2023 was a year that severely challenged the marketing plans of sheep and lamb producers, with dramatic moves in the market rarely seen. Certainly, the scale of the market moves was not typical of the normal seasonality we come to expect of the sheep market.

The Bureau of Meteorology (BOM) issued an El

Nino “watch” in March, which was subsequently upgraded in June to an “alert”. By the time the formal declaration that

Australia was under the influence of an El Nino weather pattern in September,

livestock markets had already reacted to the risk of impending dry conditions.

The Eastern States Trade Lamb Indicator (ESTLI) had dramatically fallen from

the January year-high point of 812¢/kg cwt to sit in late September at 431¢, a

381¢ or 53% fall over the 8 months!

Mutton fared even worse, with the National

Mutton Indicator (NMI) coming from the year high in February of 378¢ to bottom

out in late October at 102¢, a 276¢ or 73% retracement.

While other factors contributed to one of

the most dramatic market corrections ever seen, the response by producers to

the risk of another dry season was the key ingredient to the collapsing

markets. Sellers were trying to reduce their stock numbers before feed and

water ran out, and restockers and traders were hesitant for the same reason as

well as not being keen to jump into a falling market.

The other consequence of this response was

to see the light lamb market also struggle to attract any restocker interest. In

the previous two seasons, almost all the light unfinished lambs offered to the

market found willing buyers who were prepared to feed these lambs to heavier

weights; reselling them in the late Summer & Autumn.

Fortunately, the cheaper lamb market

brought back a previous buyer. The Middle East & North Africa (MENA)

regions had been a strong buyer of light lambs, sometimes called “bagged

lambs”. These are lambs in the 12 to 18 kg CWT range that are usually

airfreighted as whole carcasses. From the middle of 2023, as this market pulled

back, the MENA buyers stepped in. Mecardo estimated that almost 900,000 lambs

headed to this market in the four months to November (read here).

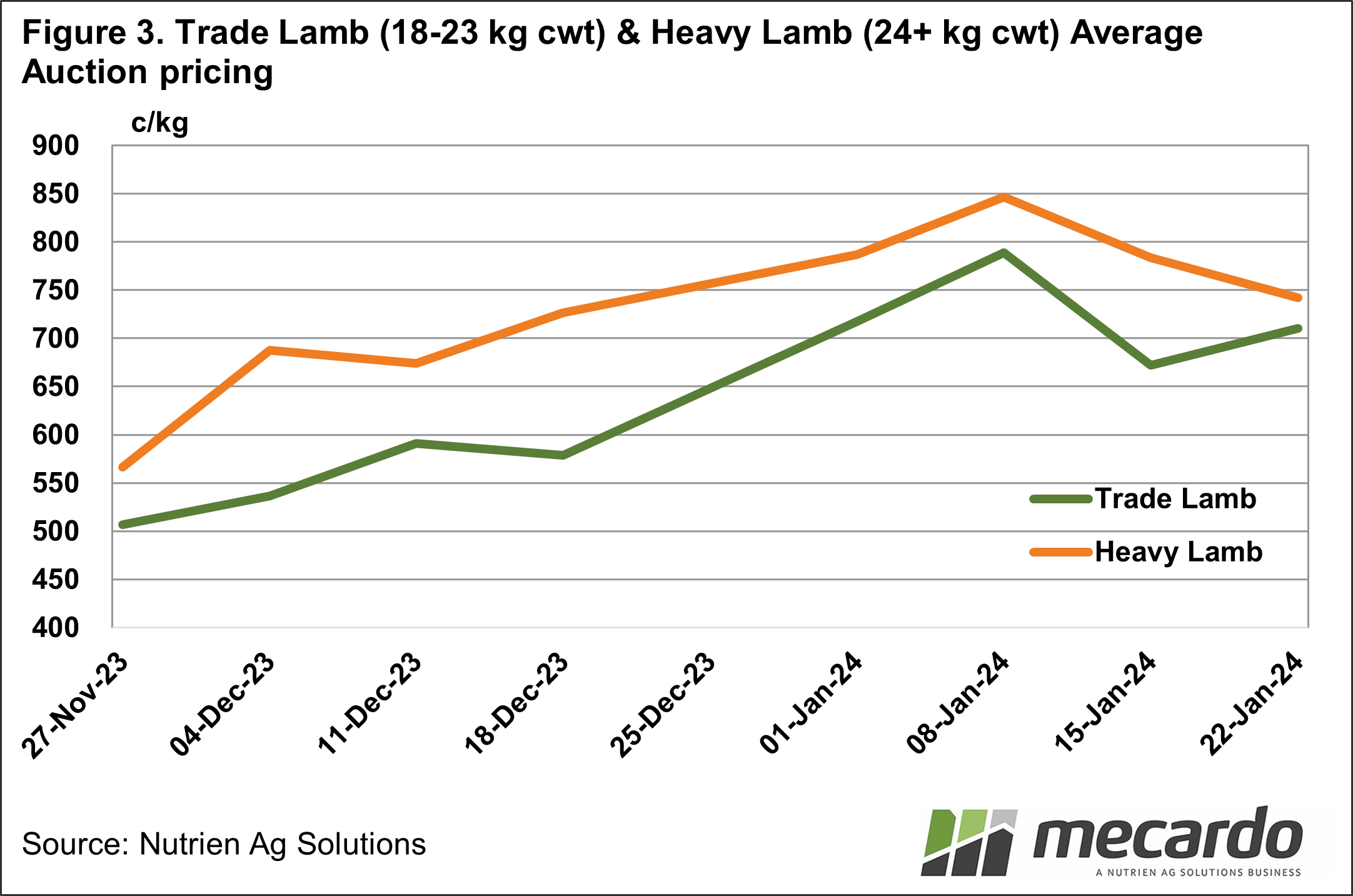

To gather some more detail to accompany these

higher-level observations, we have used auction sales data of stock sold by Nutrien Ag Solutions® or associated agents in December and January. Broadly speaking, this confirms that when the November rain

arrived, followed up by further December falls on the East Coast, markets

improved. The arrival of restockers and lamb backgrounders was the spark that

ignited the markets. Comparing the early December prices to the first &

second week in January sheep & lamb prices, trade lambs had a 56% rally,

while heavy lambs were up 49%.

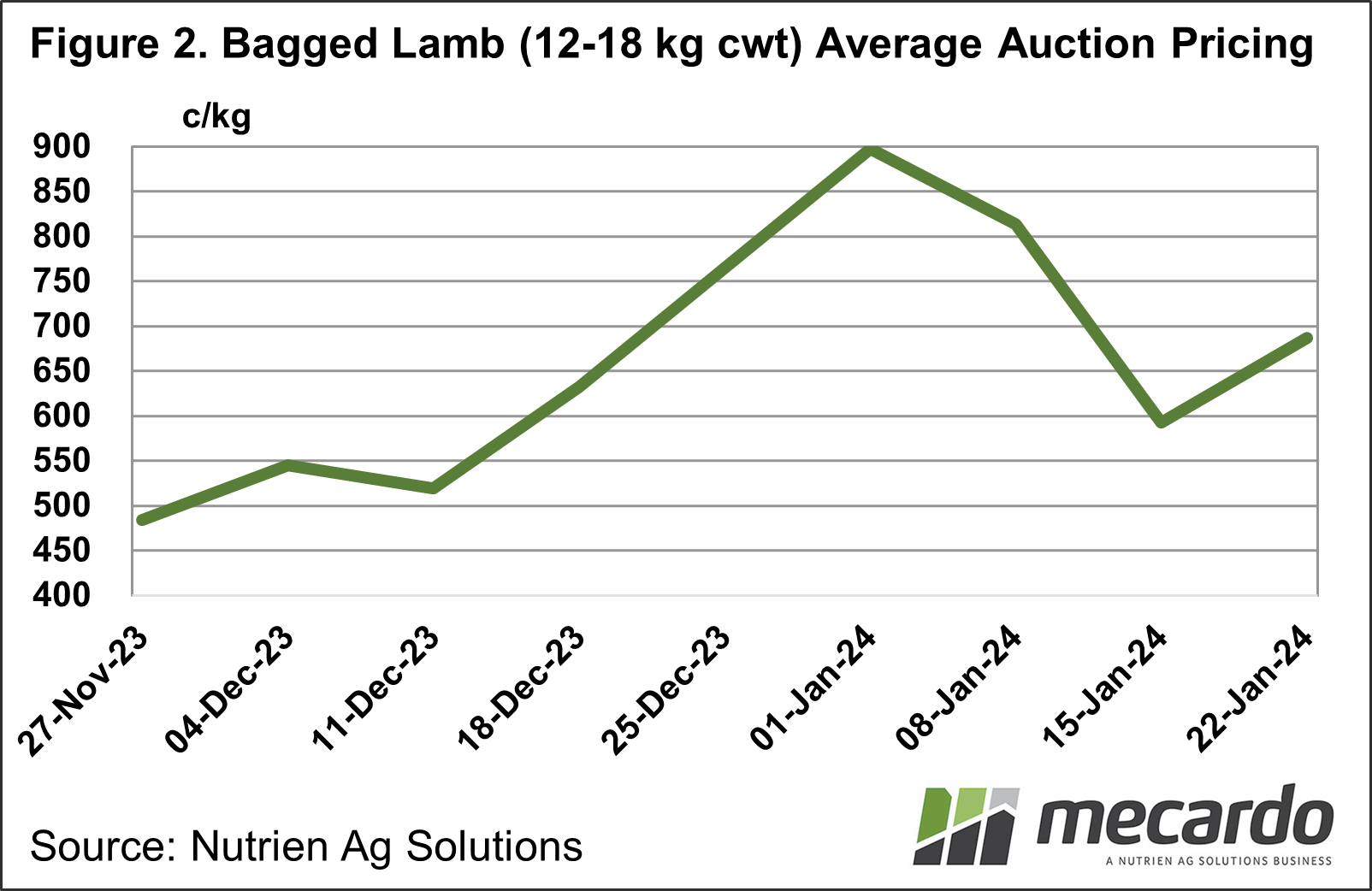

For “bagged” or light lambs, the emergence

of restockers with confidence in their feedbase after the summer rains, added

competition lifting pricing from the early December quote of 484¢/kg cwt to

above 800¢ in the first two weeks of January 2024. In fact, in the first week

of 2024, this market peaked at 897¢, an 85% lift on the early December quote.

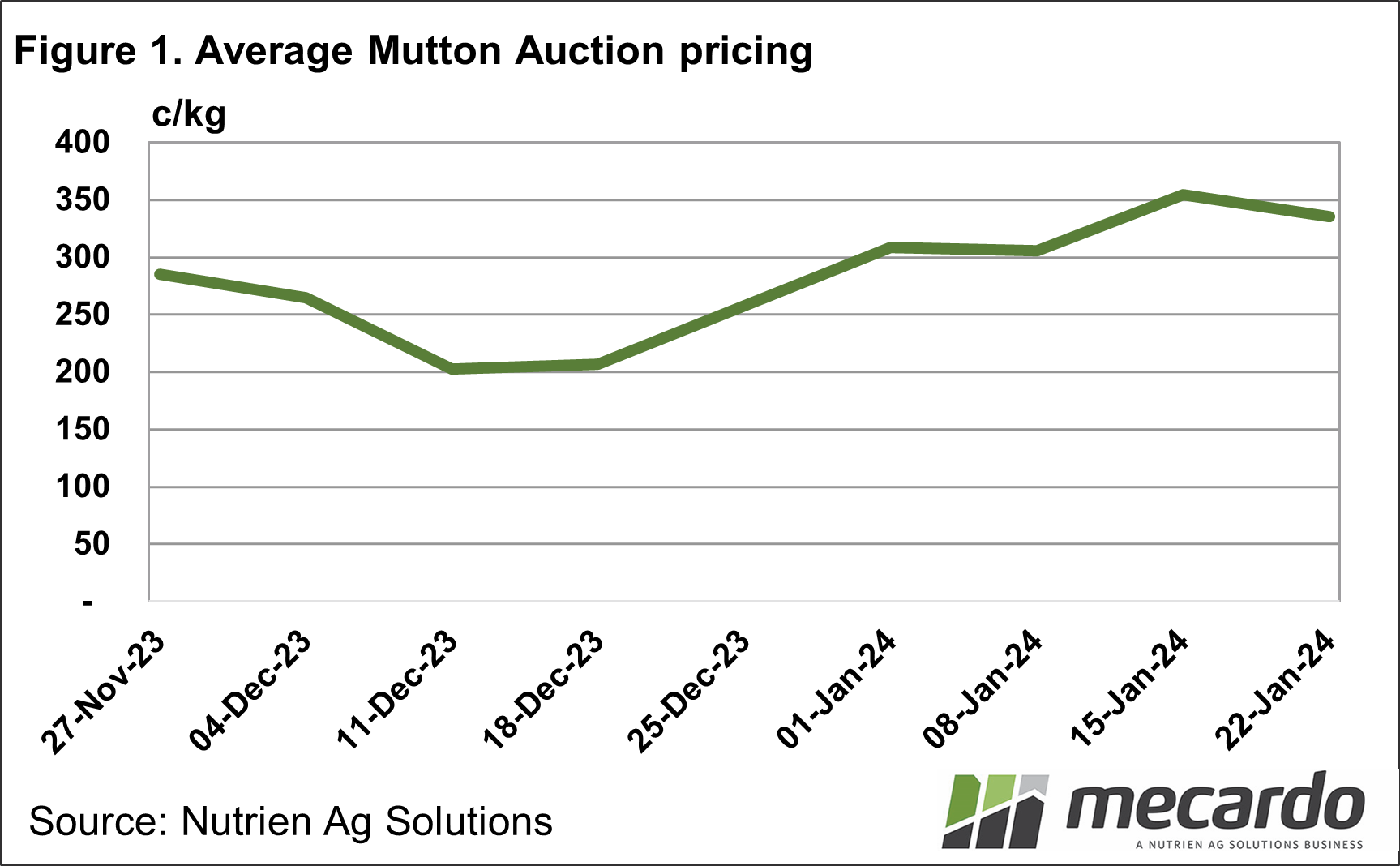

Mutton prices have also lifted, albeit a

couple of weeks lag to the lamb market. From a low at saleyards of 202¢, it

produced a 75% rally over the two months. Mutton still looks cheap, so as lamb

supply eases, we could well see further increases in the mutton market as

processors look to maintain their slaughter numbers.

What does it mean?

While the sheep & lamb markets have steadied, the response of producers to the season-changing conditions has no doubt been influential. Anecdotally, some producers with stock still to sell are now re-considering the timing. Add in traders looking to convert abundant available feed into meat & income, and the context of the market has all the ingredients of providing a vastly different scenario going forward than was looking likely three months ago.

Have any questions or comments?

Key Points

- There has been a strong recovery in Sheep and lamb markets post-summer rain.

- MENA markets supported light lambs during market lows.

- Restockers stepping in has contributed to market improvement.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: MLA, Nutrien Ag Solutions, Mecardo