At the absolute last minute, Russia rolled over and rubber-stamped the Black Sea grain corridor for another 60 days. This is despite getting no concessions from the UN in terms of relaxing any of the sanctions that Russia was unhappy about. The delaying tactics and rhetoric leading up to the deadline meant that the market had priced in a risk premium, no doubt helped by some speculative rebalancing of poorly placed short positions.

Since the grain corridor terms were agreed to, we have seen wheat lose approximately 60c/bu or roughly AU$33/t over the past three trading sessions. Corn has lost 40c/bu and soybeans 70c/bu. It has been a significant fall in anyone’s language.

Wheat prices are now playing ‘catch up’. Russian FOB values are trading around US$262 FOB (despite them setting a floor of $275) and European wheat is now seen trading at US$258 FOB as they attempt to win back some market share.

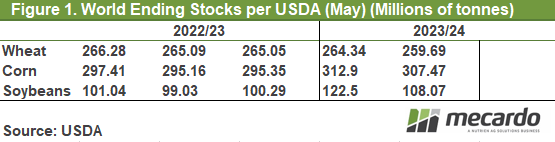

Wheat is now trading at two-year lows and looks weak. But now time for a little bit of perspective. While all this drama has been going on, the USDA released its US and global stocks report. Corn and bean stocks look a little more comfortable courtesy of slow Chinese demand and a monster Brazilian crop. Wheat gets tighter and major exporter stocks are suddenly down around 13% stocks to use.

This is despite the projection of some bumper crops. Europe is sitting on a big crop (147mmt?), the Russian crop is at 85mmt and potentially getting bigger, Argentina has bounced back from the brink with an estimated 19mmt crop, and Canada has hopes of a record crop based on increased wheat acres. This hasn’t been enough to offset a smaller US crop and an Australian crop forecast of 28mmt (down from 39mmt last year).

The interesting thing about the Aussie forecast is that this number is based on a 2.2t/ha average. The long-term rainfall outlook does not support a 2.2t/ha average given our average wheat yield is 1.82t/ha. Assuming average yields, Australian production would be in the order of 24mmt. Unless we see widespread demand destruction, the tightness of global supplies should eventually lend support to prices.

The week ahead….

In the short term, the continuation of the Black Sea grain initiative removes a lot of the need for speculative traders to quit their short (sold) futures positions. They may even resume building their shorts. With the Northern Hemisphere harvest in about 4-6 weeks, I would expect prices to continue to show weakness.

Have any questions or comments?

Click on graph to expand

Data sources: USDA, Reuters, CSIRO, Next Level Grain Marketing, Mecardo