The wheat market is being pulled between two opposing trains of thought. One thought is that wheat should get dragged higher by deteriorating corn production in Europe and the US. The other thought points to the large Russian crop and a tenuous, yet so far workable, export corridor in the Black Sea.

The market has found some support in the past week as solid US export demand has helped to arrest the slide. The workable grain corridor has also given the macro economic factors some breathing room, resulting in a falling USD and a more ‘risk on’ attitude across broad commodity and investment sectors. How long this lasts with China beating war drums is something to watch.

The flow of grains out of Ukraine has been a major development across markets and one factor that will likely set the direction of prices in the coming months. The reality is that the ships that have sailed have been those stranded at port since the start of the war. The litmus test will be the arrival of new bulk carriers and the ability to load new crop cargo’s. At a FOB level, Black Sea grains are the cheapest in the world and should be commanding the majority of demand. At a CIF level (cost including freight), the picture is not so compelling, with insurance and chartering premiums making the outgoing leg a costly exercise.

As it stands today, trade flows are out of kilter with Europe exporting at a frenetic pace and increasing demand for US origins starting to emerge. This has the potential to leave world grain markets exposed to a situation where the majority of exportable surplus is sitting in a war zone. If the grain corridor were to slam shut again, it would be explosive for grain markets. The flip side (why is there always a flip side?) is that the flow of Black Sea grain remains steady and actually increases, eating into traditional Aussie dominated time slots.

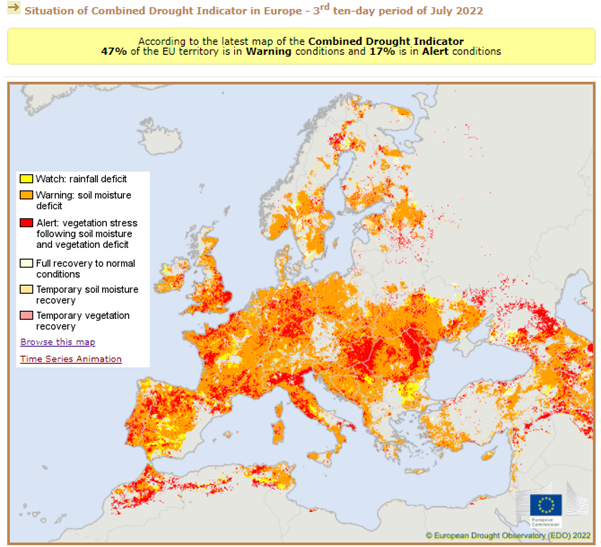

Tonight, our time, the USDA will release their August report. This has the potential to be a real market mover. Firstly, there is a widely held belief that the heat in the US corn belt has done more damage than expected and that yields are unlikely to meet the trend line 177bu/ac target. Secondly, the drought in Europe is believed to have cut corn production by 10mmt. This places more emphasis on Ukrainian exports.

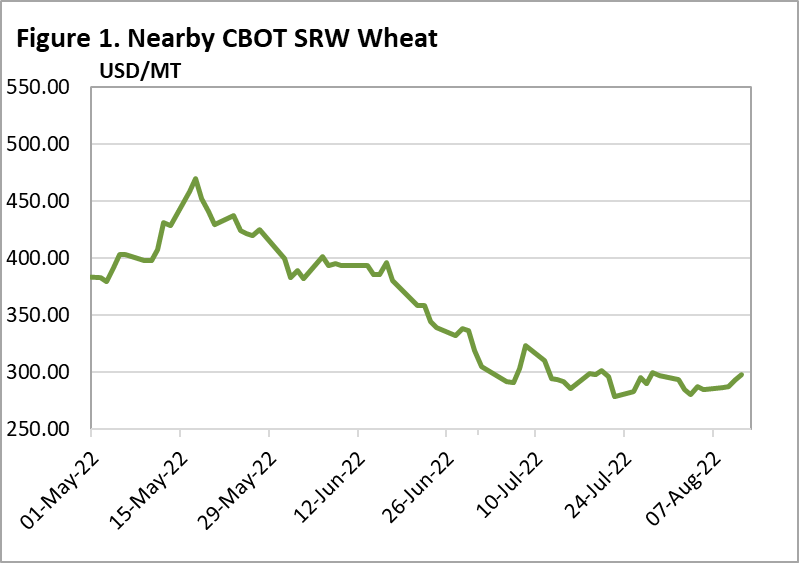

Changes to wheat production are not likely to be as significant as a good US spring wheat crop and a building Russian crop will likely cancel out any cuts to production in other origins. Looking at the wheat market chart, the price has been trading in a tightly confined range – a pattern known as coiling. This is often a precursor to a much larger move, but in which direction? A corn production estimate well below trader estimates could be the catalyst to see wheat jump higher. However, a ‘friendly’ corn production number, would disappoint the market bulls and see the market move another leg lower.

The week ahead….

Longer term, it feels like the wheat market will grind higher on the back of tightening stocks and demand rationing. Shorter term, the market will likely remain choppy, trading Black Sea news and weather/production related issues.

Have any questions or comments?

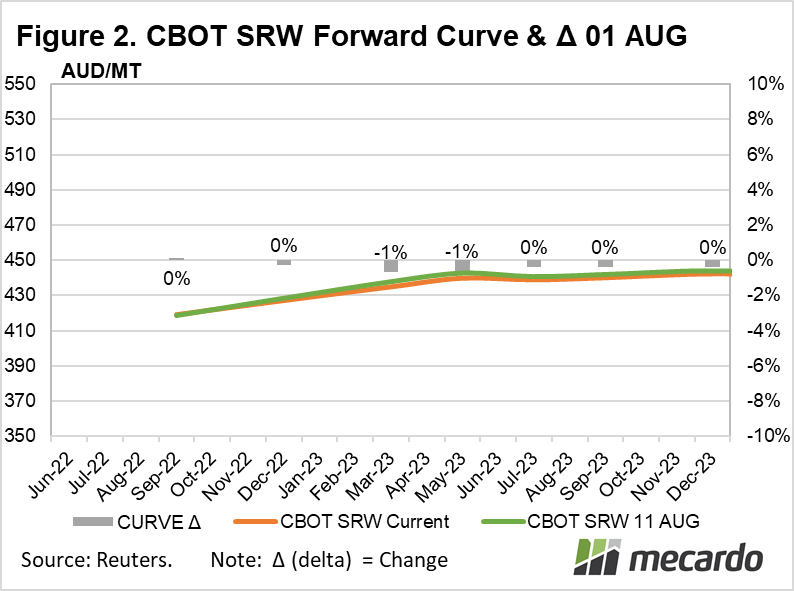

Click on graph to expand

Click on graph to expand

Data sources:Reuters, Strategie Grains, Agricensus, EU commission, Mecardo