Southern weaner calf sales and the first prime offerings of the year have given some insight into how cattle prices are trending for 2023, and that’s lower. The Eastern States Young Cattle Indicator (EYCI) has opened the year about 14% below where it closed in 2022, and while the market might still be in holiday mode, it’s a good indication of where things are at domestically in terms of supply. However, looking further afield, it’s the price of 90CL beef imported into the US that can shine a bit of light on what’s to come for the demand side of the equation.

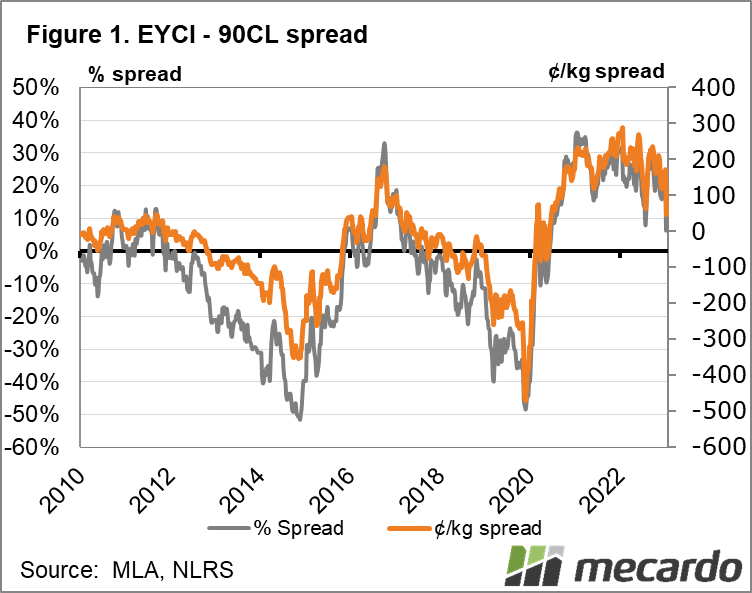

As we discussed back in December, lower Australian slaughter usually equates to an EYCI trending at a premium to the 90CL (the lean cow beef Australia exports to the US). The 90CL has also opened the year lower than where it ended in 2022, but it is only marginally so at about 1%, and at 730¢/kg it is 3% higher than last January. Plus, the first full week of slaughter data in Australia has the east coast throughput 103% up on the last week of December, and 24% up year-on-year.

The EYCI has now been above the 90CL price for more than two years, the longest period this has been the case for at least 20 years. But the above factors mean that the EYCI premium has dropped from more than 170% at the end of 2022, to just 40% this week. Figure 1 shows us the last time the 90CL overtook the EYCI was during the 2018-2020 drought, which was also the last period of high turnoff.

Demand for 2023 does look positive, however. According to the Steiner Consulting Group’s latest update, US cow and bull slaughter (the category which produces the domestic lean beef) has started the year off with above-average volumes, but this is expected to drop off as soon as next month – and stay that way. Drought conditions have improved in many areas, and with the US cow herd estimated to be at the lowest it’s been in nearly a decade, US cull cows are likely to be in tight supply this coming year – meaning lean beef has got to come from imports.

While young cattle supply is on the increase due to the herd rebuild, the difference between now and the last time the EYCI and 90CL spread reversed, Australia’s seasonal conditions had meant significant female turnoff. This time around another good spring and reasonably mild summer means there’s unlikely to be any significant lift in the Female Slaughter Rate (FSR) in the short term. And there is plenty of room for it to move, as according to Meat and Livestock Australia, the FSR averaged its lowest average figure consecutively on record over 12 months from Q3 2021 to Q3 2022 (with Q4 2022 figures yet to be available).

What does it mean?

Last year was one for the record books for the cattle industry. Plenty of rain kept confidence in the beef market sky-high and price ceilings were broken. This confidence saw sustained high prices and restricted supply, but it couldn’t last forever, with more cows in the paddock meaning more calves for sale eventually. This has seen the year open with the EYCI and 90CL converging, a sign the supply/demand equation is shifting. But it isn’t all bad news for producers, with a turnaround in US cow turnoff coming at a good time for Australia, and likely to give support to domestic prices, especially cows.

Have any questions or comments?

Key Points

- Cattle slaughter starts the year off strong pushing EYCI lower

- EYCI still at a premium to 90CL, but spread tightens considerably

- Outlook for US export demand looks positive as their seasonal conditions improve

Click on figure to expand

Click on figure to expand

Data sources: Mecardo; Meat & Livestock Australia; Steiner Consulting Group; DAFF