Last week Mecardo published an article on prices for 60 mm long (“prem”) merino fleece, with a graph looking at the current RWS premiums operating in the category. A further look at the development of these premiums during 2021-22, prompted a more detailed comparison to comparable South African premiums.

As with all of the South African data used in these articles, credit must be given to Cape Wools which supplies this information via its website (view here). As earlier articles have noted, RWS premiums were first published by Cape Wools in late September 2021. Until that point the RWS market in Australia sputtered along with around 1% of merino fleece accredited to this quality scheme, and with little in the way of premiums (on average) in auction sales. The forward/direct market was different but the transparency of this section of the market (approximately 15% of the clip when all non-auction volume is accounted for) is limited.

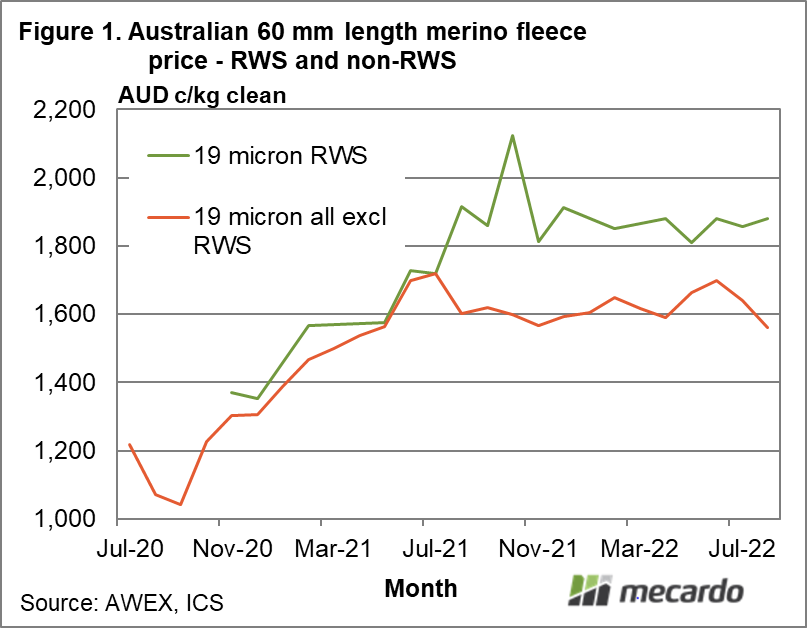

Figure 1 shows monthly average eastern Australian price series for 60 mm prem fleece (the same series as used in the article last week), broken into RWS accredited lots and non-RWS lots. The schematic begins in mid-2020 and runs to this month. Up until August 2021 there is little in the way of price difference between the two series, with the RWS series only appearing in late 2020. From August 2021 a large gap in price (premium) emerges and has remained so since. Keep in mind these are monthly averages, so they will incorporate some lots which may not have picked up the premiums. However the average monthly premium is both large and fairly consistent.

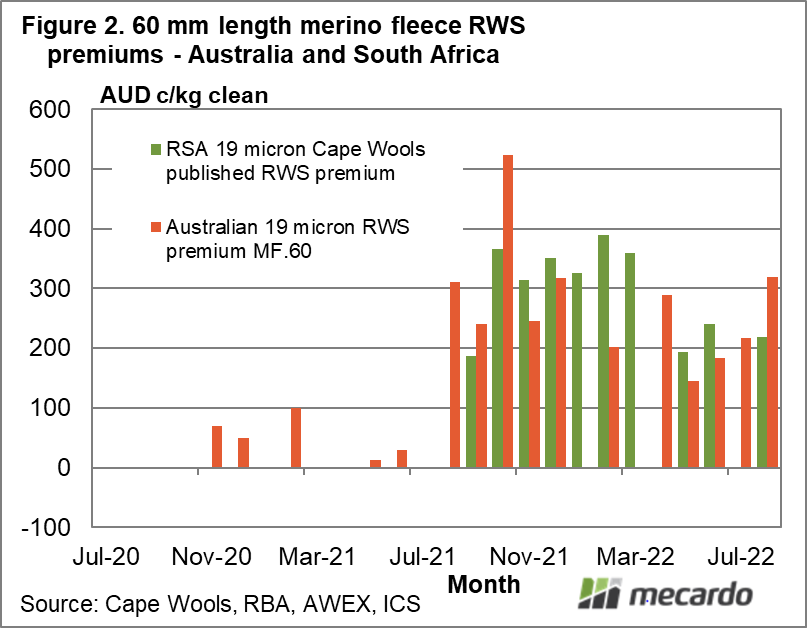

One of the defining features of the South African wool clip (merino included) is the short staple length, with the 60 mm length staple the mode, or most common. Mecardo showed this feature of the clip in an article two weeks ago. Figure 2 has averaged the Cape Wools weekly published RWS premiums for 19 micron across calendar months and expressed them in Australian cents per kg terms, in order to compare with the RWS premiums seen for 60 mm length merino fleece in our market. The Cape Wool premiums only begin in Figure 2 in September 2021, when they began publishing them. From a simple visual assessment it is fair to say the two series are similar. Keep in mind that the South African wool market operated with a ban on exports to China from April through to this month (due to an outbreak of foot and mouth disease), so there has been a weakening in their premiums.

What Figure 2 seems to show is the birth of major premiums for quality integrity schemes (in this case RWS), which apply across different regions of supply.

What does it mean?

Valuing short staple wool is difficult at the best of times, and with the advent of large premiums for RWS accreditation it has become even more difficult. Up until late 2020 there was little supply if any of RWS accredited 60 mm long merino fleece and up until mid-2021 there was little in the way of premiums for this wool. From August 2021 the price structure dramatically changed, awarding large premiums to RWS accredited lots both here in Australia and in South Africa, and most likely in the other merino producing regions of the southern hemisphere.

Have any questions or comments?

Key Points

- The RWS premiums seen in the Australian market for 60 mm long merino fleece began in earnest in August 2021.

- These premiums are comparable to those seen in the South African market, where the main staple length is 60 mm.

Click on figure to expand

Click on figure to expand

Data sources: Cape Wools, RBA, AWEX, ICS