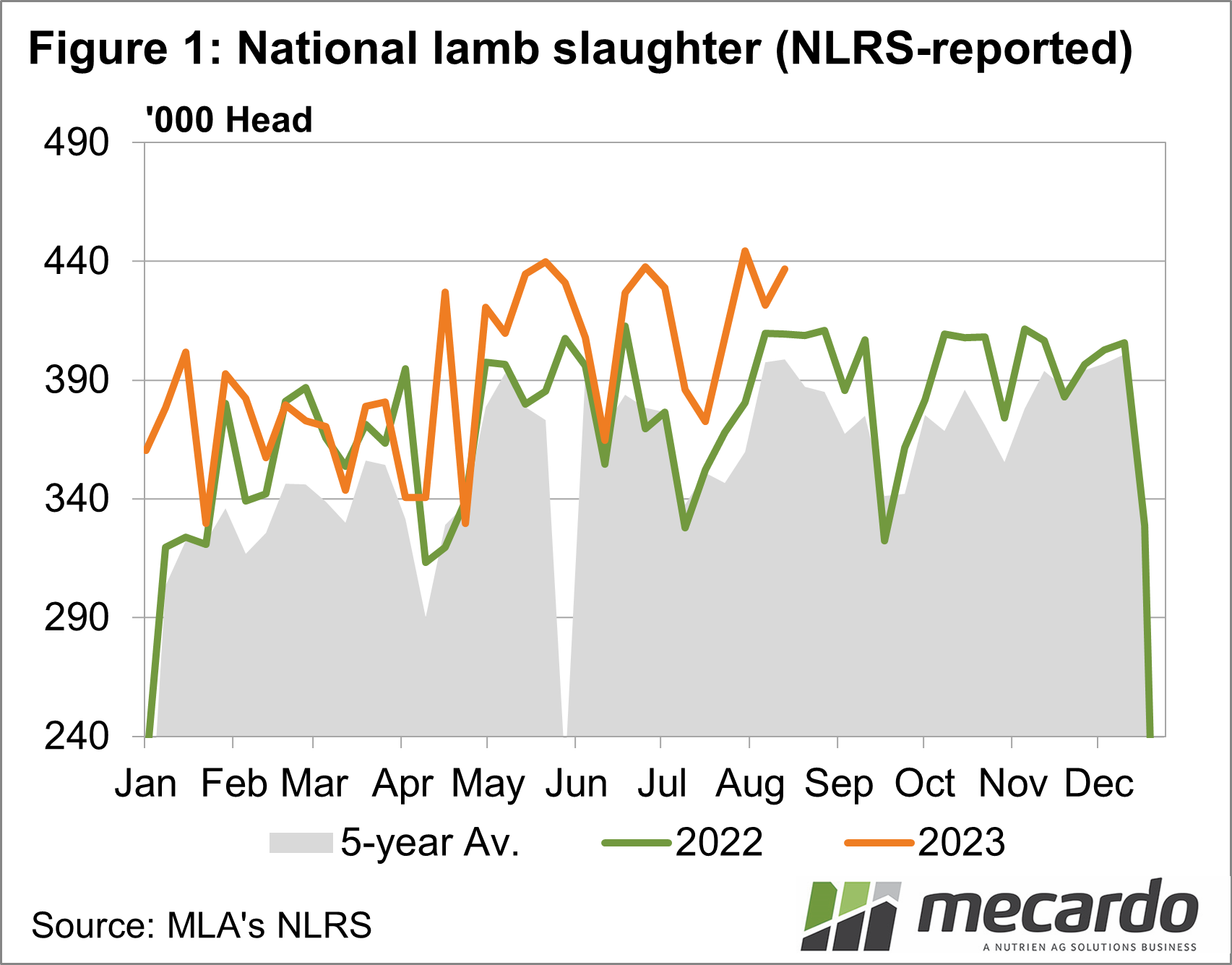

With weekly National Livestock Reporting Service reports showing lamb slaughter at well above both year-ago and five-year-average figures this year, it came as no surprise when the latest Australian Bureau of Statistics quarterly data came in last recently with very strong numbers. From March to June this year, 6.05 million lambs were processed - the third-highest quarter on record, and 11% above the average for that period.

The latest numbers brought the year-to-June numbers to 11.65 million head, which was 11% higher year-on-year, and just 3% shy of 2018. 2018 is the record holder in terms of year-to-June for lamb slaughter.

This means that numbers would have to drop in the second half of 2023 to meet Meat and Livestock Australia’s forecast lamb slaughter for the year (as we forecast last week here). The more likely scenario is we will process more lambs than previously expected. But how many are there actually still to come?

According to the NLRS, the national weekly lamb slaughter is averaging 392,024 head so far this year. This is nearly 13% above the five-year average for the same period, and 7% more than last year. Given the spring flush of new season lambs, traditionally weekly slaughter numbers climb in the second half of the year. The five-year average lifts its weekly lamb slaughter by about 4% from now until the end of the year, while last year it increased by 2.5%.

That said, when we look at the 5-year average, ABS data has the September quarter lamb slaughter 6% lower than the June, but the December quarter is the strongest of the year, climbing to just marginally above March-June. However, it has been well documented that 2023 is expected to be a bumper lamb crop thanks to a replenished flock, with skyrocketing mutton slaughter and seasonal conditions in some areas supporting stocking rates.

Let’s say the average weekly lamb kill figure stays the same for the remainder of 2023, then MLA would be spot on with their predictions (which is likely how they got to the figure when they revised it lower from its February forecast) and 10.2 million lambs will be processed in the second half of the year. This would be lower than both last year’s second half, and the average for the June-December period. However, considering the weekly average lamb slaughter has jumped by about 5% since the start of July, and the observations made above, there’s a strong chance it will increase.

If the weekly slaughter remains where it has been since the start of this quarter, it will be more like 10.75 million lambs to be processed from July-December, which just surpasses the same period in the record-breaking 2018 season and is half a million more than the forecast. At the extreme end of the spectrum, if the second half of the year tracks at 7% above the ABS five-year-average lamb slaughter (which is what the first two quarters were) then nearly 12.5 million lambs will go through the system. This is unlikely given the inflated throughput for the first half of 2023 due to held-over lambs, but interesting for context of where things have been tracking so far.

What does it mean?

If the predicted drier spring eventuates, some producers won’t have as many options as they’d like to hold over lambs until the new year, despite current lower prices. Historically, there is very little upside in lamb prices from now through to the end of the year, with improved quality holding them firm through the start of spring before the supply outweighs new season demand. So even if the most reserved slaughter figures eventuate, which will still be historical highs, there will be little market relief for producers in 2023.

Have any questions or comments?

Key Points

- ABS lamb slaughter lifts 11% year-on-year for the year-to-June, just shy of the record 2018 throughput.

- Current NLRS average weekly lamb slaughter is trending at 13% above the five-year average.

- If slaughter rates remain at current levels, half a million more lambs than the MLA’s previous forecast are still to come.

Click on figure to expand

Click on figure to expand

Data sources: MLA, Mecardo