In late August we looked at the Ifo index for German manufacturing (a proxy for demand in the merino market) as a guide to the trends we should be seeing in the merino market. Two months down the track it is time to update the data to see what external demand pressures on the merino market are doing

The August article explained why the German Ifo Index is useful as a guide to the cycles and trend demand for merino wool. The correlation between the Ifo indices and wool prices is not perfect but the bigger cycles do match up well and we are going through a bigger downturn (from the German perspective) currently, so it is time to pay attention.

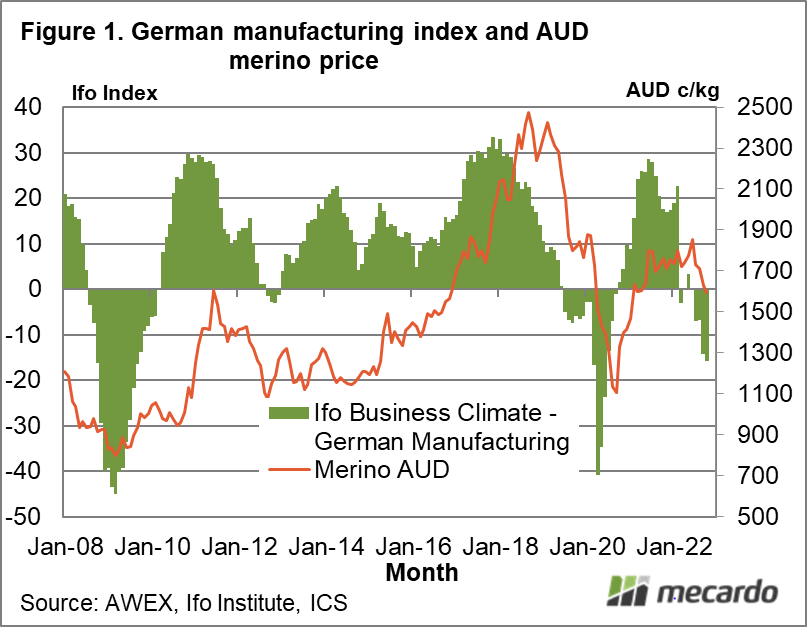

Figure 1 compares the average merino price, in Australian dollar terms, from 2008 through to this month as well as the Ifo German Manufacturing Index. The key information from the current market is that the Ifo index used here (there are quite a range of indices published by the Ifo Institute) is still falling and is at levels now which has only been exceeded in 2020 (pandemic) and 2008-2009 (financial crash). The index is falling and continuing to put downward pressure on prices from the demand side of the market.

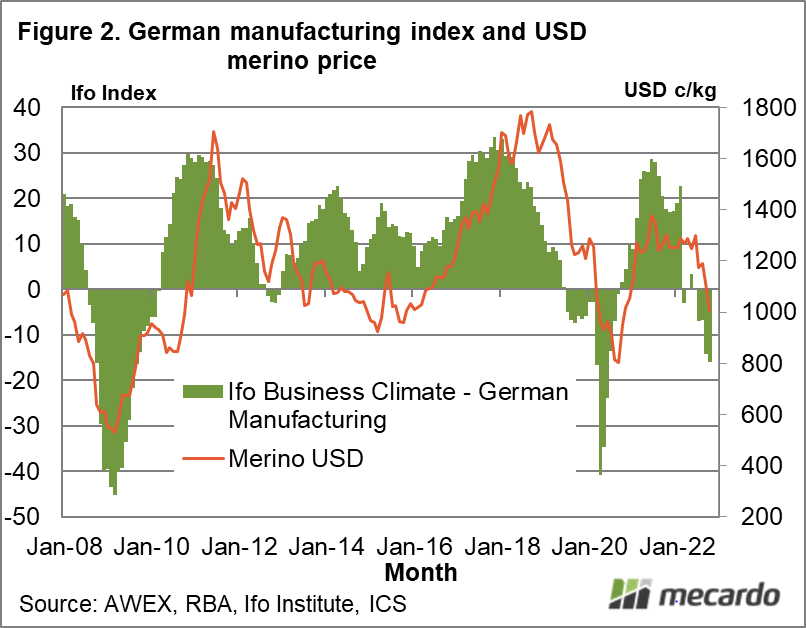

In Figure 2 the process is repeated, using the average merino price in US dollar terms. Without the floating Australian dollar “muddying the waters” the correlation between the wool price and the fluctuations in the Ifo index show up more clearly. It is the same story as in Figure 1 but told more forcefully – there is downward pressure from the demand side on wool prices.

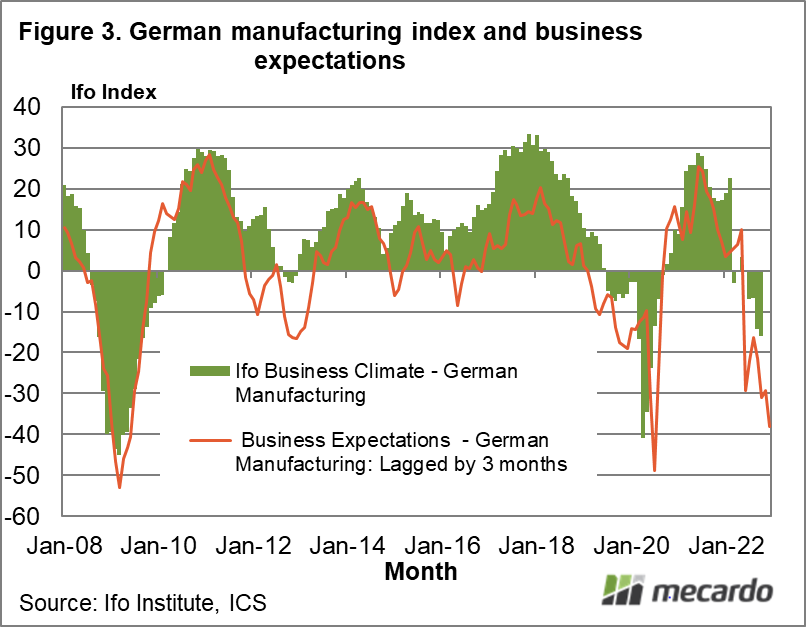

The Ifo Institute also surveys business expectations, in addition to current conditions. The business expectations indices tend to be more volatile (that goes with guessing the future) but they provide a short term lead on where the current conditions are going. In Figure 3 the business expectations for German manufacturing are compared to the Ifo index for manufacturing, with expectations lagged by 3 months. This schematic puts the current downturn on par with 2020 and 2008-2009, which is a worrying comparison. One comfort is the rebound in wool prices out of the two earlier downturns was relatively quick.

What does it mean?

In late August the conclusion was that the falling trend in the Ifo index was likely to continue, which has proved correct. The monthly average merino price for October is 15% below that of August in US dollar terms and a more moderate 7% lower in Australian dollar terms. The business sentiment index indicates the trend will continue for at least the short term (1-2 quarters), which in turn points to a continued weakness in demand for merino wool through to the autumn.

Have any questions or comments?

Key Points

- The Ifo manufacturing index continues to fall.

- The Ifo manufacturing business sentiment index (a short term lead indicator on the main index) also continues to weaken.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: AWEX, RBA, Ifo Institute, ICS