The wheat market has been looking decidedly sick over the past few trading sessions. The Dec ’22 wheat contract has lost 77ȼ/bu for the week. Wheat isn’t the only commodity under pressure, with Dec ’22 corn down 12ȼ/bu and the MATIF rapeseed Nov ’22 contract down a sizeable €54/t.

So where has the shift in momentum come from? It is hard to put a finger on any one event, rather it is the combination of a number of factors. The evolution of the Black Sea grain corridor is perhaps the biggest turning point. As of last night, another 4 vessels sailed out of the Black Sea bringing the total tally to 25 vessels since the corridor opened. To start with, most of the vessels were relatively small, but with increasing confidence, we are now seeing larger bulk carriers being booked and making the journey. This week, bulk carriers will load 70kmt wheat from Ukraine which will mark a milestone event for the under siege country.

Production of wheat is also seen as rising in major exporters. SovEcon raised Russian production to a record 94.7mmt this week, on the back of the USDA increasing Australian production to 33mmt and Canadian wheat (non-durum) to 28mmt (up 49% from 21/22). The overall increase is likely minor when considering reduced production in Europe and India.

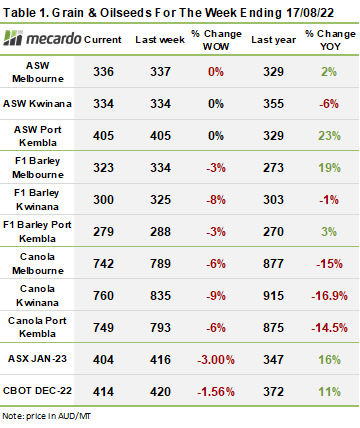

Canola prices here and abroad have been under pressure as well. The oilseed complex as a whole initially hit record highs on the war in Ukraine but also the export ban of palm oil from Indonesia. With both of these issues now seemingly in the rearview mirror, oilseeds have been taking their lead from crude oil. As a macro economic indicator, crude has also been under the pump on faltering economic conditions in Europe, the US and now concerns that the Chinese economy is teetering.

The ag commodity market appears to be pricing in a ceasefire in Ukraine on whispers of peace talks. Zelensky has said no ceasefire until there is full Russian withdrawal from all occupied territories. It remains a very difficult situation to price, especially when you consider that a third of the world’s exportable surplus is still sitting in an active war zone.

The week ahead….

Longer term, corn production in the US and South America, a three peat La Niña and the ability of the Ukrainian farmer to sow their winter wheat crop will have a say in wheat price direction.

Have any questions or comments?

Click on graph to expand

Click on graph to expand

Data sources: Reuters, Oilworld, SovEcon