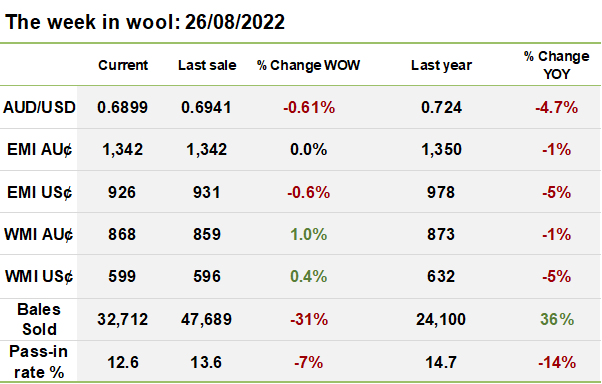

A much smaller offering due to no sales in the west saw strong buyer support across most indicators. There were some significant falls for the 17-18.5 MPG’s in Melbourne, but lifts in their Sydney counterparts saw the EMI stay put for a second week in a row.

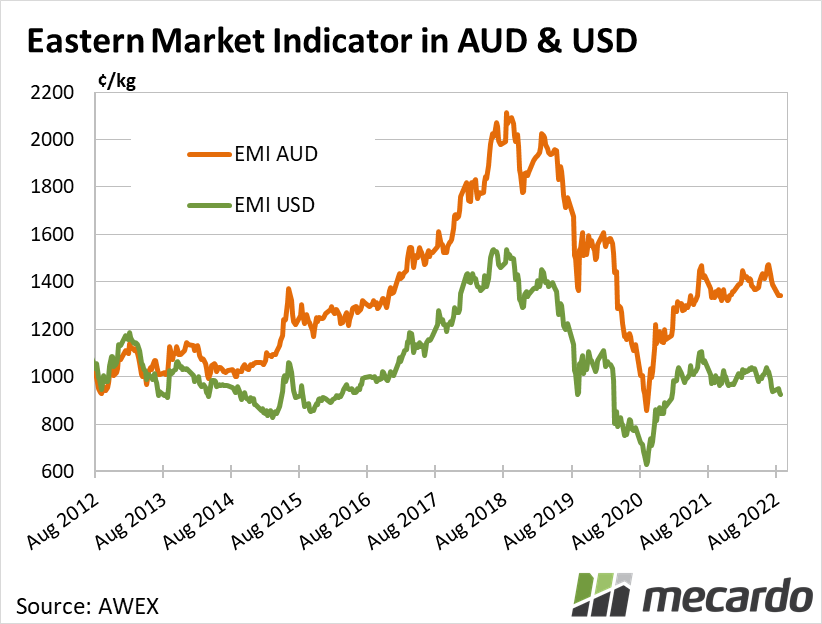

The EMI is at 1342ȼ/kg for the third week in a row, although like last week, due to a continued weakening in the aussie dollar (down 0.42ȼ), in US dollar terms the EMI fell again, down 6 cents to 926ȼ/kg.

Most of the micron categories lifted on the week prior in Sydney, albeit modestly, by 1 to 9 cents, bar the 16.5 and 17.5 MPG’s which fell 8 & 6 cents respectively. There were bigger falls in Melbourne with the 17 to 18.5 MPG’s down between 5 & 36ȼ’s. Falls in the south were balanced out by rises in the north, hence the EMI didn’t budge again.

Looking at crossbreds and in Melbourne only the 26 micron lifted, by 8 cents, while the 28-32 microns all fell between 3 and 12 cents. There was no movement for the crossbred indicators in Sydney.

Cardings had a positive week, lifting 9 cents in Sydney and 15 in Melbourne.

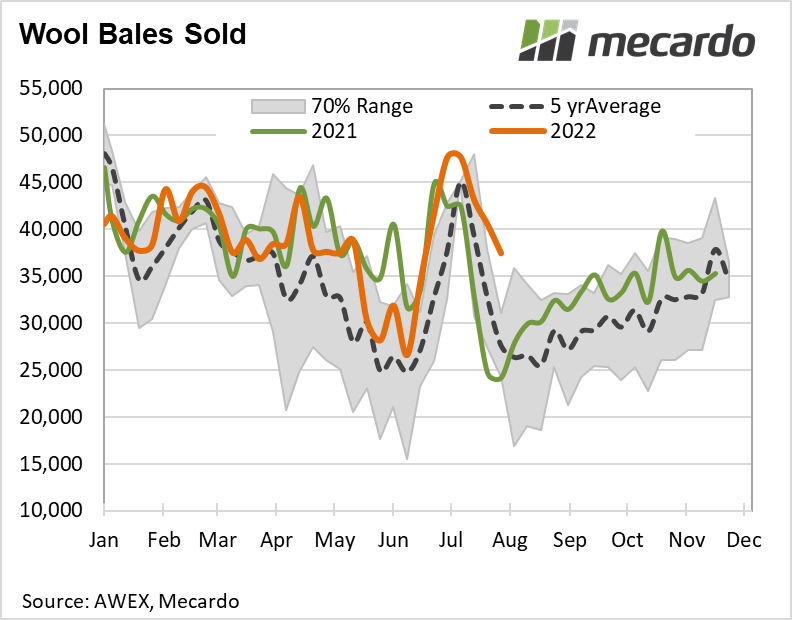

There were significantly less bales on offer this week due to no sales in the west. 37,431 bales were offered, with a pass-in rate of 12.6%, resulting in 32,712 bales sold, the lowest amount so far for the 2022/23 season. The average bales sold for this season is still nearly 5,000 bales higher than last season.

This week on Mecardo, Andrew Woods took a look at correlations between the performance of the German manufacturing sector, via the IFO index, and merino prices both in AUD & USD. Andrew also took a look at the recent performance of short staple length wool, via 10 year percentiles.

The week ahead….

Next week WA is back in the fold, and as such we have a bigger offering – there are 39,192 bales scheduled for sales across the 3 main centres on Tuesday and Wednesday.

Have any questions or comments?

Click on graph to expand

Click on graph to expand

Click on graph to expand

Data sources: AWEX, AWI, Mecardo