If you’ve spent much time looking at livestock commodity markets in the past five or so years, China is a topic you’d be familiar with. It’s impact on Australia’s red meat export has been on the rise, culminating in 2019 when it took about 25% of our lamb and beef that went offshore, and 45% of our sheepmeat. Lower livestock slaughter and in turn production, caused by green grass galore in the south east, has meant a significant drop in exports due to the sheer lack of product. But those Chinese percentages have also fallen, especially since the latest trade issues between the two countries started in May.

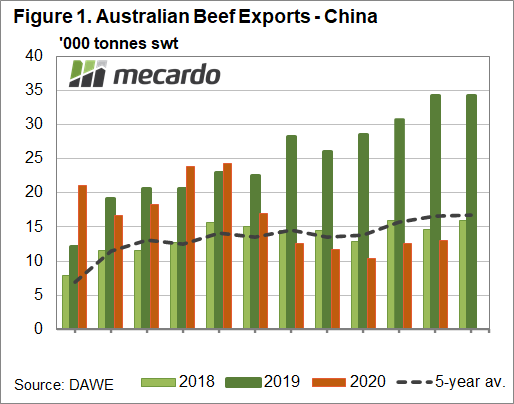

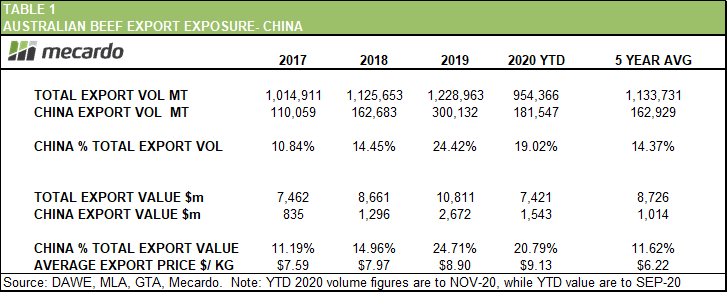

The number of Australian abattoirs which now aren’t able to trade with China rose to eight this week. For these exporters who have had to find alternative markets for product, the “bite” will be reflected in export values. China, while not always our biggest beef export market, does currently make up 19% of the year to date volume – down from 24% last year. Beef volumes sent to China in November were at their highest levels since June, but were still more than 60% lower than the same month last year, and 21% below November’s five-year-average. Certainly, some of the decreased Chinese activity in our beef market can be put down to Australia’s dramatic production decline and dipping volumes since trade tensions began to rise – the first round of abattoirs were suspended for the year in May. Covid-19 has also no doubt played a role, with China not the only country to have had monthly export volumes from Australia dip below the five-year average over the past six months. It is however, the only country that has lost market share.

And just as we point to market resilience due to the variety of export markets we have, China so too has alternative options. Last month we took a closer look at the volume of South American beef heading to China, with their growing herd numbers and low-cost point creating strong competition for Australia (view article here). But as well as countries such as Brazil and Argentina competing on the beef front, the US has started to increase their market share in the premium beef sector in China as well. While beef volumes from the US to China are still relatively small-fry compared to Australia, they have more than tripled so far this year, and Meat & Livestock Australia report there is still more than last year’s total volume still to be sent in outstanding orders. As we know all too well, dealings with China can be fickle, but one would think there’s a strong possibility of improved US-China relations when the new US president steps in.

What does it mean?

Asked at the dinner table this week how much of an impact the China situation would have on the overall beef market, I felt confident Australia’s supply and demand scenario would mean it would bring limited downward pressure on domestic prices in the short to medium term. Now looking closely at export volumes, it is clearer that the supply dearth can only help producers for so long, and better China relations, or new markets, are going to be crucial.

Have any questions or comments?

Key Points

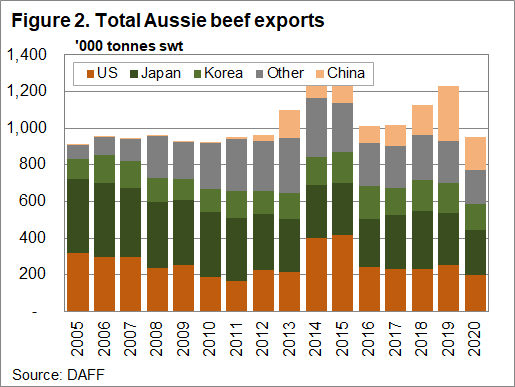

- Australian beef exports for the year to date are 15% lower than 2019, with volumes to China down 32%.

- Japan remains the largest beef export market, down just 7% year-on-year, followed by the US, which has taken 22% less Australian beef this year.

- Monthly Australian beef exports to China have fallen well below the five-year-average since trade tensions increased in June.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: MLA, DAWE, GTA, ABARES, Mecardo.