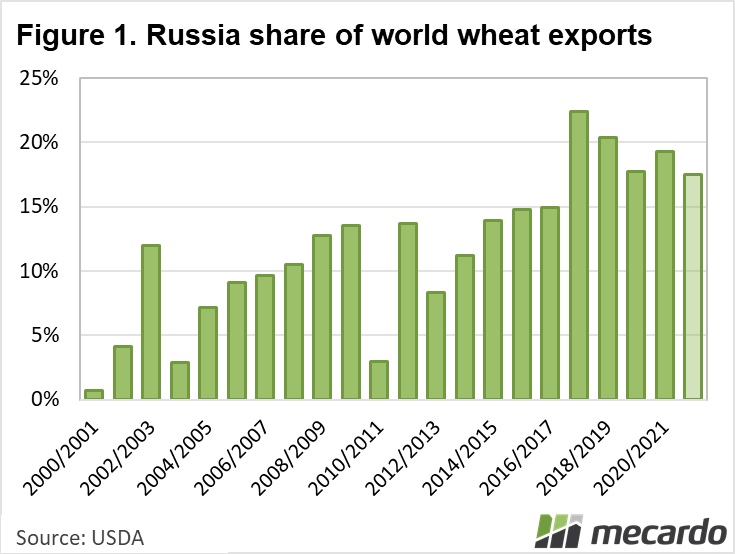

In 20 short years, Russia has grown from a food insecure, net importer to the world’s largest, and arguably, most important wheat producing nation. The opening up of the Soviet Union presented to the world an opportunity to invest in a relatively undeveloped agricultural sector and start afresh.

In the past eight years, Russian wheat production faced a golden era where production records were being broken every year. Foreign investment, naturally fertile soils, improving technology and infrastructure has seen Russian agriculture expand at an unprecedented rate. A warming climate was also seen to be helping wheat production, especially the dominant winter wheat class (70% of total wheat produced), as winters were seen as becoming milder.

In the past couple of years, by a quirk of fate, wheat production in the domestic zones around the centre and northern Russia has been poor. This has led to increasing staple food costs as wheat (also sugar and edible oils) are freighted from the southern districts to the population dense north. As the cost of living started to rise (food inflation) the Russian Gov’t stepped in. The Russian Export Tax was implemented in 2020 as a means of reducing the pace of exports to maintain a critical mass of domestic food supply.

An initial fixed export tax was scrapped in favour of a more complicated floating tax, and to add to the complexity, it was to be adjusted on a monthly basis. So other than immediate delivery, exporters face great uncertainty over how much duty they will be forced to pay. The tax has turned global market dynamics on its head.

Still, Russia remains a wheat powerhouse. Exporting is more risky, but courtesy of production issues in North America, quality issues in Europe and significant disruption to export capacity in the Gulf of Mexico, market analyst ProZerno report that Russian grain exports hit an all-time record of 5.7mmt (including 5.2mmt wheat) in August. Most of this business is done at the private sector level where long-term relationships are viewed with more importance than that seen at the international tender level.

Whether this export pace can be maintained is questionable. The floating export tax and Russian FOB values are increasing in line with global prices. The increase to the tax simply puts more pressure on the very tight stocks held by the remaining major exporters.

Another factor at play is the new found freedoms being enjoyed and employed by the Russian farmer. They are exercising their market rights and simply holding onto grain when the prices are considered too low and also using their stored grain as a market hedge against a dry winter seeding campaign. Global stocks are tight enough without any concerns around the fate of next seasons wheat.

What does it mean?

The Russian Gov’t have said that the Export Tax is here to stay. While it makes global trading far more complicated, it has also priced Russian origin wheat out of competitive international tenders. Exorbitant ocean freight rates and production woes in the US and Canada, puts Australian wheat in the box seat.

Have any questions or comments?

Key Points

- Russian transition from food insecure/net importer to global wheat exporting powerhouse over past 20 years.

- Russia may account for 1/5th of global wheat trade this season.

- Russian government export tax set to stay for the foreseeable future.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: USDA, Bloomberg, RusGrain Union, ProZerno