The price point everyone loves to follow has kept its upwards glide this week, reaching a record high 910¢/kg. The Eastern Young Cattle Indicator surpassed the 900¢/kg mark for the first time at the end of last week, and is close to 200¢/kg higher than the same time last year. As always, supply and demand are playing the main parts in the EYCI story, as yarding numbers remain limited and pasture prospects continue to look positive for the winter.

Generally, the percentage spread between the EYCI and other key indicators have been following patterns seen in the previous cattle market price swell in 2016/17, when conditions were similar. However, the differentials are also now hitting record highs, which traders need to be aware of.

First let’s look at the EYCI. In Tuesday’s record indicator, there were 14,326 head eligible – one of the larger offerings for April so far – with the Roma store sale making up a very clear majority of these at 27 per cent. In fact, with the exception of only a handful of head at Toowoomba, the listing of numbers per location from highest to lowest are clearly in state groups as well, with Queensland at the top and Victoria at the bottom. Processors remain priced out, loading less than 10% of EYCI cattle, with the remainder split fairly evenly between restockers and feeders.

In March last year, the EYCI started its current record run when it reached 737.50¢/kg. There were just 12,200 head eligible for that indicator, and it was 320¢/kg higher year-on-year. This means the EYCI has risen more than 500¢/kg in the past two years. There have been many comparisons to the last low-supply, high-demand period of 2016/17, but now the prolonged gains are reaching unchartered waters. When the EYCI broke its then record in August 2016 of 725.25¢/kg, the gains only lasted a matter of weeks, and significant falls occurred within 12 months.

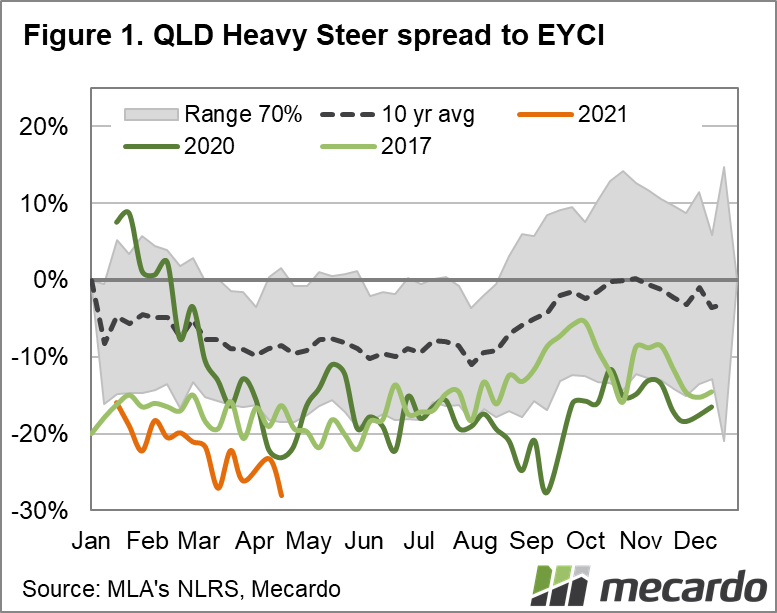

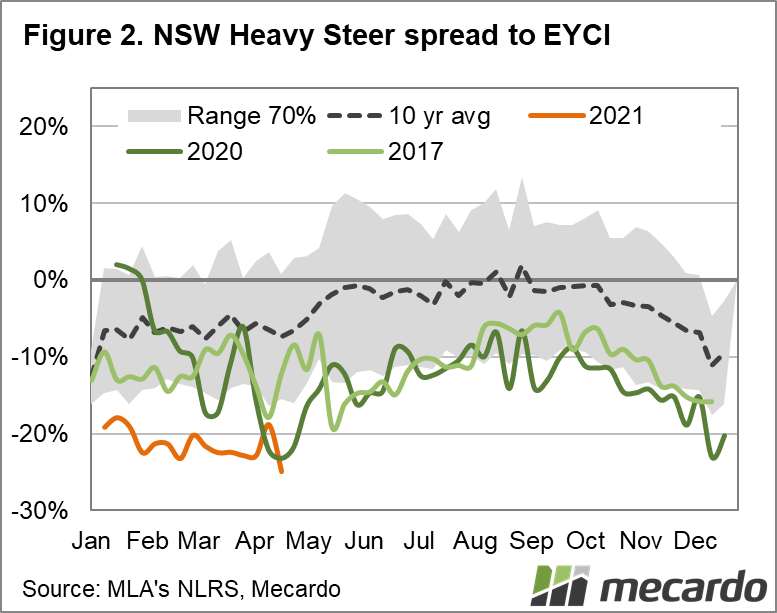

If we look to Figure 1, the spread between the Queensland Heavy Steer Indicator and the EYCI has been following a similar trajectory – albeit much higher – in 2021 as 2017. That’s until this month, with the spread now seeming to be increasing at a much steeper rate than in 2017. Usually, the winter months are when the EYCI trades at the highest premium to the heavy steer in Queensland, including in 2017. Victoria trends the other way, with the spread at its smallest through winter and the start of spring, with the 10-year average showing the Heavy Steer price trading inline with the EYCI, and occasionally at a premium. In 2017, however, the two prices didn’t converge until September, which is when the EYCI started to dip from its peak. NSW is perhaps behaving closest to expectation, with the price spread growing at this time of year.

What does it mean?

The common denominator with all states for April has been further divergence between the EYCI and the heavy steer price, as supply remained tight and restocker confidence strengthened. While this trajectory isn’t seasonally uncommon, a price spread of 20-28% sure is. That gap will have to begin to close, regardless of the state, but with processors currently influencing young cattle prices very little, it’s hard to see the spread reaching the 70% range in the short term. Long term, they need to come back together, and with Australian cattle prices already some of the highest in the world, heavy steer prices won’t be the indicator to make the move.

Have any questions or comments?

Key Points

- The Eastern Young Cattle Indicator hits a new high of 910¢/kg, rallying at 200¢/kg higher year-on-year.

- Restocker and feeder competition continues to outpace processors, with the eastern Heavy Steer Indicator (370¢/kg), only 100¢/kg higher year-on-year.

- Queensland price spread is the highest, diverging by a record 28 per cent at the close of last week, with Victoria the lowest on the east coast at 20%.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: MLA, Mecardo