It wasn’t that long ago we produced an article talking about the record premium of young cattle prices over those of lamb. How things have turned, with the two now almost at even money.

In October 2022, we discussed the record premium for cattle over lambs. At that time lamb prices had declined as the post-rebuild supply arrived, and some processing bottlenecks depressed values. In contrast, cattle prices were still flying high, having bounced from Foot and Mouth Induced decline to sit close to historical records.

It was more by coincidence than by design that it turned out to be the very top of the cattle premium. It should be of little surprise, with young cattle trading at a 40% premium to lamb something had to shift.

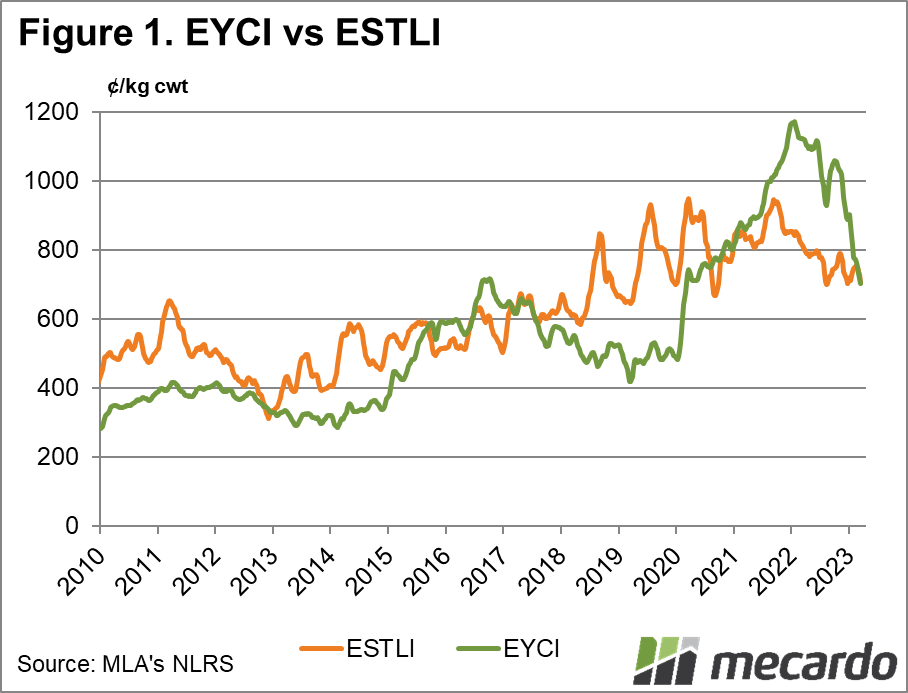

Figure 1 shows that since October last year, lamb has largely traded sideways, at least compared to cattle. Since October, the Eastern Young Cattle Indicator (EYCI) has declined an extraordinary 38% and has broken through a key support level of 700¢/kg cwt.

The lamb decline was nothing like cattle, with the Eastern States Trade Lamb Indicator (ESTLI) losing 22% from 2021 peaks to 2023 lows. We can see in figure 1 that while lamb prices have been bouncing around, they are largely holding in the 650-800¢/kg cwt range.

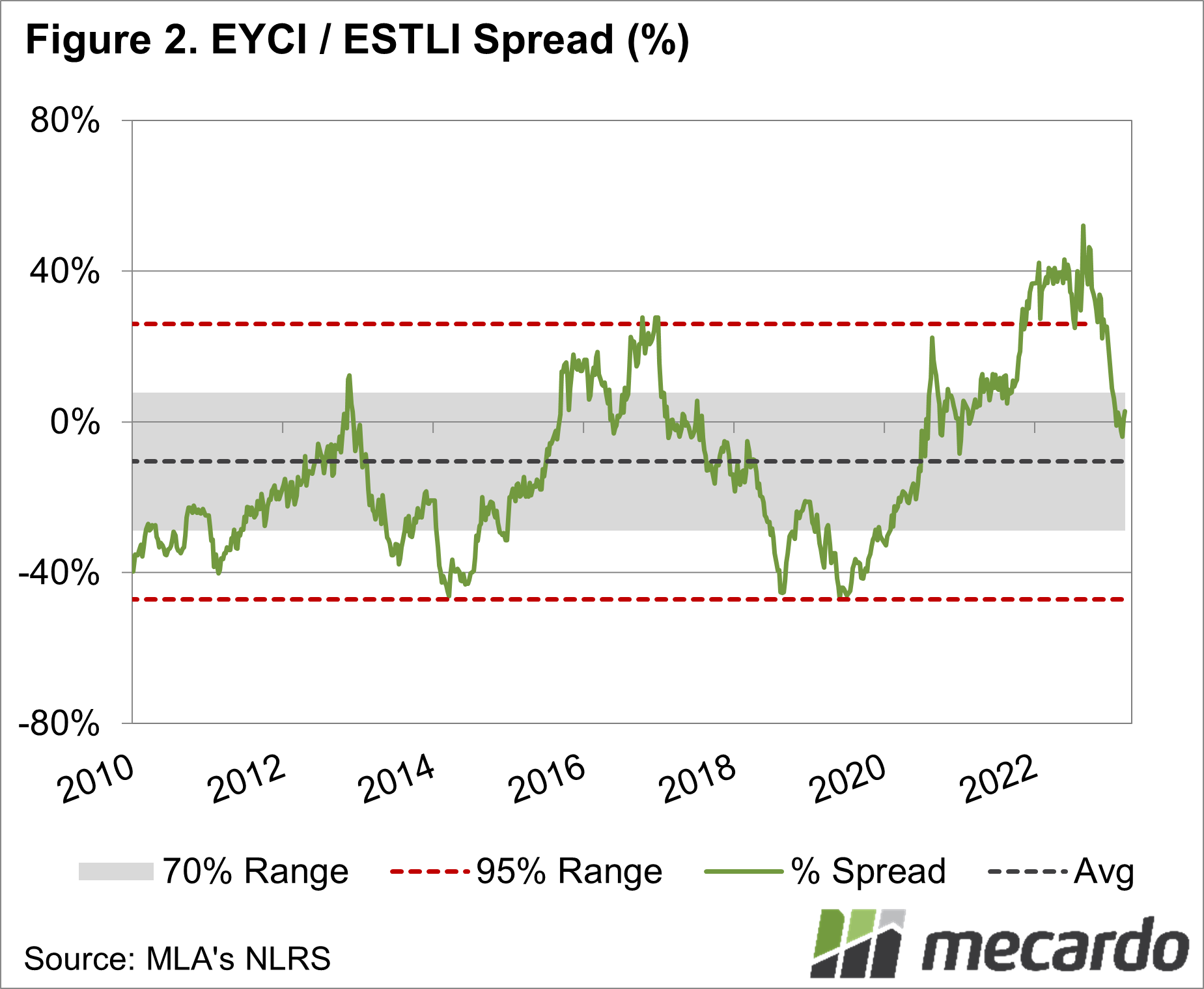

Figure 2 shows the EYCI spread to the ESTLI. From above 40% in October the EYCI last week was at just an 18¢, or 2.7% premium to the ESTLI. Historically lamb has been slightly more expensive than young cattle, with the EYCI averaging a 10% discount to the ESTLI. The spread is never steady for long, with cattle at big discounts during drought, and at a premium during better times.

Back in the article last October, we suggested it was a good time to get out of cattle and into sheep. As it turns out it would have been a masterstroke, and even better if cattle were simply sold and bought back in now. Hindsight is a wonderful thing.

What does it mean?

Where the EYCI & ESTLI spread heads from here depends on the season. The broad consensus is that there will be some upside for cattle at a global level, but growth in the herd will stymie rises here, especially if the season turns drier than normal.

The narrowing of the spread is bad news for lamb at a broader level. Lower cattle prices will eventually lead to cheaper beef at retail, which could see some substitution at the consumer level domestically.

Have any questions or comments?

Key Points

- After hitting a record in October the EYCI premium to the ESTLI has disappeared.

- The spread has narrowed due to a heavy fall in cattle prices, and steady lamb values.

- Where the spread heads from here is highly dependent on how the season pans out.

Click on figure to expand

Click on figure to expand

Data sources: ABARES, Mecardo