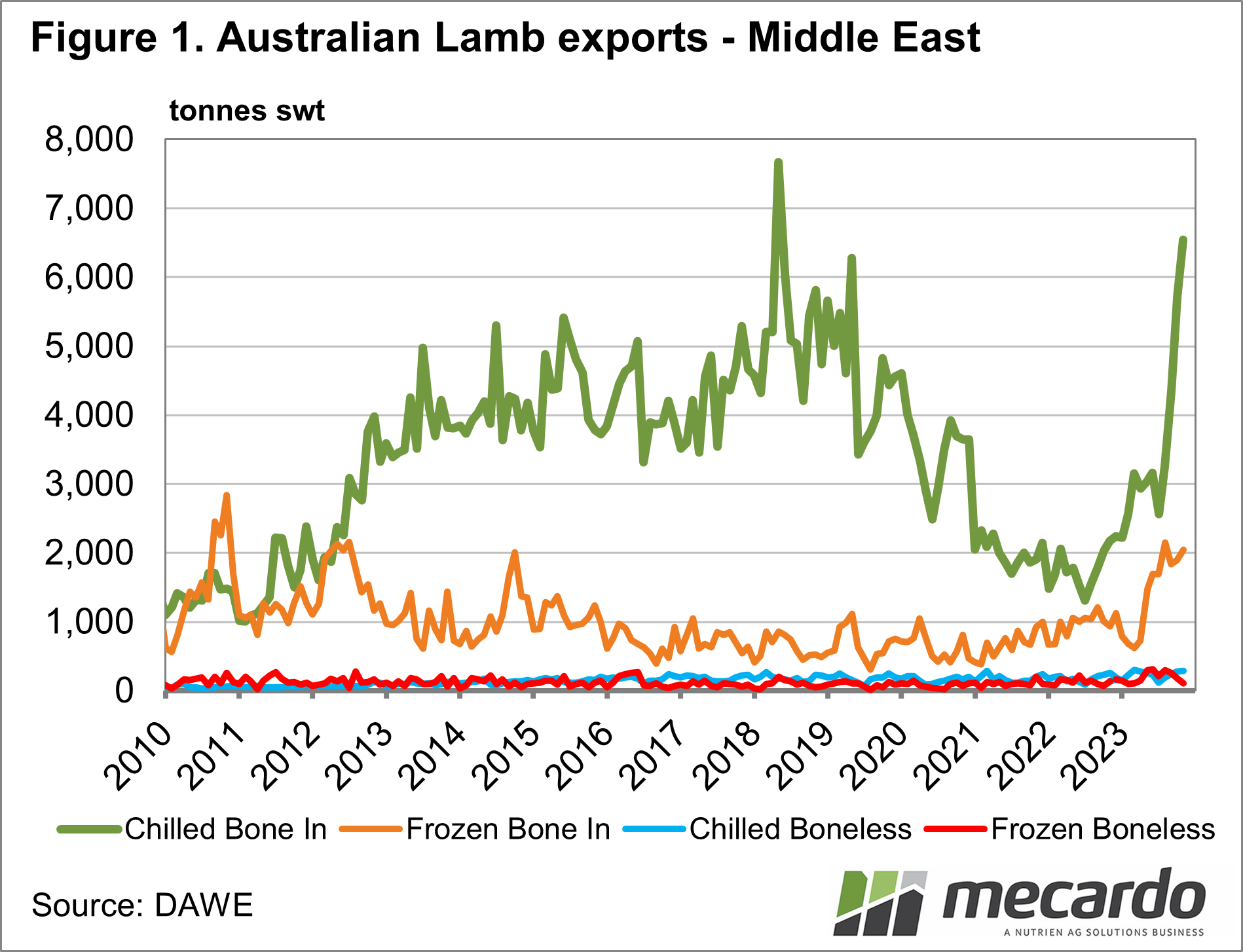

For a few months now we’ve been tracking lamb exports to the Middle East. This data has been backing up the anecdotal reports regarding the number of light lambs that have been heading to slaughter rather than back to the paddock or the feedlot. New saleyard data is adding to the evidence that tighter supply might be coming.

The November

lamb export data showed further increases in exports to the Middle East, with

the chilled bone-in category taking another jump. Figure 1 shows chilled bone-in lamb exports

to the Middle East jumping another 14% higher, and hitting the second-highest

level on record.

The Middle

East traditionally takes lighter lambs, which can be exported whole. This market has seen huge growth this year,

with lighter lambs cheaper on a ¢/kg basis than trade or heavy lambs.

Over the

last four months, over 16,000 tonnes more lamb has been exported to the Middle

East than last year. Some rough numbers put

the number of extra lambs that have gone to the Middle East at close to 900,000

head.

It’s

interesting to note that nationally just over 1 million more lambs have gone to

slaughter from August to November, compared to 2022. Not all these lambs would have gone back to

the paddock last year, and there are likely more lambs available this year, but

the early exit of lambs in the spring is no doubt having an impact on supply

now.

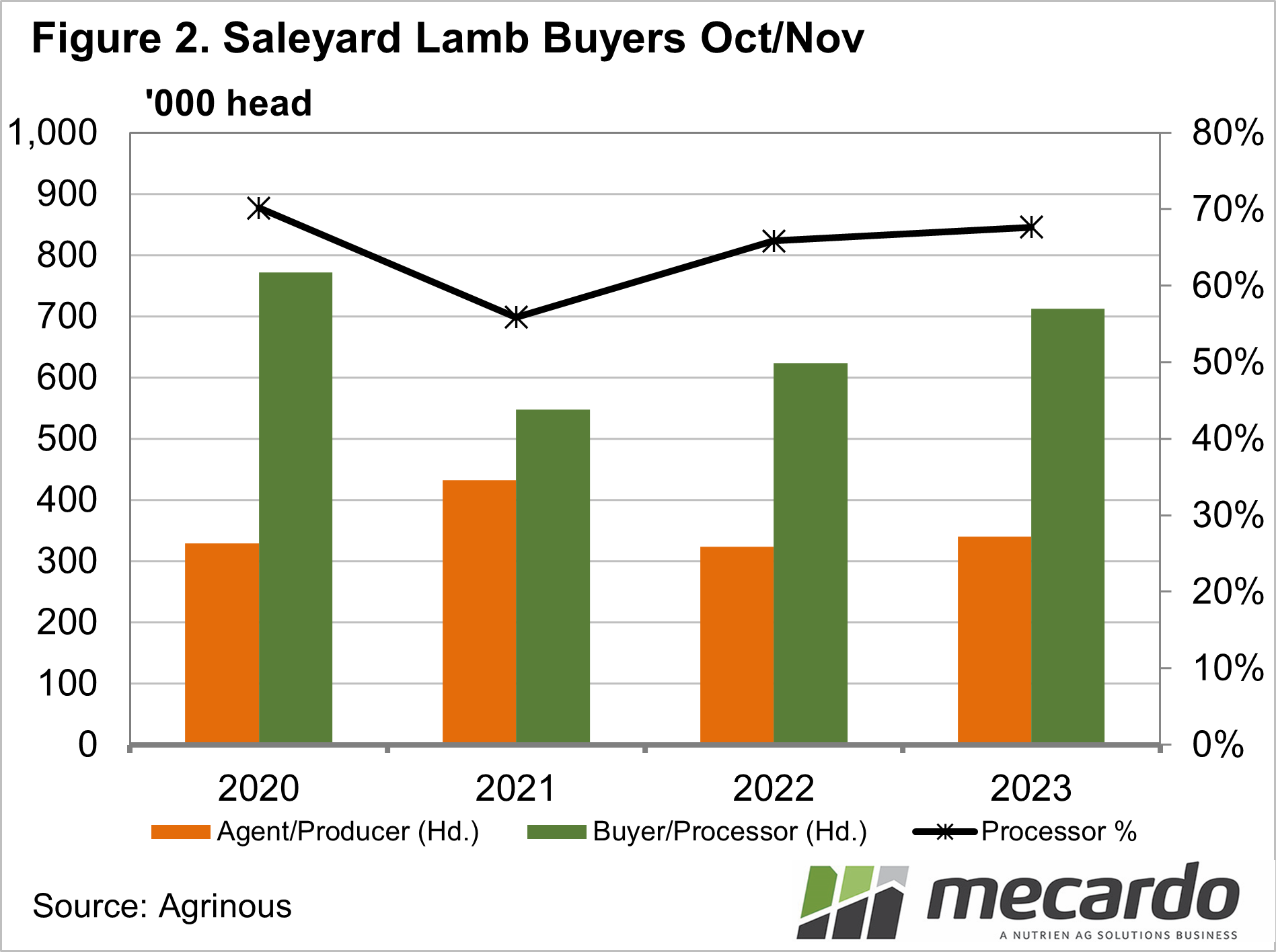

We can see

in 2023 more lambs have been yarded than in 2022, and while the increase in the

proportion bought by processors was only small, the total was over 100,000

head. There was a major shift in buyers

in 2021, as more lambs went back to the paddock in a good season. Last year the lambs that didn’t find their

way to saleyards likely stayed home.

Agrinous

also records the price of lambs. This

year the average price has been $90.86/head, down from $155.98 last year. Processors have paid on average $103 per head

this year, down 40% on 2022. Agents and

producers have paid $64.8 per head, down 47%.

This is another indication of weaker demand from restockers and feeders,

allowing processors to buy more light lambs.

What does it mean?

The current dearth of finished lambs is no doubt in part due to the early exit of more light lambs this year. The lighter lambs of August to October would have been the trade and heavy lambs of now. The next question is whether the increase in the light lamb kill in November will exacerbate the trend in the coming months, or whether the increase in total lambs will be enough to compensate.

Have any questions or comments?

Key Points

- Lamb exports to the Middle East continued to increase in November.

- Processors have bought more lambs at saleyards, and slaughter is up.

- Weak supply of finished lambs is in part due to the early exit of lambs from August to October.

Click on figure to expand

Click on figure to expand

Data sources: Agrinous, MLA, DAFF, Mecardo

Categories

Have any questions or comments?

What does it mean?

While lot feeders have been benefiting from the falling young cattle prices, they’ve also been facing plenty of other rising costs this season, as well as lower finished cattle prices themselves. Lower turnoff numbers well outweigh the higher number of total cattle of feed, showing they were less active for the quarter than those numbers might demonstrate.

Record high capacity and strong utilisation, teamed with the record high grainfed beef exports, all demonstrate a growing sector that is confident of progression despite the extremities of the market in the past 12 months.