Wool (merino and crossbred) is produced across a wide array of geographic regions in Australia. This article takes a brief look at the (auction) sale value of wool produced out of the regions.

Wool prices are built primarily on breed, category (fleece, pieces etc..), objective measurements (such as fibre diameter), subjective assessments (such as stain, modulation and so on) and in recent times accreditation to quality schemes. Of the objective measurements fibre diameter has been the dominant characteristic driving price since the advent of the modern greasy wool market in the early 1980s, albeit with fluctuations in its effect on price.

The paragraph above is a preamble to looking at Figure 1, as the varying bale values will be a function of the qualities of wool produced in each region. Further to that profitability is a function of production per hectare rather than price per kg as the Holmes Sackett benchmarking showed year in, year out.

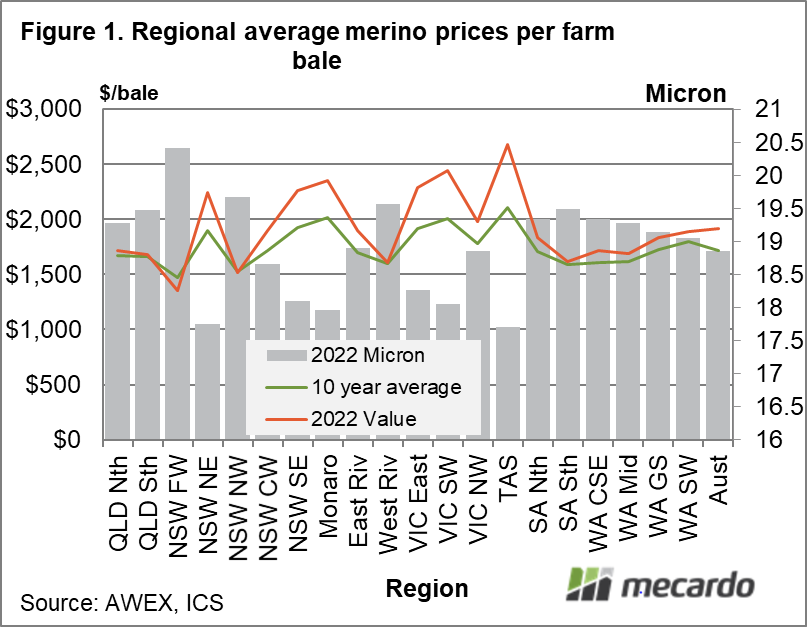

Figure 1 shows the average auction sale value for merino (all wool sold at auction except for broker rehandle wool) wool sold in the current season to date by region. The regions run from Queensland on the left through NSW, Victoria, Tasmania, South Australia to Western Australia on the right hand side of the schematic. In addition the average bale value for the past decade is shown and the average merino fibre diameter for the current season (2021-22). As would be expected given the extreme price differences between micron categories during this season, micron accounts for 93% of the price differences between regions.

Tasmania has the highest average merino farm bale value for the current season of $2,677 gross, averaging 17.7 micron. The overall Australian average merino fibre diameter has been 18.85 microns for the season to date with a farm bale value of $1,912. The region with the broadest merino clip this season has been the far west of NSW averaging 20.4 microns.

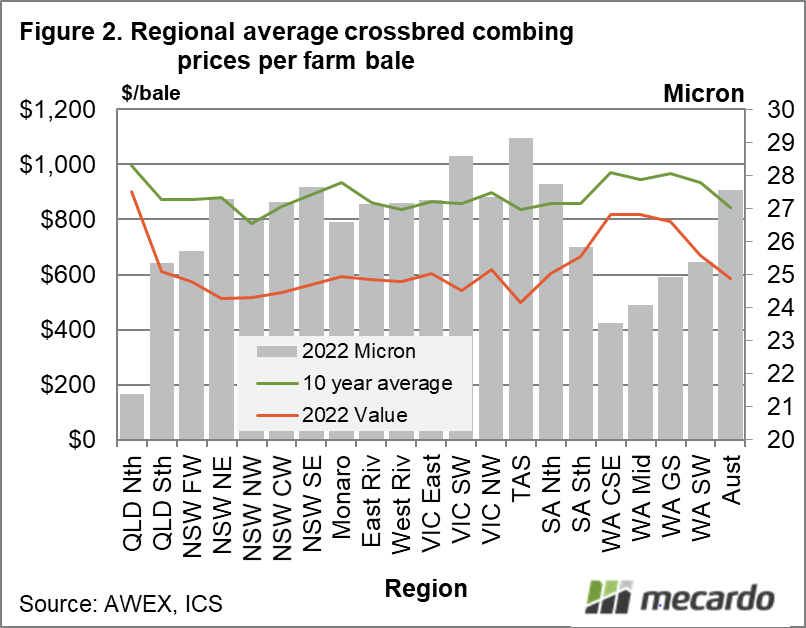

To complete the wool picture Figure 2 repeats the exercise for combing length crossbred wool. Needless to say the current season bale value is well below the decade average. Regions with finer crossbred combing (quite likely to be comeback wool which is not officially recognised by the AWEX ID system) have averaged higher prices, with this supporting a strong correlation between average bale value and fibre diameter. In contrast to its merino clip, Tasmania comes in with the broadest crossbred combing clip at 29.1 microns.

What does it mean?

Regions with finer merino clips have bale values well above their decade averages, which makes sense given the extreme fine wool premiums operating this season. Regions with an average merino micron in the 18.5 to 19.5 micron range have been selling wool close to their decade averages. Fibre diameter is usually the prime driver of price differences between regions as it has been this season.

Have any questions or comments?

Key Points

- In the season ladder for merino bale value Tasmania leads the way followed by South West Victoria and the Monaro.

- The Tasmanian performance is underpinned by having the finest merino clip, in contrast to having the broadest crossbred combing clip.

- Fibre diameter normally drives the differences between regional wool values, and it is doing so very strongly this season.

Click on figure to expand

Click on figure to expand

Data sources:

AWEX, Holmes Sackett, ICS