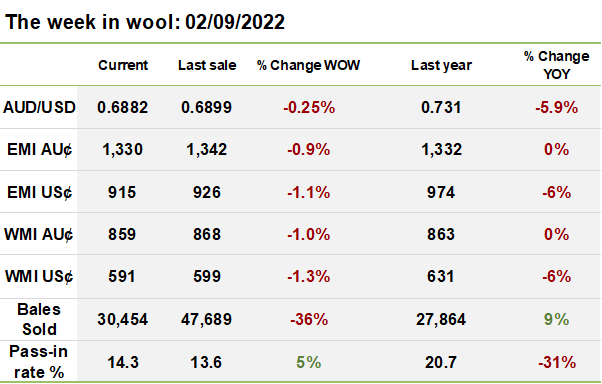

After two weeks of minimal price movements, the wool market has recorded considerable falls this week. As reported by AWI, ‘subdued competition and lacklustre off shore demand’ saw most microns fall as sales progressed, with most indicators finishing in the red.

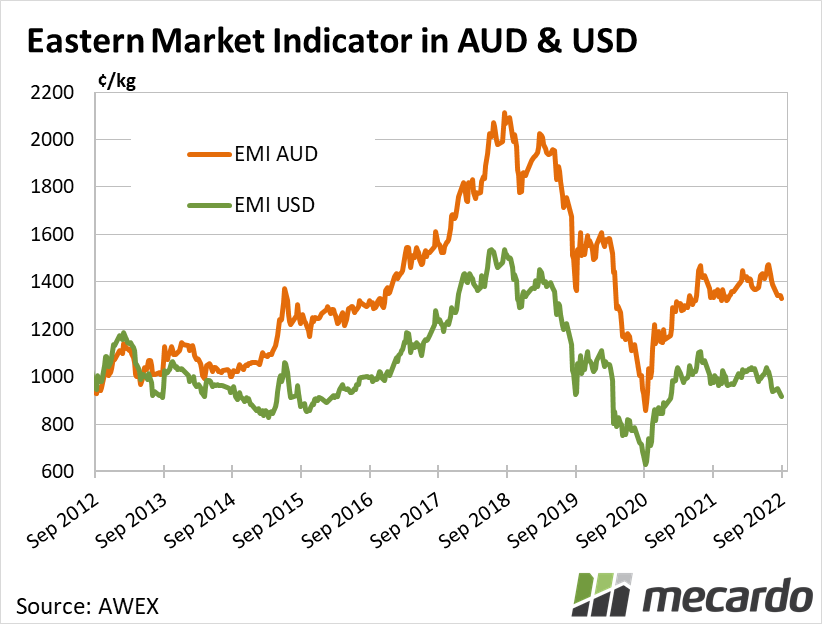

After three weeks of not moving, the Eastern Market Indicator (EMI) lost 12ȼ this week, falling to 1330ȼ/kg and due to a continued weakening in the Aussie dollar (down 0.17ȼ), in US dollar terms, the EMI fell 11ȼ to 915ȼ/kg.

There were some significant falls, particularly for the finer microns in Melbourne which dropped between 40 to 76 cents. The finer microns in Sydney had mixed results with some modest lifts and falls ranging between -12 to +11 cent changes. Over in the west, the finer microns fell between 20 to 62 cents with the Western Market Indicator (WMI) indicator losing 18ȼ to finish the week at 1441ȼ/kg.

The medium type microns were mostly in the red, although in Sydney the 19.5 & 20 MPG’s lifted by 1 & 11ȼ respectively. The 19.5 – 21 MPG’s in Melbourne were weaker and the 22MPG lifted 15ȼ.

Crossbred indicators fell between 2 to 5 cents, except for the 26 MPG in Melbourne which rose by 11ȼ to 669ȼ/kg. Cardings continued its downward spiral, dropping 9 cents in Sydney and Fremantle and by 17 cents in Melbourne.

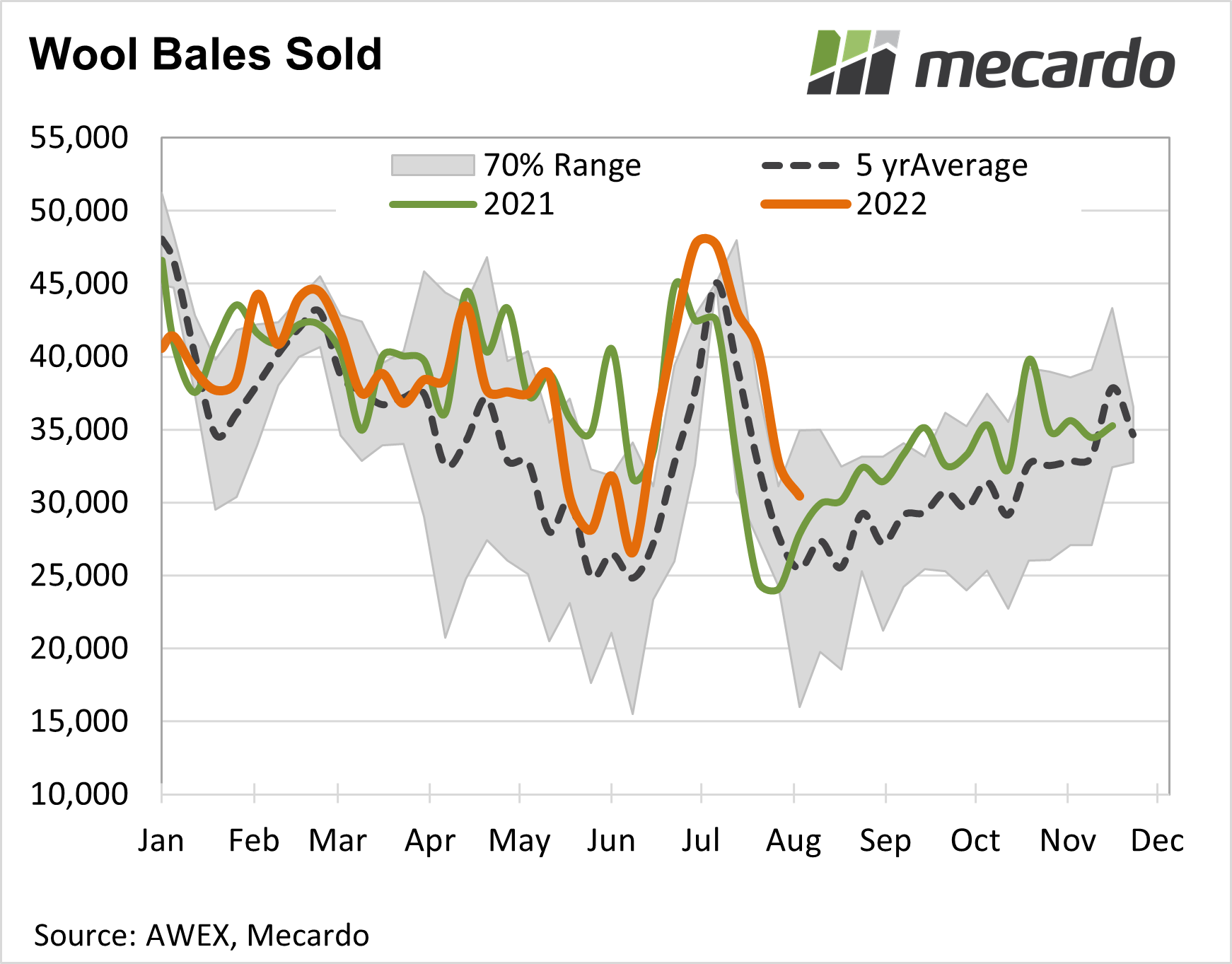

Even with Fremantle back in the mix, the offering was considerably smaller than the first three weeks post-recess break, with just over 35,000 on offer. The pass-in rate was a little higher than last week at 14.3%, resulting in 30,454 bales sold. This was the lowest amount so far for the 2022/23 season. The average bales sold for this season is back under 40,000 now and getting closer to the average bales sold of last season, which was 36,146 per week.

This week on Mecardo, Andrew Woods revisited mohair prices in South Africa, demonstrating a strong correlation with finer micron price movements over the past 10-15 years and also a rapid uptake of the RWS equivalent for mohair, RMS, since auction data for RMS accredited wool has been published in mid 2020. Andrew also followed up from his article last week on RWS premiums in Australia for ‘short staple’ wool by taking a look at equivalent premiums in South Africa.

The week ahead….

Next week sales are on Tuesday and Wednesday at Melbourne, Sydney and Fremantle with 39,562 bales currently on offer. The EMI hasn’t been this low since mid-November 2021, and has not recorded any positive movements this season to date – it will be interesting to see what happens next week whether the trend downward continues or whether we will see a reversal in this seasons direction.

Have any questions or comments?

Click on graph to expand

Click on graph to expand

Click on graph to expand

Data sources:

AWEX, AWI, Mecardo