Producer’s intentions to continue rebuilding Australia’s sheep flock have diminished since October, as market prices have lowered, and input costs (namely interest rates) have risen.

Meat and Livestock Australia and Australian Wool Innovations latest sheep producer sentiment survey was conducted in May, and it found sentiment around the sheep meat industry for the next 12 months had decreased significantly. On the other hand, sentiment about wool for the coming year has increased slightly, with three of the four biggest wool-producing states thinking things are looking up, with WA being the outlier.

The February condensed version of this survey focussed on lamb sales, with the latest full update looking more closely at both the breeding ewe and wether flocks. Breeding ewes are reported to make up 66% of the entire flock in this survey, up from 58% in October’s results. This actual breeding ewe number has also increased, from 37.5 million head in October to 46.1 million currently. A better comparison of actual ewe numbers might be with the June 2022 survey, however, which recorded 42.5 million breeding ewes.

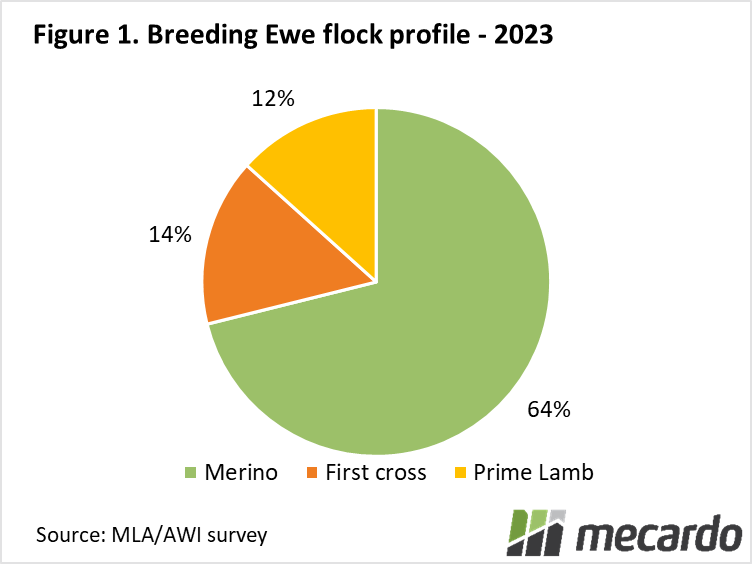

In this survey, Merinos made up 64% of that figure, with first-cross ewes at 14% and ‘prime lamb’ (meat-only) production’ were at 12%. Of those producers surveyed, 56% had Merinos in their operations, and 70% of the Merino ewe flock was being used for pure Merino production. This was a reduction from 12 months prior, where Merinos made up 72% of the ewe flock, and 71% of that were Merino-Merino joined.

Producer intentions have been scaled back since October, with just 30% of respondents planning to increase their flock numbers in the next 12 months, compared to 46% in October who forecasted they would be producing more lambs this year than last. While 22% were planning to decrease production from 2022 to 2023 in the previous survey, this time around 32% are looking to downsize. Unsurprisingly, the uncertainty of the future of the live export industry has impacted WA producer intentions, with nearly half of those surveyed expecting to decrease numbers, and sentiment for both the wool and sheep meat industry being lower than recorded in October.

What does it mean?

Producers looking to increase their breeding flock into 2024 are predominantly (66%) planning on retaining more replacement ewes, rather than holding onto their older ewes (20%). This is about a 10% swing away from old ewe retention compared to the previous June. And not only is there a higher percentage of producers looking to downsize, but they will also lose more ewes (4.5 million head) than those planning to grow will gain. And 69% of those decreasing numbers plan to cull older ewes more heavily than usual.

This means despite the forecast flock growth of 1% between now and next year, old ewes going through the mutton market will be on the increase, boosting slaughter numbers and putting more pressure on the mutton price.

Have any questions or comments?

Key Points

- Producer intention survey forecasts breeding ewe flock to fall 6% from 2023 to 2024.

- Producer intentions split down the middle, with 30% planning to increase their flock, and 32% to decrease.

- WA producer sentiment of the industry is well below the rest of the country as live export ban concerns rise.

Click on figure to expand

Data sources: MLA, AWI, Mecardo