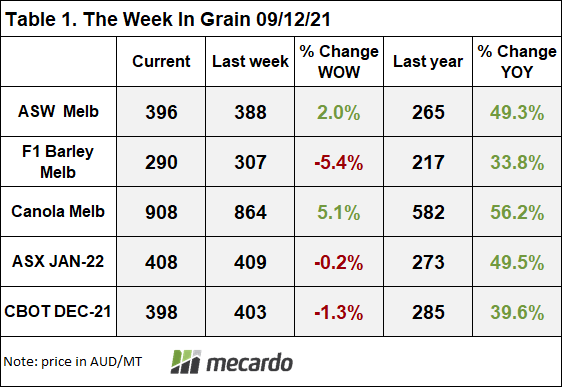

Last night the USDA released their December WASDE (World Agricultural S&D Estimates) report. In short, there was little for the wheat bulls to get excited about with increasing pro-duction and ending stocks dragging down prices. The market had been largely expecting the increase in stocks, with the USDA lifting Aussie production to match ABARES estimate and a little extra wheat in Russia. As a result, the move lower has been evident over the past couple of trading sessions.

Global stocks to use was revised up slightly to 12.6% from the previous estimate of 12.1%. It remains very tight. However, the fact that the increases were in major exporter countries, means that the reliance on US stock is slightly diminished, resulting in higher ending stock.

Corn and beans found muted support largely around supportive energy prices. Corn enjoys strong demand especially from the ethanol sector. Global ending stocks of soybeans was also revised lower based on increased consumption.

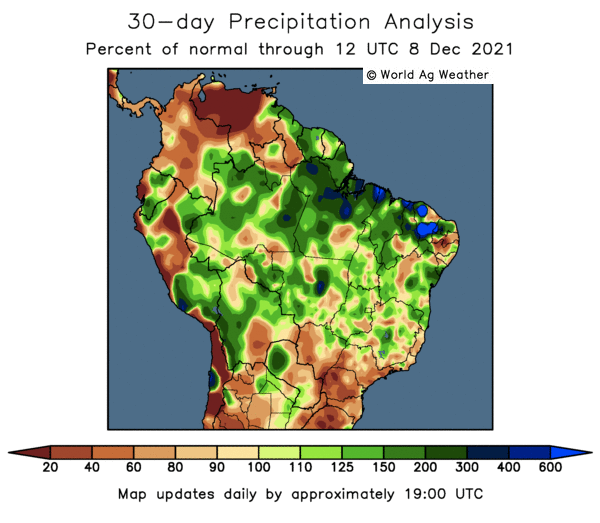

Looking forward, the market will be highly focused on South American production. Brazil is enjoying a good growing season to date, however with La Niná embedded in the Pacific, no one is taking anything for granted. Some areas of southern Brazil are showing rain deficits, including the key producing states of Parána and Rio Grand do Sul. These two areas contribute 17% and 20% respectively of the countries corn crop and combined 32% of soybeans. We are heading into the key flowering and pollination period and stresses at this time can have a significant impact on final yield.

The elephant in the room for new crop production will be the impact of fertiliser cost and relative scarcity. Some European analysts are suggesting that winter wheat is borderline producing negative margins and heavily dependent of on-going price support. With this crop already planted, and a steep inverse in European and Black Sea wheat markets, the next six months could be tough going. Questions will also continue to swirl around spring crop rotations (corn, beans, spring barley, canola) if prices for nitrogen in particular don’t ease by the time the Northern Hemisphere farmer intends to plant.

The week ahead….

While we have seen a slight improvement in global wheat inventories, the wheat market will likely remain at supported at or near these levels in the short term. However, in the absence of fresh bullish news, the market will eventually tip over.

Have any questions or comments?

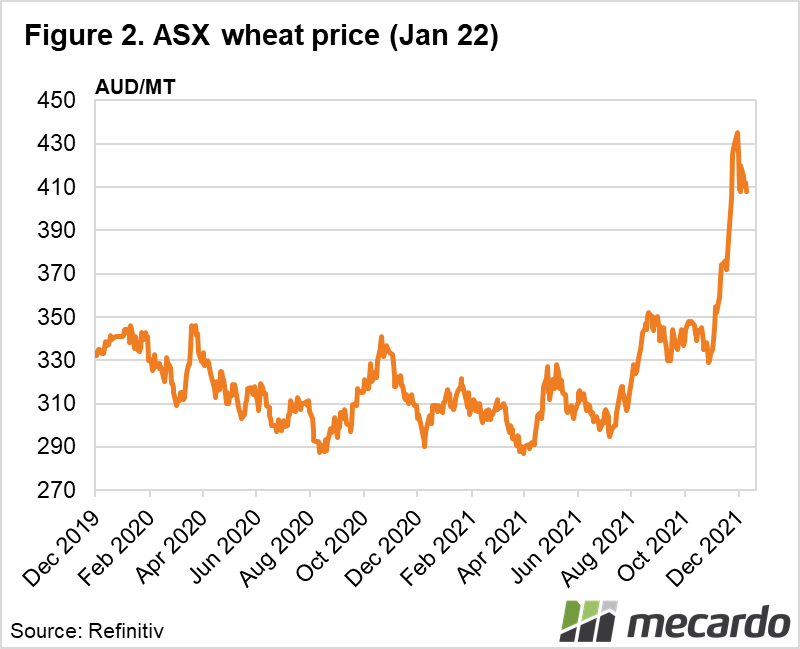

Click on graph to expand

Click on graph to expand

Click on graph to expand

Data sources: USDA, Reuters, ADHB