Lamb export figures for the month of November dipped only slightly compared to the same month in 2019, and increased from the October volume. Mutton exports didn’t fare so well dipping 24% year-on-year, and losing 8% from the October total.

While any review of export figures this year should take into account lower slaughter and production because of the improved seasonal conditions across much of the south east – total sheep and lamb slaughter in Australia for the year-to-date is 16% lower than last year – we can gauge some demand factors from the monthly data.

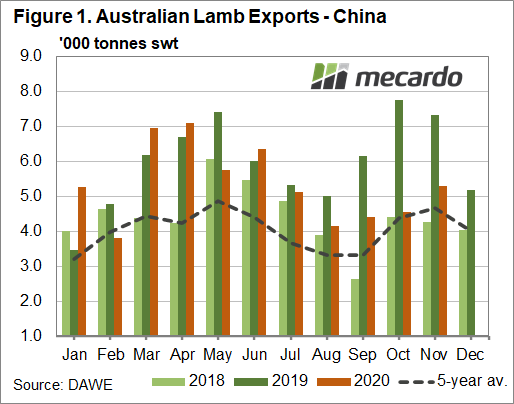

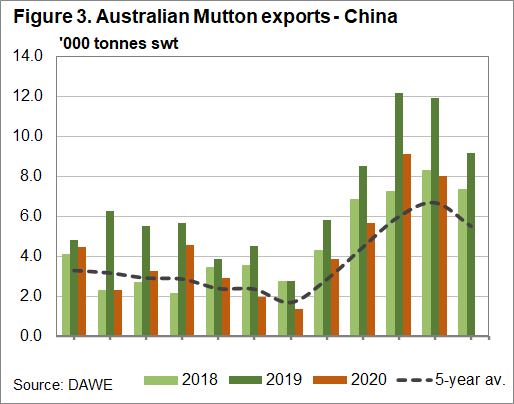

Sheepmeat demand from China doesn’t appear to have been hit any harder in November than any other month this year, despite trade tension between the two countries. Both lamb and mutton volumes to China for November tracked above the five-year-average, and lamb exports increased compared to the previous month. There is no doubt that demand has fallen from the record breaking 2019. However, the lack of downward movement for November is positive, and could mean that sheepmeat might be the last Australian commodity on China’s chopping block, as it is not as readily available from other countries. That being said, ABARES December agricultural report does point to the impact of the African Swine Fever on China’s pork production lessening, giving China more access to protein alternatives.

Total exports were above the five-year average for lamb, but fell behind for mutton in November, which again is most likely a consequence of lower production. Sheep slaughter is 31% lower for the year-to-September than 2019, and 21% below the five-year average for that period. China actually took the largest market share of Australian lamb exported in November with 24%, followed by the US at just under 23%, while China remained the clear market leader for mutton at 38%, despite their lower volume intake.

What does it mean?

There doesn’t appear to be any significant increased downward pressure on export demand as of yet from frosty relations with China, and as we pointed out last month, the domestic lamb price is not operating at a huge premium to export values. While international trade is being watched closely at the moment, confidence continues in the sheep industry, and should do so for the time being.

Have any questions or comments?

Key Points

- Total lamb exports down 2% year on year for November, but higher than October volume.

- Total mutton exports are 22% lower for the year-to-date, with volume to China down 44% on 2019.

- Sheepmeat trade to China tracks above five-year average for November, as China takes the biggest market share of exported Aussie lamb for the month.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: MLA, ABARES, Mecardo.