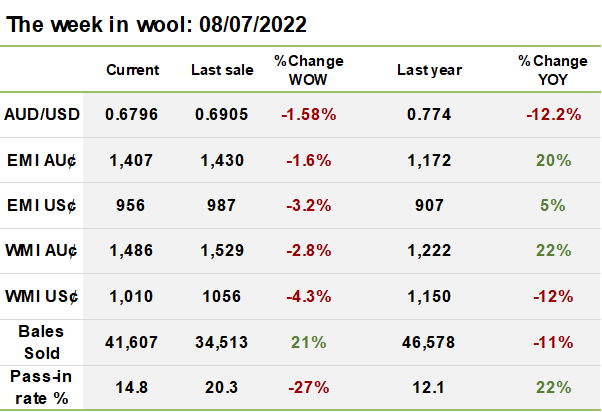

Supply overwhelmed the first week of the new selling season as a big offering of wool for sale was met with a softer market. The cheaper Australian dollar wasn’t enough to overlook the concern with commodity prices tanking around the globe.

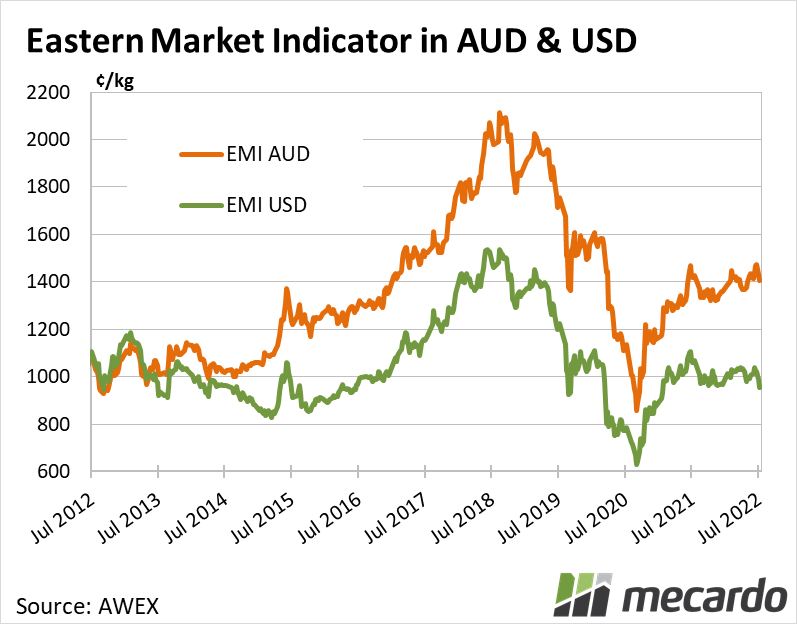

The Eastern Market Indicator dropped 23¢ or 1.6% over the week, settling at 1407¢/kg. For comparison, at the end of the first week of the 2021/22 season the EMI was slightly higher at 1420¢/kg. The Australian dollar continued to trend lower alongside the crash in many commodities on the fear of recession. At 0.6796 USD the Aussie is at the lowest level in over two years. In US terms, this pushed the EMI 31¢ lower to 956¢/kg.

Fremantle wasn’t immune to the market pressures. It faced the largest losses of all three centres. The Western Market Indicator shed another 43¢ to 1486¢/kg.

Continuing the trend of last week, all medium to fine fibres recorded losses. Fine wools in Melbourne were down 25 to 60¢, and 30 to 50¢ in Sydney. 20MPG in Melbourne avoided the significant falls, but was still 7¢ softer. The damage in Sydney was done on the first sales day, with some MPG’s recouping some of the earlier losses on Wednesday due to better quality wool.

Results were mixed amongst crossbred wools. The 26 MPG recorded a 14¢ gain to 705¢ while 28-30 MPG moved slightly lower. Merino cardings dropped 9 and 10¢ respectively in Melbourne and Sydney, and improved 2¢ in Fremantle.

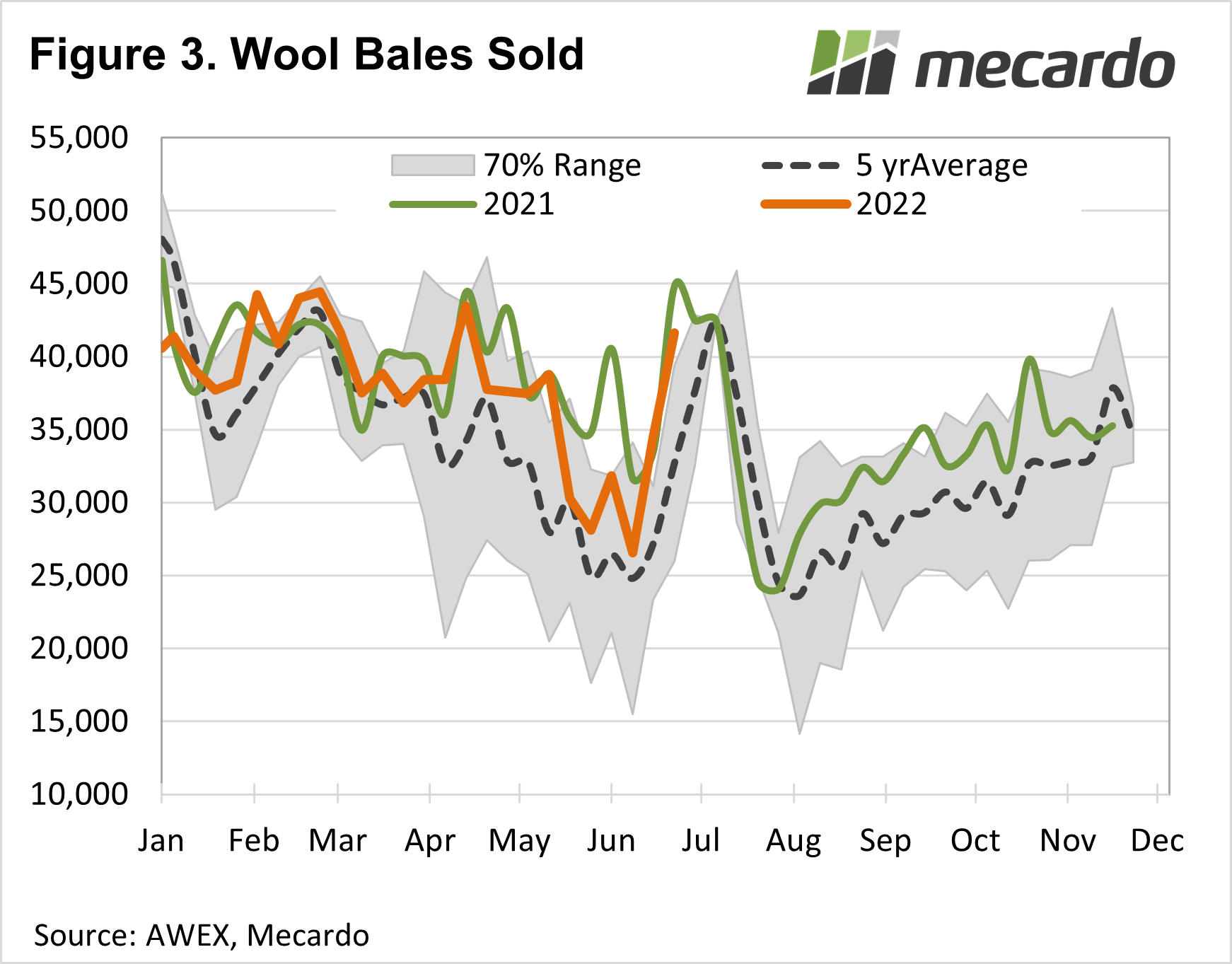

Despite the weaker market, less wool was passed-in at auction compared to the week prior. The national pass in rate of 14.8% saw 41,607 bales sold.

While the 2021/22 is now behind us, our analysis this week looked at how the full season fared for crossbred, fine & broad Merino wool compared to history. Supply chain expenditure on fine merino wool was the third highest since the mid-1990s last season. While the gross sales value of crossbred wool picked up slightly last season, it remains at half of the level enjoyed in the eight seasons to 2018-19.

The week ahead….

The last sale before the three week recess is expecting 61,054 bales on offer across the three selling centres. As noted by AWEX, this will be the largest week of sales since week 36 in 2019/20 if the quantity eventuates.

Have any questions or comments?

Click on graph to expand

Click on graph to expand

Click on graph to expand

Data sources:

AWEX, AWI, Mecardo